TOL - 24th Dec, 2024

7 Magnificent Miners: The outlook for copper, iron ore, lithium, coal, gold, nickel and uranium

Stay the course? Buy the dip? Or get out while you still can? These are the questions Australian mining investors want answers to in 2025.

On the 8th day of Christmas, Livewire gave to me...

Magnificent miners and the outlook for commodities

As a proud West-Aussie, the mining industry has always been a major area of interest for me – both in terms of how it has shaped the great state of Western Australia over the last 25 years – and via its contribution to the Australian investing landscape.

But, you don’t have to be a sandgroper to have an interest in investing in mining stocks. Aussies love their mining stocks, and they love a punt, and often the two are inextricably linked. Mining companies raise capital from investors in the hope that both parties can strike it rich should the correct rock be kicked over in the correct desert!

Sure, one can invest in boring old blue-chip banks and insurance companies, perhaps a little CSL, and throw in a couple of supermarkets – but, there’s always going to be a special place in the Great Australian Portfolio for mining stocks. Everything from tiny rock-kickers all the way up to our global mining behemoths.

Unfortunately for most investors, 2024 has been a disappointing year for the mining component of their portfolio. The S&P/ASX 200 Resources Sector Index (XJR) is down 13.8% year to date, and is on track for its worst annual performance in 9 years. Stay the course? Buy the dip? Or get out while you still can? These are the questions Australian mining investors want answers to in 2025.

{kind=link}

Good news, hopefully I’ll be able to provide some insights into what to expect for Australian mining stocks next year. For seven of the major commodities: copper, nickel, lithium, uranium, iron ore, coal, and gold, I’ll recap the year that was and bring you the latest views from the experts on what to expect for each over the next 12-months.

Even better, I’ll propose a Magnificent 7 of ASX-listed mining stocks – one for each commodity – that the big brokers most view as best placed to capitalise on its opportunities in 2025. Let’s dive in!

Copper - Still the next big thing in commodities?

Copper market and outlook

Copper was supposed to be the “next big thing” in metals in 2024. On paper, the medium to longer term fundamentals did appear to be sound heading into the start of the year. Copper’s energy transition credentials are well documented, for example, China consumes roughly half of the world’s copper supply and around two-fifths of this consumption is linked to the country’s power infrastructure – particularly the sweeping modernisation of its electrical grid.

According to Citi, global end-use copper consumption grew a robust 7.6% annually in October, with demand from decarbonisation segments increasing 36% p.a. (the highest rate of growth since January). Demand from cyclical segments, like manufacturing, grew 4.5% p.a. – a healthy set of numbers indeed.

Yet, as Citi also notes, the supply side of the copper equation has also improved this year. Miners, particularly in the world’s biggest producing country of Chile, have enjoyed better production conditions and fewer supply-chain disruptions. This means copper inventories are around 250kt higher now than compared with the start of the year, Citi notes.

{kind=link}

Looking forward, the broker expects that an easing Chinese economy and tariff threats would likely combine to deliver subdued copper pricing in the first half of 2025 – to around US$8,500/t versus the current price of around US$9,000/t. Longer term, Citi remains constructive on the copper outlook for many of the same big picture themes copper bulls had pegged at the start of this year. The broker forecasts copper will reach US$11,000 by 2027 – that’s around 22% upside.

Which ASX copper stock makes the Magnificent 7?

I’ve deliberately only considered stocks that derive the bulk of their earnings from copper. For a full overview of the ASX copper sector, you might want to check out this article I wrote earlier in the year: Everything you need to know about every ASX copper producer.

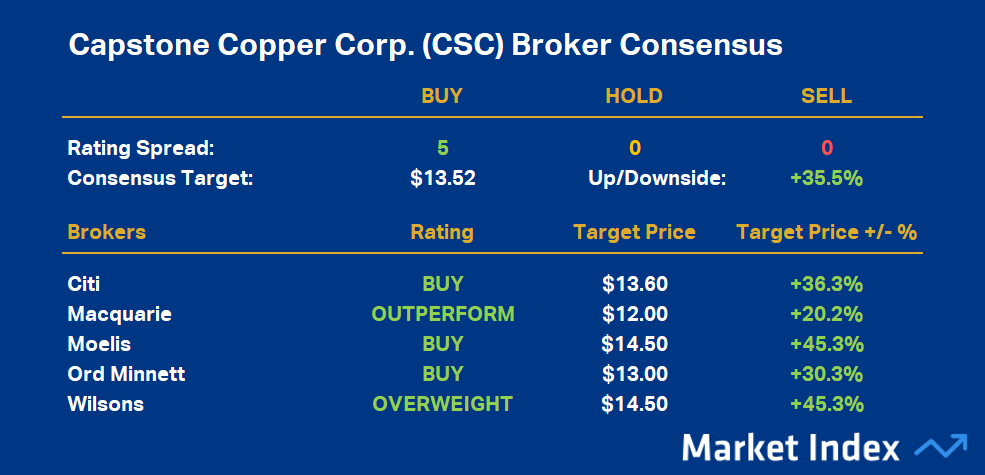

Looking through the list of candidates, and comparing against their current Broker Consensus data, it’s slim pickings for this Magnificent 7 spot. There is only one ASX copper producer that has a Broker Consensus rating equivalent to a buy – unanimously so I might add. It’s Capstone Copper Corp. (ASX: CSC).

%20Broker%20Consensus%20data.png)

Capstone Copper Corp. (CSC) is the most highly rated ASX copper stock (click here for full size image)

%20Broker%20Consensus%20data.png){kind=link}

To obtain a stock’s Broker Consensus Rating, we assign a value of +1 to any rating better than HOLD/NEUTRAL/MARKETWEIGHT, a value of 0 for any rating equivalent to HOLD/NEUTRAL/MARKETWEIGHT, and a value of -1 to any rating worse than HOLD/NEUTRAL/MARKETWEIGHT.

We then take the average of all assigned rating values and assign a Broker Consensus Rating of BUY to values greater than +0.5, a rating of HOLD for values between -0.5 and +0.5, and a rating of SELL for values less than -0.5.

The Broker Consensus Target is simply the average of the target prices we have on file for each broker. Typically, brokers define their target prices as a 12-month forecast. Each target price is based on fundamental valuation assumptions.

CSC’s broker consensus rating is +1.0, resulting in a Broker Consensus Rating of BUY. Its Broker Consensus Target is $13.52. This suggests brokers collectively believe the stock is around 35.3% undervalued based upon the closing price on Wednesday, 18 December of $9.98.

