3 reasons to lighten your equity exposure

Although headline returns from equity markets have remained buoyant over recent months, signs of some fracturing of the steady state equilibrium that has supported such an extended rally have begun to emerge. China, Latin America, and now most recently selected European markets, have all recorded material corrections.

Increasingly, it has been the United States standing almost alone in driving overall market averages higher and fulfilling its role as a safe haven for nervous money. In the calendar year to date, Japan and Europe have experienced no share market gains, whereas the U.S. (up 9.7%) and Australia (up 7.2%) have been standout performers.

Risk #1: Spike in wages and inflation likely

Notwithstanding investor confidence in the U.S. and Australian share markets of late, there is cause for caution in both markets – for quite different reasons. In the U.S., the much awaited spike in wages and inflation remains likely, providing the laws of supply and demand in labour markets still ultimately hold. A subsequent readjustment in bond yields at a time when quantitative easing is being unwound is unlikely to be conducive to smooth sailing for equity or credit markets.

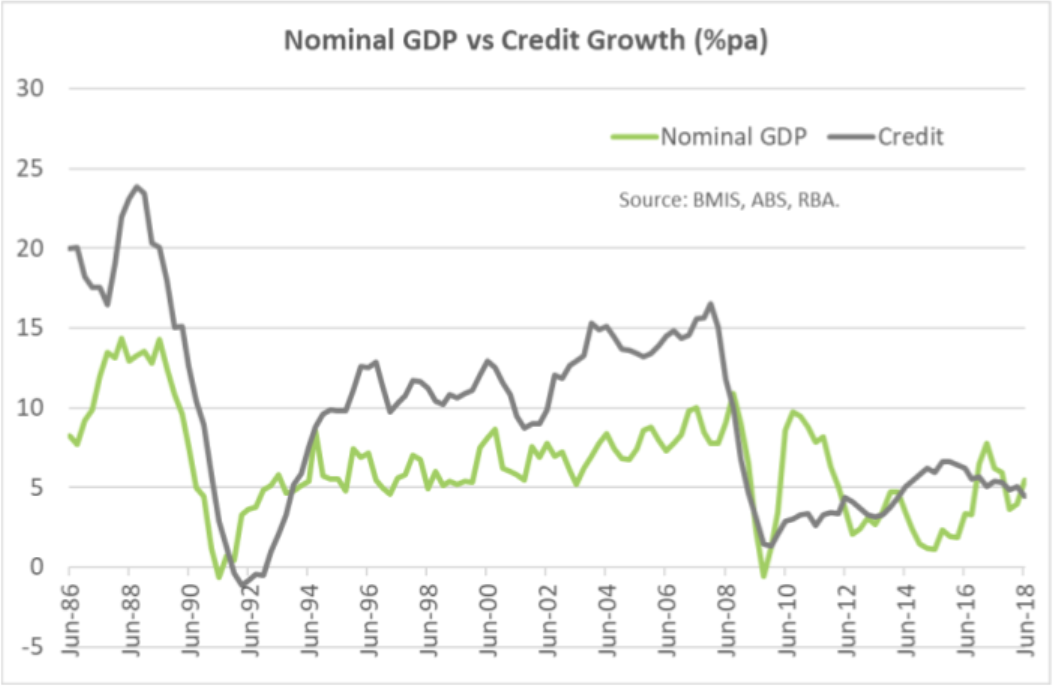

Risk #2: Low credit growth signals potential downturn

Locally, the downward momentum in the housing cycle and the evidence of weak credit growth suggests a softening in the economic outlook. As indicated on the accompanying chart, periods in Australia when credit growth is running below the level of nominal GDP, as it is currently, are rare and typically associated with sharp cyclical downturns. The household sector now has minimal capacity to increase spending in absence of credit, given the subdued state of wages growth and the fact the savings ratio is approaching zero. Unless there is an unexpected jump in business investment or surge in net exports, it is difficult to see a post housing boom economy being supportive of the local share market in the year head.

Risk #3: Political risks rising in both Australia and the US

What the U.S and Australia do have in common, though, is political risk. In the U.S., the mid-term elections in early November and the fallout from the increasingly problematic Chinese tariff escalations threaten to destabilise an administration that has proven supportive of equity markets. In Australia, a change of government next year appears likely, bringing a range of policy measures that may have at least a short-term negative share market impact. Adding to the political uncertainty is the forthcoming Wentworth by-election. History shows the resignation of a popular local member can produce very big swings in by-elections. Whilst the existing 17% margin in Wentworth suggests it is unlikely the government will lose its Lower House majority, it should be remembered that the seat’s margin was a far narrower 3.8% as recently as 2007.

How to play these risks

Hence the combination of valuation, political and economic cyclical risks do warrant some tactical underweighting of equity exposures. This could be achieved either via a switch in asset classes or via the use of managers with an expectation of lower downside participation. Managers with less tendency to hold stocks with inflated Price Earnings may show significant relative outperformance in the event of any general correction, given the nature of the recent cycle. In addition, a larger underweight to Australian rather than global equities could be considered, with the latter having the benefit of being able to be held with unhedged currency. Unhedged currency provides a potentially “safer” option, with the $A vulnerable to depreciation due to negative local factors or a more widespread global correction. In addition, in the event the U.S. economy and share market continues to advance forward unabated, the interest rate differential between the U.S. and Australia would likely continue to expand, thereby placing further downward pressure on the $A.

Changes to asset allocation

In our tactical program, some of the proceeds from lower equity holdings have been allocated to Property & Infrastructure, with relative valuations of global infrastructure improving over recent months.

Longer-term bonds continue to offer insufficient compensation for the risks that inflation may ultimately normalise. With credit risks remaining largely benign, credit exposure should remain a component of the fixed interest portfolio. However, credit spreads are insufficiently wide to generate overly attractive return prospects from this sector.

With underweight positions in place for equities and fixed interest, there are few options other than to be overweight in cash and Alternatives. If the pickup in volatility so far this year is continued, opportunities for higher returns from Alternatives may be forthcoming.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

I founded the investment consulting business, Brad Matthews Investment Strategies. BMIS provides assistance to financial planning practices in developing their investment philosophy and creating portfolio solutions consistent with this philosophy.

Brad Matthews Investment Strategies

I founded the investment consulting business, Brad Matthews Investment Strategies. BMIS provides assistance to financial planning practices in developing their investment philosophy and creating portfolio solutions consistent with this philosophy.

Expertise

Brad Matthews Investment Strategies

I founded the investment consulting business, Brad Matthews Investment Strategies. BMIS provides assistance to financial planning practices in developing their investment philosophy and creating portfolio solutions consistent with this philosophy.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

This recently triggered market signal has never failed to predict gains

Ophir Asset Management

Equities

Meet the perfect investor (and how you can beat them)

Livewire Markets