Live preview mode. Wire is not yet published.

25% further downside for Telstra?

B B

Telstra has been a core portfolio holding for many investors after being privatised at $3.30 per share in 1997. Today, the stock is trading at $2.73, well below its initial public offering price 21 years ago.

The difficult performance of Telstra since listing is because its dominant market position has gradually been eroded by the natural forces of competition and technological change.

In this wire, we highlight the risks around Telstra’s earnings and dividend from a further decay in Telstra’s core business of mobile phone subscriptions.

Our research suggests investors should be prepared for lower future earnings from Telstra - and a substantial cut in the dividend.

The market does not appreciate the decline in Telstra’s mobile earnings

The impact of the NBN on Telstra’s profitability is well understood as data moves from Telstra’s copper wires to the government’s fibre optic network.

What is less appreciated is the decline in Telstra’s mobile earnings now underway (mobile earnings represent 50% of TLS’ operating profit). Perhaps this is not surprising, as even Telstra has been late to acknowledge the deterioration in mobile profitability. Telstra were still targeting mobile earnings growth as recently as May 2018.

Background: The mobile phone industry

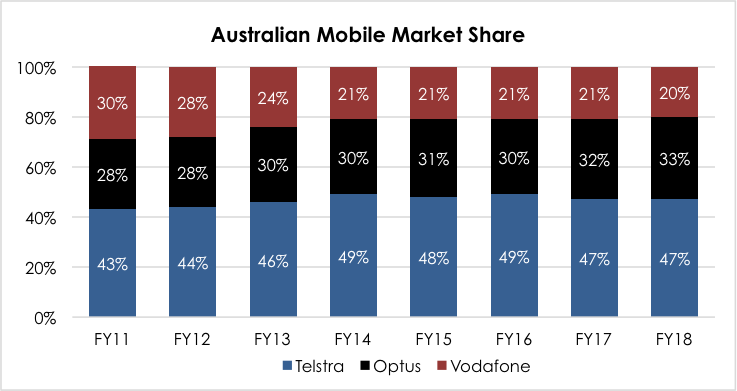

Telstra has dominant market share in Australia’s mobile sector, with almost 50% of post-paid mobile accounts, and circa 60% of mobile industry profits (EBITDA). Optus is the other major player with a 30% market share, with Vodafone at 20%.

Telstra’s mobile pricing is too high

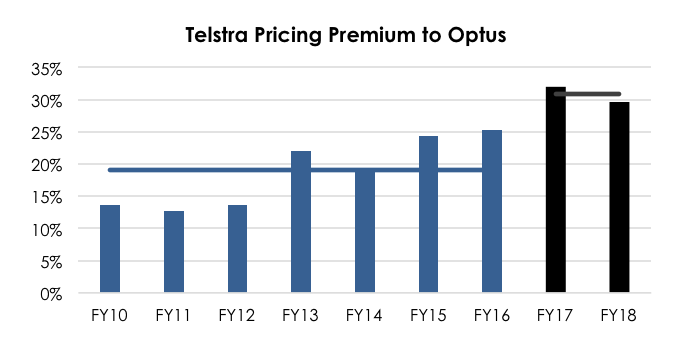

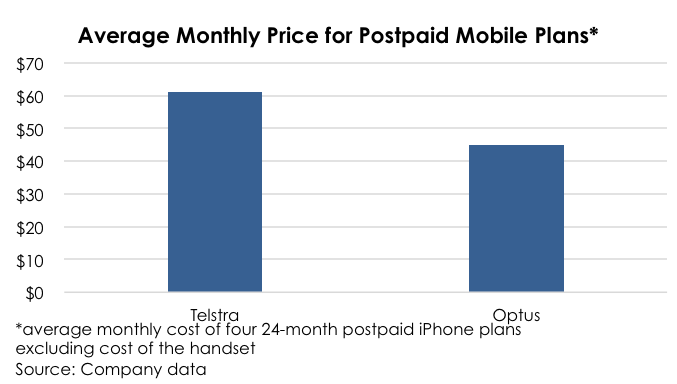

Telstra’s mobile pricing is now 30% above Optus. We believe the combination of Telstra’s dominant market share and materially higher mobile prices have left Telstra vulnerable to intensifying mobile competition from the existing players, as well as new entrants such as TPG Telecom (TPM).