Nickel - If you can’t beat ‘em, join ‘em

Nickel market and outlook

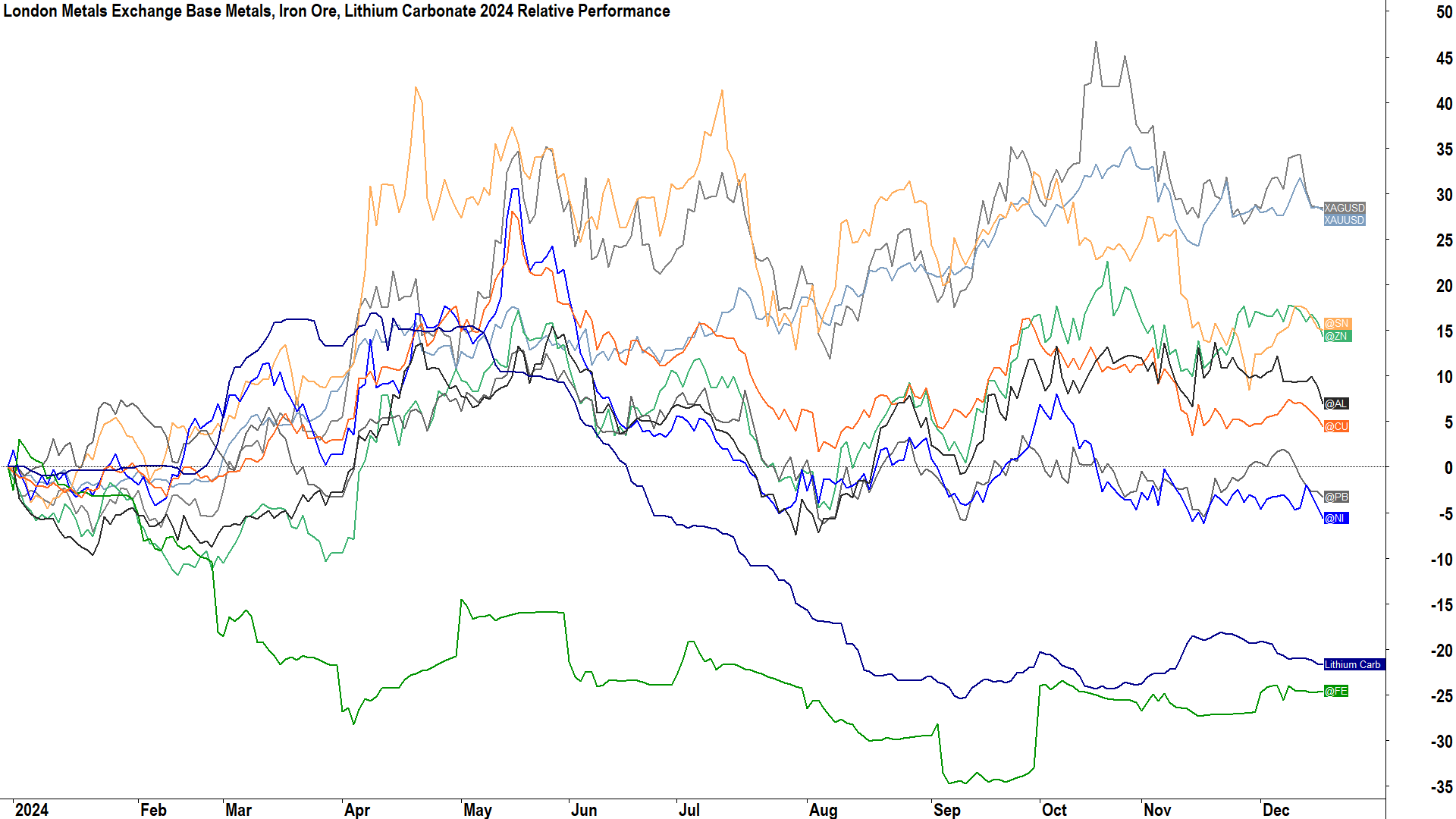

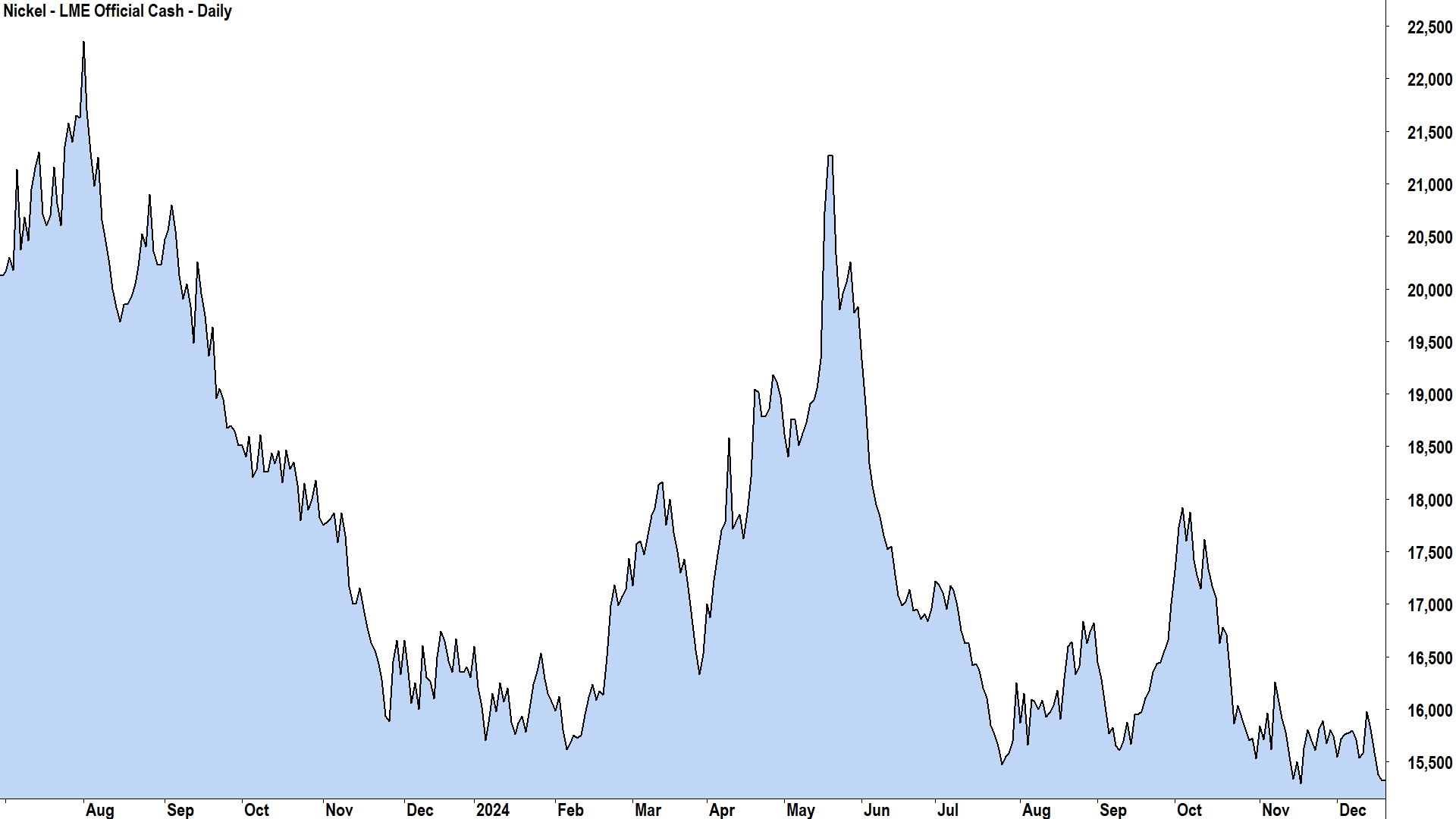

Nickel has been the worst performer among the base metals complex on the London Metal Exchange this year, losing 5.6% compared to the next worst performer, lead, at a 3.3% loss.

{kind=link}

To be fair, the nickel market hasn’t been the same over the last couple of years as Indonesia has rapidly ramped up production of nickel pig iron and other lower-grade nickel materials used predominantly in stainless steel. This ramp up has been heavily influenced by Chinese steel producers who have invested heavily in Indonesian smelters to secure feedstock.

Indonesia is on track to supply over half of the world’s nickel in 2024, and its rapid and massive transformation has reshaped the global nickel market. The flood of lower-grade Indonesian nickel has dragged on prices at a time major consumer, China, looks set to deliver its fourth straight year of lower steel production.

Traders are short nickel, suggests Morgan Stanley. The broker notes the market has recently swung back to net shorts due to:

- The current price does not incentivise additional supply cuts among producers (several higher cost producers, mainly Australian, put projects into care and maintenance this year because of the low nickel price)

- Peak EV seasonal demand is waning, and more generally, nickel-based batteries are losing market share to other technologies

- The stainless steel backdrop remains “soft”

{kind=link}

Morgan Stanley concludes that “demand risks are more skewed to the downside than upside” for nickel in 2025, concluding that whilst there is some cost of production support around US$16,000/t, there’s likely little impetus for the nickel price to rise above US$18,000/t in the near term.

Which ASX nickel stock makes the Magnificent 7?

There are even fewer ASX-listed nickel pure-plays than copper ones. Even fewer again, since BHP shut down its Nickel West division in July and Mincor (subsequently acquired by Andrew Forrest’s Wyloo Metals) shut down its Kambalda operations last year. Australia’s largest remaining locally-based nickel producer is IGO (ASX: IGO), but its fortunes are substantially tied to lithium.

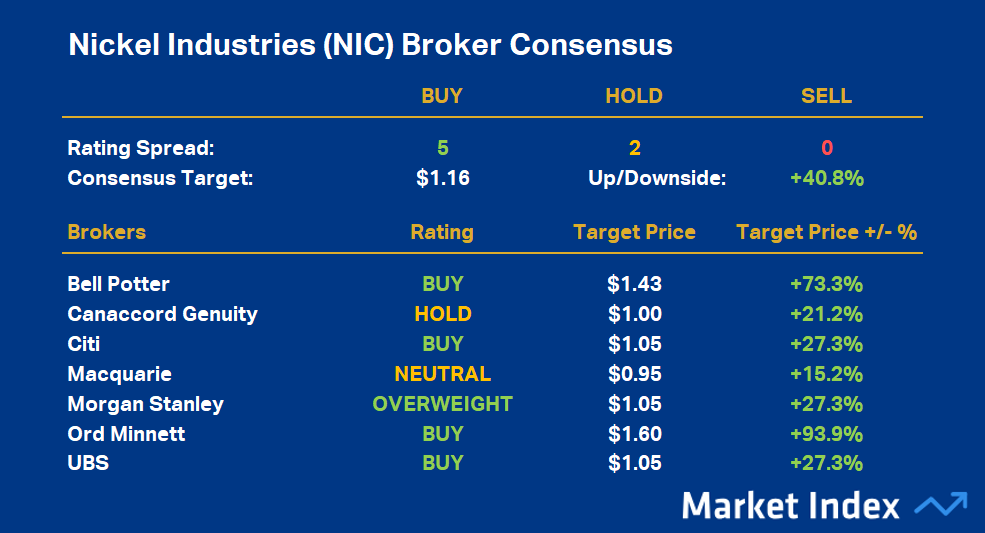

There is another ASX-listed nickel producer, a pure-play mind you, that the brokers rate very highly. Ironically, its production is exclusively Indonesian based – potentially making it part of the problem or part of the solution for those looking for nickel exposure. I am of course talking about Nickel Industries (ASX: NIC). Hey – if you can’t beat ‘em, join ‘em!

%20Broker%20Consensus.png)

Nickel Industries (NIC) is the most highly rated ASX nickel stock (click here for full size image)

%20Broker%20Consensus.png){kind=link}

NIC’s broker consensus rating is +0.71, resulting in a Broker Consensus Rating of BUY. Its Broker Consensus Target is $1.16. This suggests brokers collectively believe the stock is around 40.8% undervalued based upon the closing price on Wednesday, 18 December of $0.825.

Lithium - Wall of supply now lower, but still too high

Lithium market and outlook

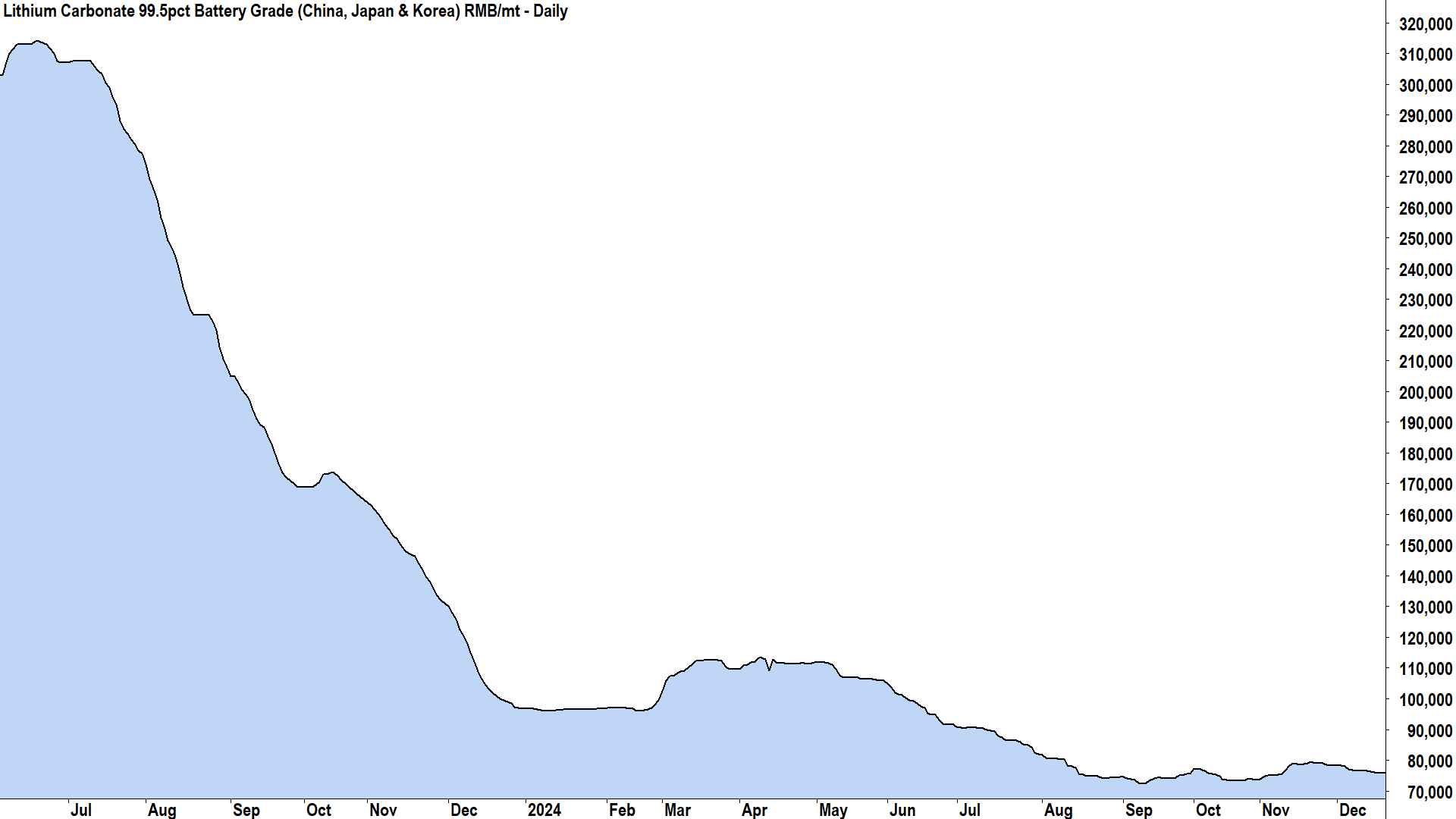

I’ve written extensively about the lithium market in 2024. It was a year characterised by a wall of supply meeting lower than expected demand. Some of the uneconomic supply was removed this year, however, and several planned ramp-ups were curtailed (see this article I wrote in November for full details).

The wall of supply may be a few courses lower at the end of 2024 than it was at the start of it, but lithium minerals prices are still faltering. Most analysts at the big brokers are calling the low is in for now, but the consensus is similarly confident that lithium prices are unlikely to rebound strongly any time soon.

Unlike in other industries, it is easier for idled lithium supply to re-enter the market should prices recover. This means that even if we do see a pick-up in demand as growing battery production more than accounts for near term headwinds like the rise of hybrid vehicle platforms (less lithium intensive) – prices are likely to be capped.

RMB90,000/t is the key level that Macquarie tips will incentivise the supply that was withdrawn in 2024 to return. The broker also notes the potential for near-term price weakness as end of year seasonal restocking winds down.

%20CNY-mt%20price%20chart.%20Source%20SMM.png)

%20CNY-mt%20price%20chart.%20Source%20SMM.png){kind=link}

So, it seems that whilst lithium prices have most likely stabilised, 2025 is unlikely to deliver the sort of price recovery many lithium bulls are hoping for. Indeed, most brokers presently forecast the prevailing surplus in the lithium market will peak in 2025, and then gradually decline through the second half of the decade.

Which ASX lithium stock makes the Magnificent 7?