Who is leading the charge on mobile competition?

We see Optus as the key source of competitive pressure on Telstra’s mobile business. After substantial investment in recent years, Optus is now widely regarded as having comparable mobile network quality to Telstra, which is substantiated by a recent independent study ranking Optus as Australia’s top mobile network.

Telstra mobile pricing premium to Optus has continued to rise…

Optus has capitalised on its significant mobile phone price discount to drive market leading mobile customer growth over the last two years. This has caused Optus’ market share to increase by +2.1% since 2016, while Telstra’s market share has declined -1%.

Telstra competitive response is not enough

We believe intensifying competition in the face of Telstra’s high pricing premiums has created pressure for Telstra to cut mobile prices to preserve its customer base. We are starting to see this unfold, with Telstra announcing at its June Investor Day that it will release lower priced mobile plans from July 2018.

What is Optus trying to achieve by aggressively chasing market share?

Optus is the second largest mobile phone player but has a market share significantly lower than Telstra. Their best strategy is to remain aggressive on price to produce material growth in customer numbers, grow market share and leverage the significant investment they have made in improving their network quality. This appears to be what they are doing.

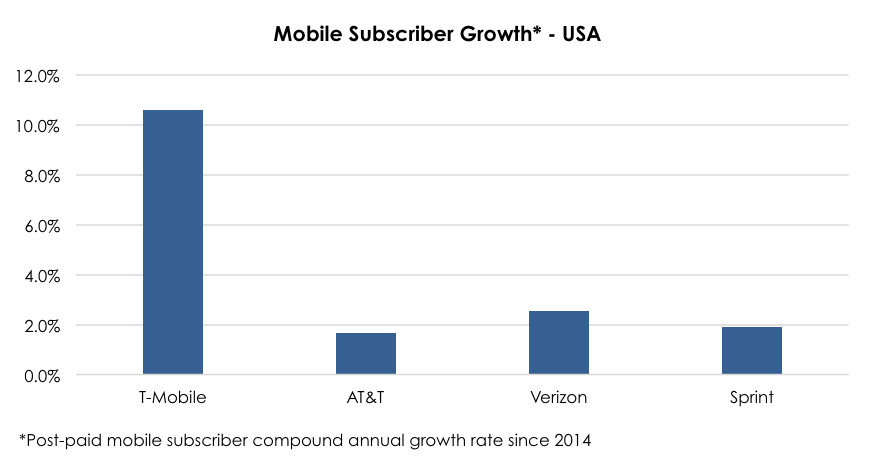

Our work on the US mobile industry suggests Optus could be pursuing a similar strategy to challenger network T-Mobile in the US.

In 2014, T-Mobile was the number four mobile competitor in the USA. It priced its mobile offering ~20% below its competitors. In just four years T‑Mobile delivered customer growth of 11% per annum, versus peers at just 2% per annum. T Mobile’s operating profits almost doubled over the same period.

Telstra earnings and free cash flow implications

We expect to see continued downside pressure to Telstra’s share price over the months ahead.

If we factor in Telstra cutting its mobile phone charges by 20% over the next three years, we estimate a 30% decline in core free cash flow (excl. one-offs) over this same time period. We note, our analysis incorporates Telstra’s announced cost-out plans.

This would see core free cash flow per share decline from 20 cents to 14 cents per share, and the dividend declining to circa 12 cents per share. If we assume that Telstra trades on a 6% fully franked yield then it would trade at approximately $2.00 per share, representing 25% downside from current levels.

We expect to see continued downside pressure to Telstra’s share price over the months ahead.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

By

B B,

1 stock mentioned

B B

Expertise

B B

Expertise

Comments

Comments

Sign In or Join Free to comment