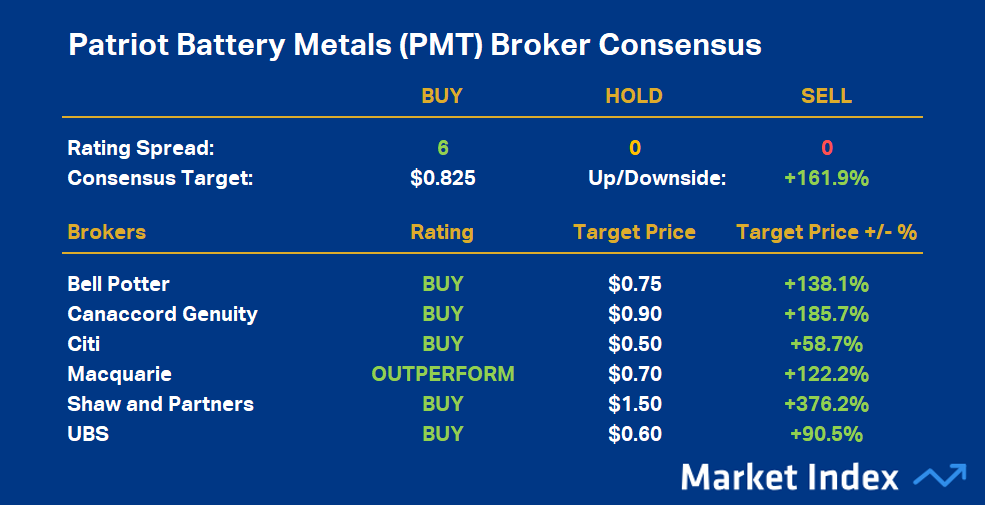

This one was easy. Hands down, the most highly rated ASX lithium stock is Patriot Battery Metals (ASX: PMT). However, I note that the brokers haven’t exactly had a smooth time with their unanimous buy-equivalent ratings here – with the stock suffering a withering share price decline throughout 2024.

%20Broker%20Consensus.png)

Patriot Battery Metals (PMT) is the most highly rated ASX lithium stock (click here for full size image)

%20Broker%20Consensus.png){kind=link}

PMT’s broker consensus rating is +1.0, resulting in a Broker Consensus Rating of BUY. Its Broker Consensus Target is $0.825. This suggests brokers collectively believe the stock is around 162% undervalued based upon the closing price on Wednesday, 18 December of $0.315.

Uranium - Never underestimate the Force (of the supply-side)

Uranium market and outlook

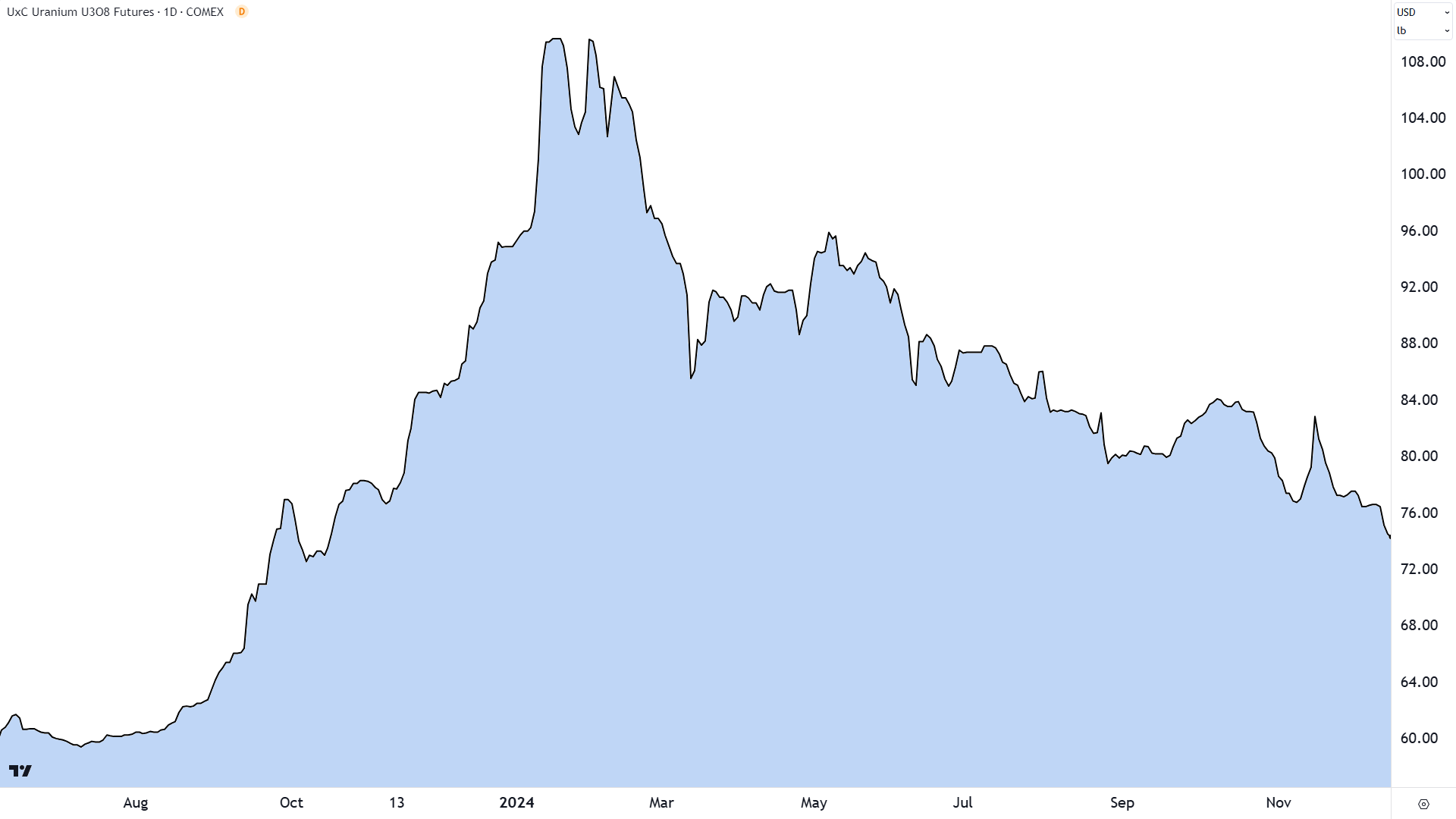

Uranium is one of many disappointing commodity stories of 2025. Like copper and lithium, there are several big picture narratives that paint a booming demand-side of the uranium price equation. Unfortunately, many investors focus too much on demand-side narratives and forget there’s also a supply-side of the equation.

If prices rise, the supply-side wants nothing more than to capitalise. This means they will find any way they can to get supply to market. Before too long, increased supply balances out the prevailing environment of excess demand, causing prices to moderate.

Possibly, that earlier environment of excess demand was driven by genuinely relevant bullish narratives. Possibly also, plenty of fear of missing out (“FOMO”) given supply at the time was lacking. However, when the demand-side realises there’s little reason to FOMO anymore – that the market is indeed likely to be adequately supplied – they cool their heels and prices can really come back fast.

%20COMEX%20price%20chart.%20Source%20TradingView.png)

%20COMEX%20price%20chart.%20Source%20TradingView.png){kind=link}

Case in point: The uranium price chart in 2024. The uranium bull market of 2023 endured little more than one month into 2024. The current price is around 30% lower since then, and it’s getting very close to the marginal cost of production for several newer producers.

Like copper and lithium, it was uranium’s supply side that curtailed what was a very promising bullish narrative. Major players, Kazakhstan’s Kazatomprom and Canada’s Cameco Corporation, have been joined this year by new ASX-listed producers in Boss Energy (ASX: BOE) and Paladin Energy (ASX: PDN).

Uranium supply is likely to continue to exceed uranium demand in 2025, according to UBS. The broker forecasts that a planned production increase by Kazatomprom, the world’s largest uranium producer, will help drive a 6-7% rise in uranium supply next year as that company aims to lift volumes by 12%.

Compared to this, global nuclear reactor demand growth will likely be closer to 3.4%. After crunching the numbers, UBS has pegged the uranium price at US$78/lb in 2025, and US$80/lb in 2026 – offering only a modest upside from the current price of US$75.10/lb.

Which ASX uranium stock makes the Magnificent 7?

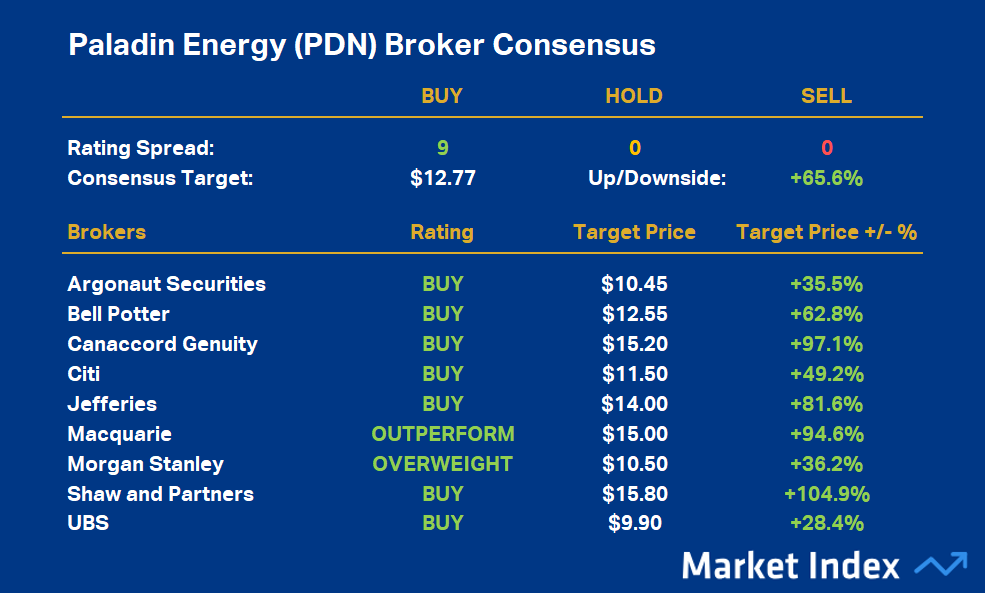

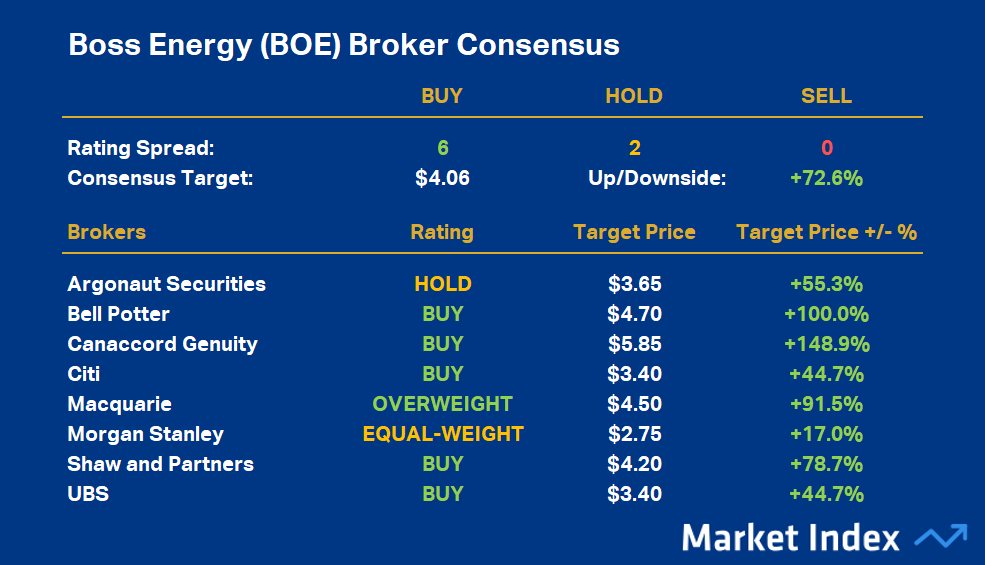

It’s a very close call between BOE and PDN here, with just two hold-equivalent ratings preventing BOE from achieving PDN’s clean buy-equivalent clean sweep. BOE, however, had greater upside compared to its Broker Consensus Target. For this reason, I provide you with Broker Consensus readouts for both!

%20Broker%20Consensus.png)

Paladin Energy is the highest rated ASX listed uranium stock (click here for full size image)

%20Broker%20Consensus.png){kind=link}

PDN’s broker consensus rating is +1.0, resulting in a Broker Consensus Rating of BUY. Its Broker Consensus Target is $12.77. This suggests brokers collectively believe the stock is around 65.6% undervalued based upon the closing price on Wednesday, 18 December of $7.71.

%20Broker%20Consensus.png)

Boss Energy is the second highest rated ASX listed uranium stock (click here for full size image)

%20Broker%20Consensus.png){kind=link}

BOE’s broker consensus rating is +0.75, resulting in a Broker Consensus Rating of BUY. Its Broker Consensus Target is $4.06. This suggests brokers collectively believe the stock is around 72.6% undervalued based upon the closing price on Wednesday, 18 December of $2.35.

Iron ore - A good place to hide?

Iron ore market and outlook

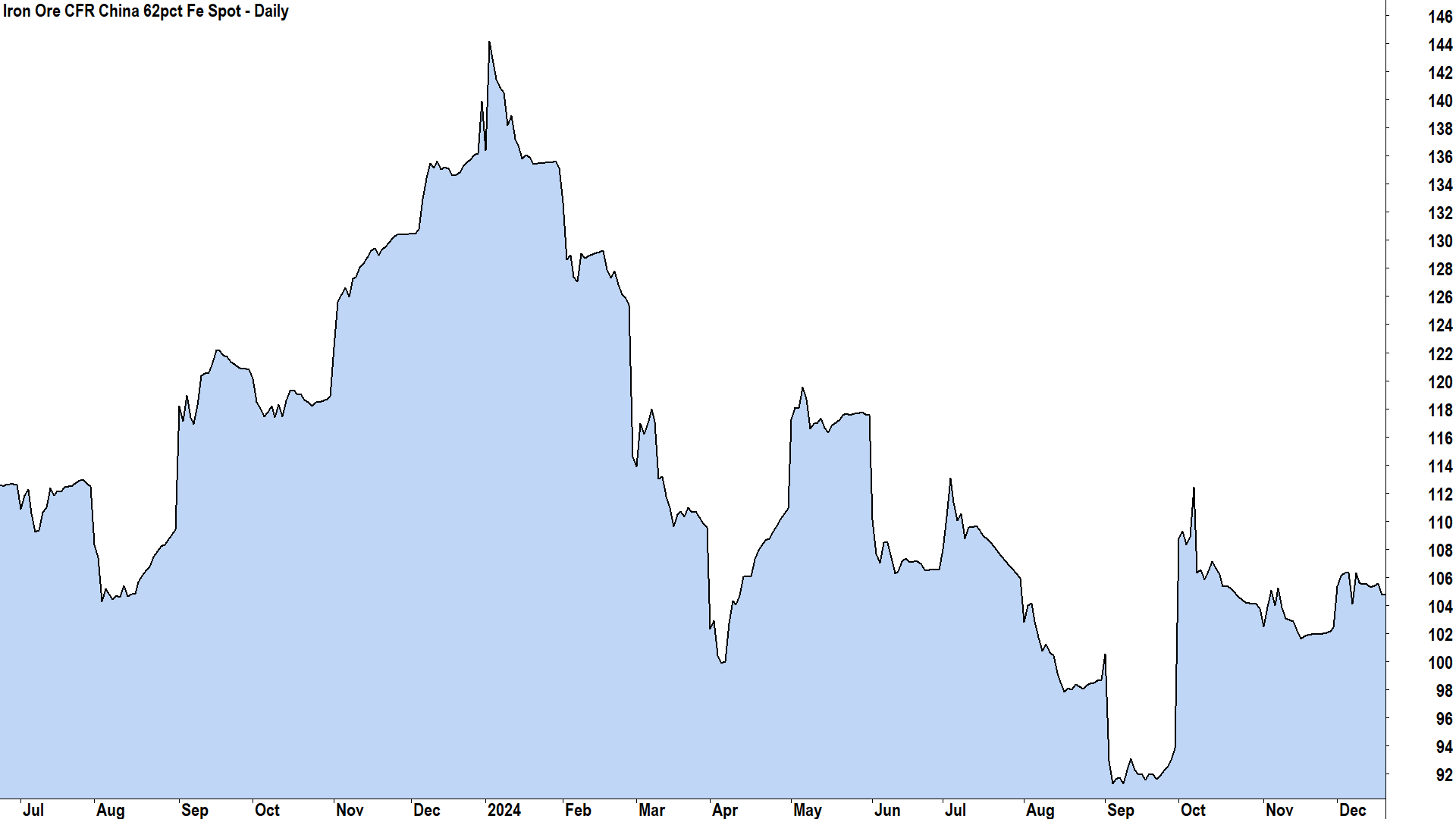

Iron ore has also delivered investors substantial disappointment in 2024. On 3 January the iron ore price was riding high at over US$136/t, having roughly doubled from the May 2023 lows. By mid-September it was back below US$88/t, and it has since recovered to around US$104/t.

Without the mid-September announcements from the People’s Bank of China (“PBOC”) of a range of monetary policy measures aimed at jump starting the ailing Chinese economy, and subsequent promises from Beijing of further monetary and fiscal stimulus to come – one feels things could have turned out much worse for iron ore in 2024.

{kind=link}

Still, Morgan Stanley offers that iron ore might be a “good place to hide” in 2025. Sure, Chinese steel production has eased for several years, but this also means that steel inventories in the country are at their lowest level since 2019. This creates a “restock opportunity” for iron ore, suggests the broker, who also notes that cost of production support at US$90/t should also underpin prices in 2025.

Hide is one thing, prosper is another. Morgan Stanley's price target of US$105/t in the first quarter of 2025 offers only slender upside, but this improves slightly to US$110/t by the end of the year (and remains so in 2026).

Which ASX iron ore stock makes the Magnificent 7?

Morgan Stanley’s upside forecasts for iron ore in the short and medium term may appear modest, but one must remember that our local iron ore behemoths – with their cost bases in the US$20’s/t – are printing money around current levels.

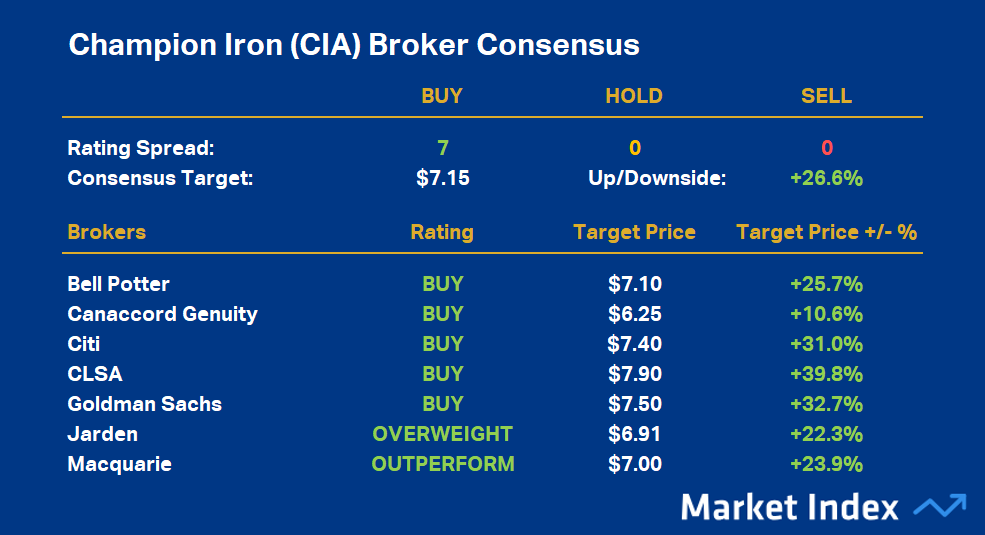

It’s likely this is why our two biggest iron ore producers in BHP Group (ASX: BHP) and Rio Tinto (ASX: RIO) are so highly rated. I won’t do the Broker Consensus readouts for both in favour of the highest rated ASX iron ore stock – Champion Iron (ASX: CIA), but note that both BHP and RIO presently have a highly commendable Broker Consensus rating of +0.70.

%20Broker%20Consensus.png)

Champion Iron (CIA) is the highest rated ASX iron ore stock (click here for full size image)

%20Broker%20Consensus.png){kind=link}

CIA’s broker consensus rating is +1.0, resulting in a Broker Consensus Rating of BUY. Its Broker Consensus Target is $7.15. This suggests brokers collectively believe the stock is around 26.6% undervalued based upon the closing price on Wednesday, 18 December of $5.65. (Note: BHP’s Broker Consensus Target is $45.93 and RIO’s Broker Consensus Target is $130.01)

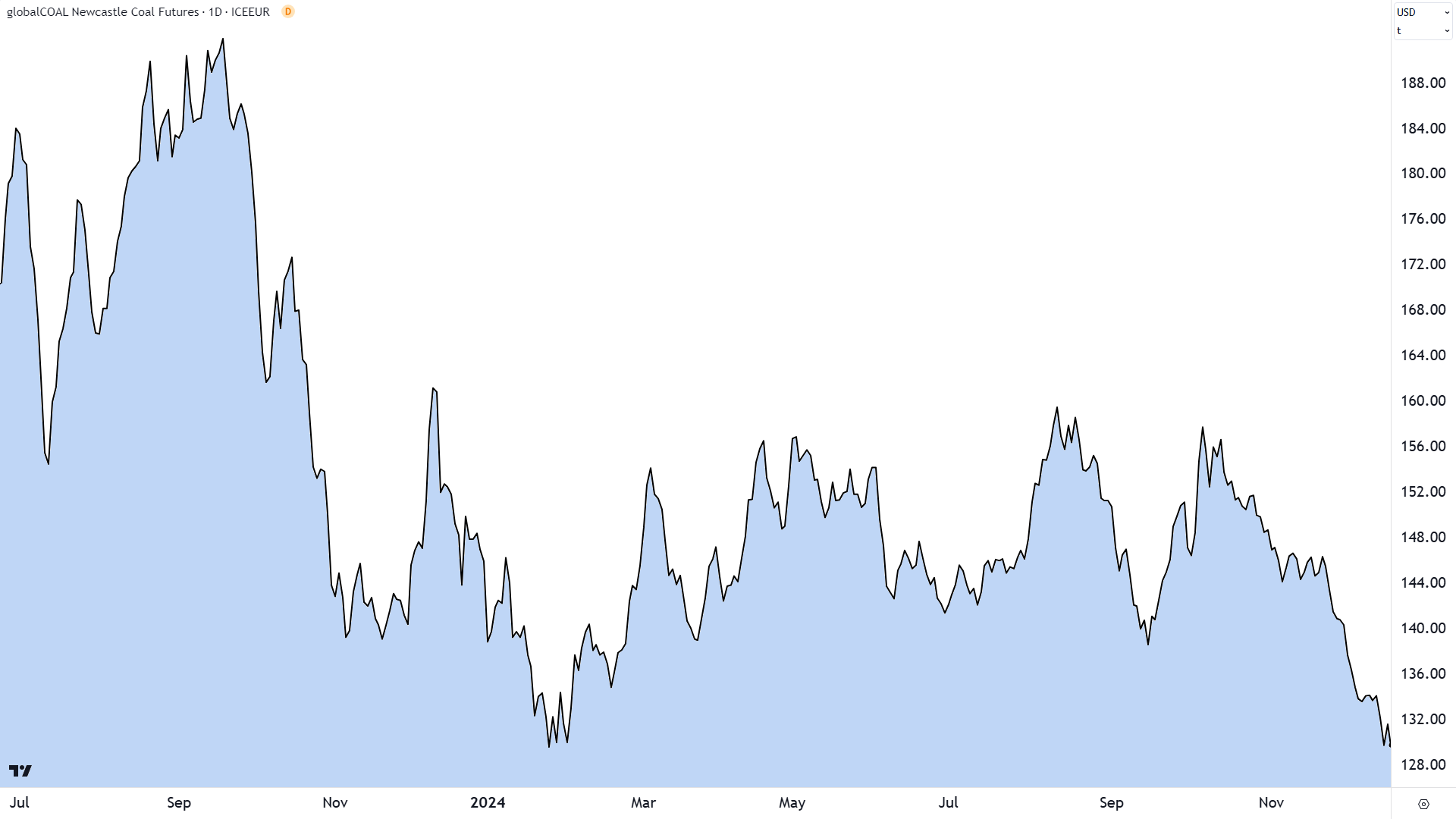

Coal - Burnt out

Coal market and outlook

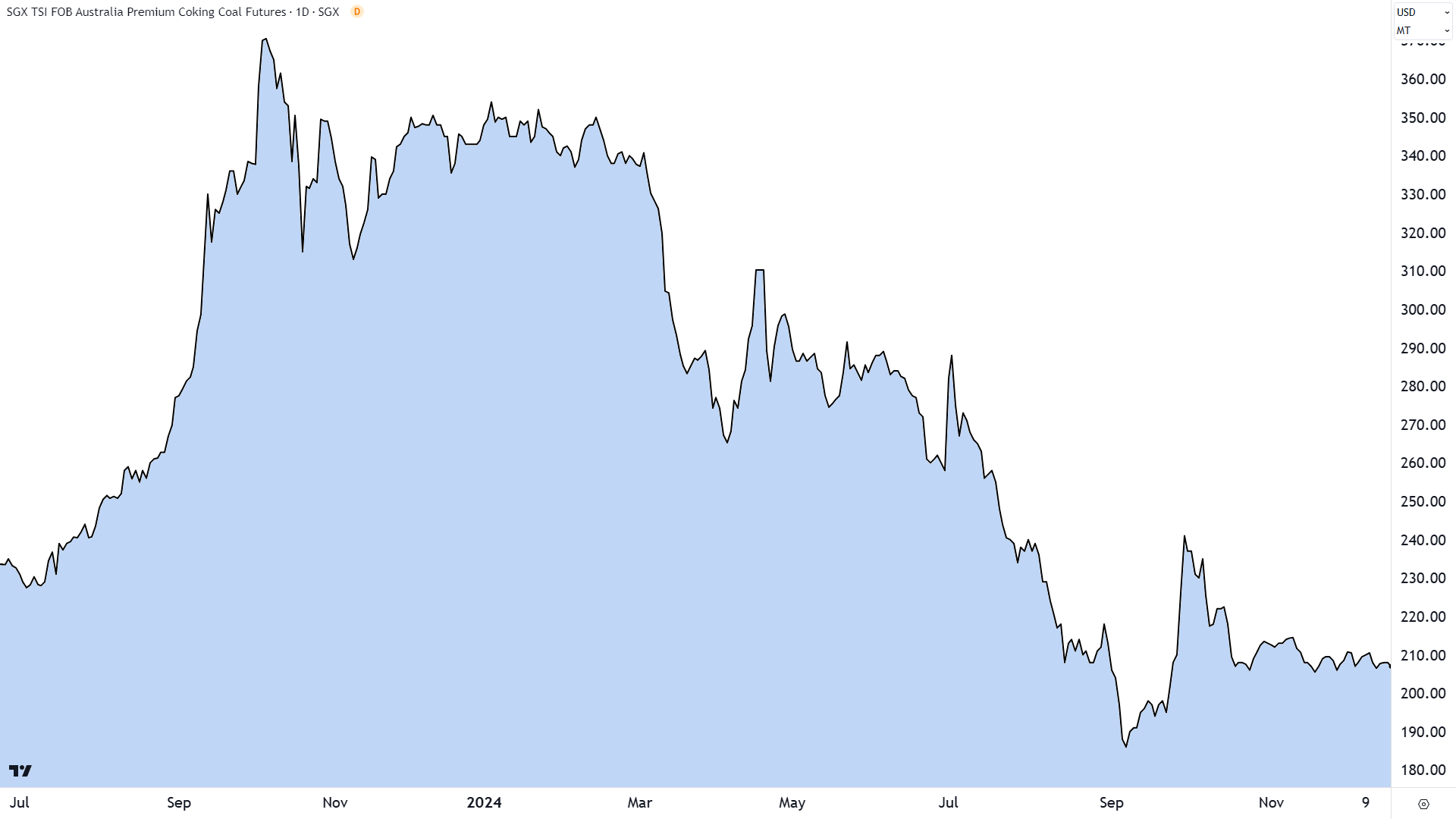

One can’t talk about iron ore without also considering metallurgical (or “coking”) coal. The two are the key components of steel production. It’s perhaps then no surprise that the coking coal chart looks very similar to the iron ore chart – with one exception – the post September rally appears to be fizzling out.

Morgan Stanley blames recent weakness in coking coal prices on prevailing weak demand from steel producers through most of the year, including disruptions to key Indian producers due to that country’s elections. On the supply side, the broker points to increased production coming out of Mongolia.

According to Citi, improving demand from India and a pickup in infrastructure spending there and in China, should support coking coal prices in a range between US$210-$220/t in 2025 (versus the current price of US$208/t). Morgan Stanley’s 2025 coking coal price target offers even less upside at US$209/t, but this does improve to US$223/t in 2026.

%20SGX%20price%20chart.%20Source%20TradingView.png)

%20SGX%20price%20chart.%20Source%20TradingView.png){kind=link}

The other critical coal variant for Australian coal stocks is thermal coal. The benchmark Newcastle contract has seen one of the most sustained declines of any commodity since most of their prices peaked after Russia’s invasion of Ukraine in 2022.

%20(Front%20month,%20back-adjusted)%20ICE%20price%20chart.%20Source%20TradingView.png)

%20(Front%20month,%20back-adjusted)%20ICE%20price%20chart.%20Source%20TradingView.png){kind=link}

One may think falling thermal coal prices are a function of the global pivot towards carbon-free sources of energy production, but this is not the case, suggests Morgan Stanley. The broker points out that whilst decarbonisation trends are growing, China’s imports of thermal coal have risen 80% in the past 2-years.

They’re “showing no sign yet of peaking out”, says Morgan Stanley, who notes new official contract guidelines for 2025 are likely to “further boost import volumes”. This, along with “tight” gas markets, should help drive stronger thermal coal prices heading into 2025, the broker notes.

These factors, along with upcoming peak winter demand, moved Morgan Stanley to this week raise its thermal coal price forecast for 2025 to US$135/t from $US129/t. An improvement, but only slender upside from the current price of US$131.50.

The demand picture is improving, but the market remains well supplied and Chinese thermal coal inventories “appear quite healthy for now”, Morgan Stanley notes.

Which ASX coal stock makes the Magnificent 7?

This one was particularly straightforward. With 11 out of 11 buy-equivalent ratings, Whitehaven Coal (ASX: WHC) deserves its title of highest rated ASX coal stock heading into 2025. FYI, WHC was well ahead of rival New Hope Corporation (ASX: NHC) which presently has a hold-equivalent Broker Consensus Rating of +0.29.

%20Broker%20Consensus.png)

Whitehaven Coal (WHC) is the highest rated ASX coal stock (click here for full size image)

%20Broker%20Consensus.png){kind=link}

WHC’s broker consensus rating is +1.0, resulting in a Broker Consensus Rating of BUY. Its Broker Consensus Target is $8.84. This suggests brokers collectively believe the stock is around 39.8% undervalued based upon the closing price on Wednesday, 18 December of $6.32.

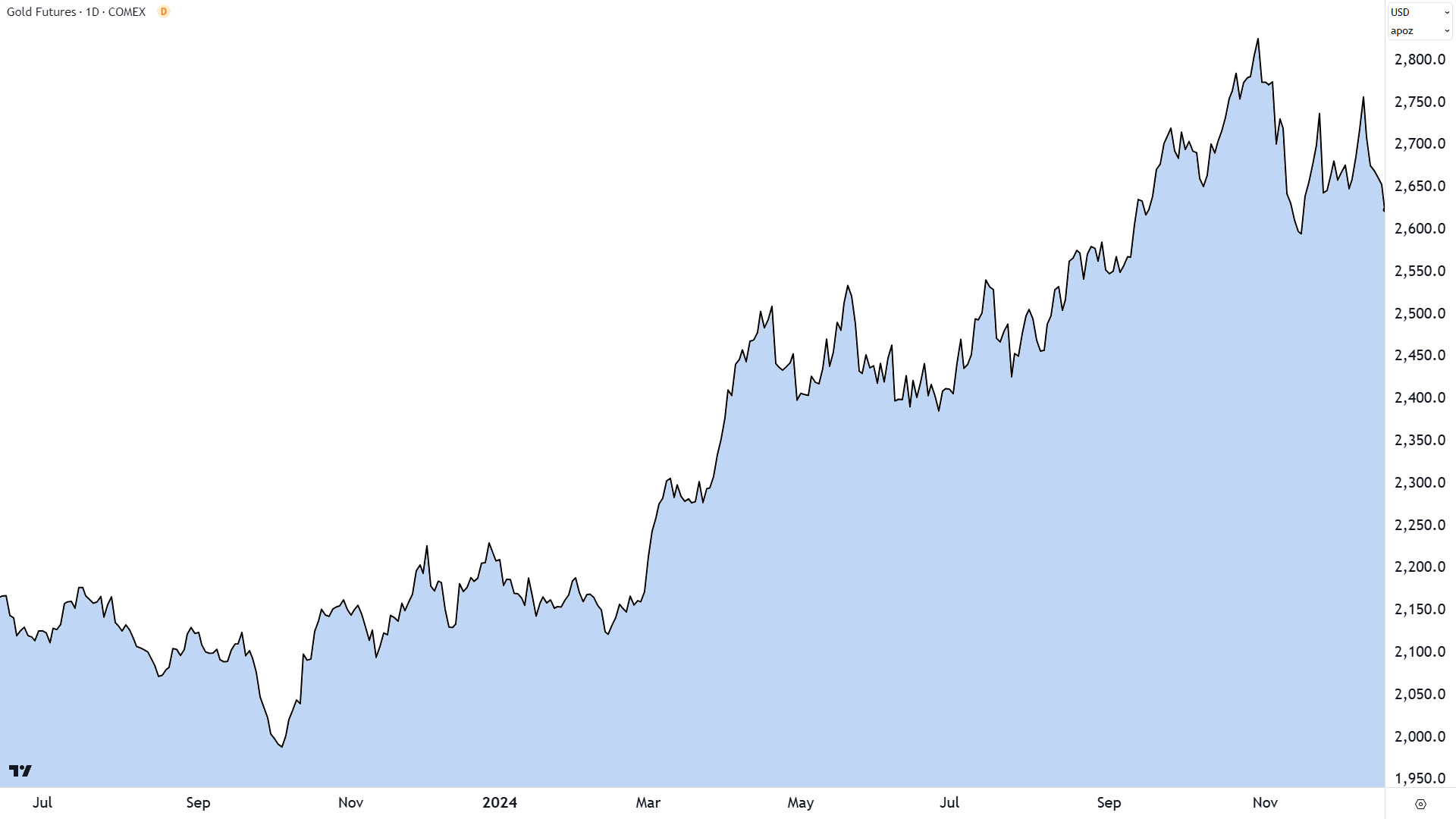

Gold - Bumped by Trump

Gold market and outlook

All this 2024 commodities doom and gloom is enough to get an Aussie mining investor down. But thankfully, there was one commodity – a perennial favourite among Aussie mining investors – that shot the lights out in 2024. It is of course, gold.

%20COMEX%20price%20chart.%20Source%20TradingView.png)

%20COMEX%20price%20chart.%20Source%20TradingView.png){kind=link}

Gold was riding high until the end of October on strong investor and central bank buying. On the first source of demand, Chinese investors have been snapping up gold over the last 18-months as it's viewed as a relative haven compared to their ailing stock and property markets.

On the second source of demand, central banks have also been big net buyers of gold due to broad “de-dollarisation” trends. This refers to the growing desire among central bankers to diversify their exposure away from the US dollar, increasingly viewed as a risky bet given the US government’s spiralling public debt.

But as you can see from the above chart, the gold price turned sharply in early November. What happened in early November? The US election! The Trump + Red Sweep as it has come to be known was widely considered the worst-case scenario for the gold price as it triggered a surge US dollar, and it removed significant uncertainty surrounding the potential fiscal policy path in the USA over at least the next two years.

Longer term, most brokers I’ve read research from believe gold’s recent weakness will be short-lived. Most agree that the US election should result in greater risks around US debt levels, and lead to greater inflation – both typically considered positive for the gold price.

Canaccord Genuity is one such bullish broker, who notes that just this week we’ve seen news the PBOC is back to buying gold. Further, US inflation continues to be hotter than expected, and US fiscal deficits continue to widen – up a staggering 64% from a year ago.

Canaccord points out that US government spending has returned to levels not seen since the pandemic, and before that, not since other emergency spending periods such as the wake of the GFC in 2009-11, and during the 1982 recession. (Hmm…Just asking for a friend – what’s the emergency now?)

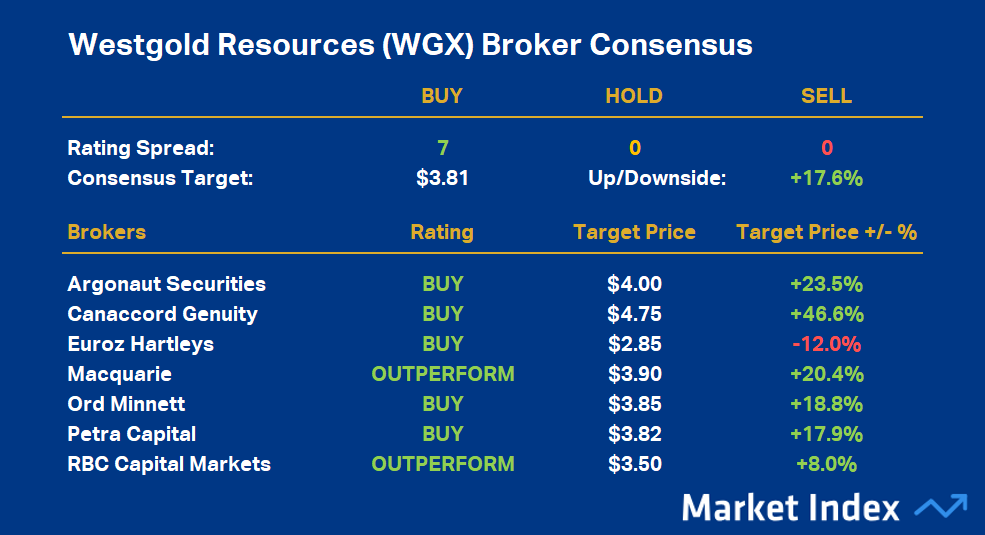

Which ASX gold stock makes the Magnificent 7?

This was a much closer race compared to the other commodity categories. The title of highest rated ASX gold stock heading into 2025 goes to Westgold Resources (ASX: WGX). Its perfect Broker Consensus Rating of +1.0 pipped out near-perfect ratings from Capricorn Mining (ASX: CMM), Perseus Mining (ASX: PRU), and Ramelius Resources (ASX: RMS).

%20Broker%20Consensus.png)

Westgold Resources (WGX) is the highest rated ASX gold stock (click here for full size image)

%20Broker%20Consensus.png){kind=link}

WGX’s broker consensus rating is +1.0, resulting in a Broker Consensus Rating of BUY. Its Broker Consensus Target is $3.81. This suggests brokers collectively believe the stock is around 17.6% undervalued based upon the closing price on Wednesday, 18 December of $3.24.

Conclusion

Well, that's your Magnificent 7 of commodity stocks – one for each major commodity Aussie investors love to follow. It was a tough year for many of the stocks on this list with the exception of gold miner WGX. It's fair to say, though, that the fortunes of the stocks mentioned here closely tracked their respective commodity.

So the question of whether each stock can live up to the brokers' lofty expectations in most cases – I mean we're talking an average target price upside of the Magnificent 7 of 58% – depends on how commodity markets fair over the next 12-months. Clearly from the outlooks I have presented here, it could be a similarly rocky ride for ASX mining stocks in 2025.

There are many moving parts to the global economic picture, both in terms of threats (tariffs and simmering geopolitical tensions) and opportunities (generally falling official interest rates and the prospect of meaningful economic stimulus in China).

From the research reports that come across my desk each day, I get the feeling most brokers feel the ASX Resources sector is oversold, and that it generally represents good value with respect to historical norms. Investors will clearly need to either keep the faith if they are already invested, or watch attentively for a signal to buy if they're not.

One thing is for sure, you'll want to bookmark this page and refer to it often in 2025!

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl has a passion for technical analysis and has taught his unique brand of price-action trend following to thousands of Aussie investors.

........

Investing is risky. Inevitably you will endure losses. If you can't cope with losing, don't invest.

Never miss an update

Get the latest insights from me in your inbox when they’re published.

5 topics

15 stocks mentioned

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl...

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl...

Comments

Comments

Sign In or Join Free to comment