A Bodaful Amount of Value

Alkane Resources (ALK) is an Australian focused gold mining and exploration company who’s four key assets comprise the Tomingley Gold Operation (TGO), the rare earths project referred to as ASM, equity investments, and the Boda porphyry prospect.

My view is that at current prices investors are roughly paying fair value for TGO, ASM & the equity investments and receiving Boda as a free option. Given Boda could potentially be worth $1b+ in its own right this presents as an attractive risk-reward opportunity.

Boda – Key Value Driver

Whilst the positive backdrop for gold prices is favourable for ALK (and just about any other gold miner), the delineation of the Boda porphyry prospect is the key value creation driver which I believe can see ALK deliver outsized gains relative to other gold stocks over a longer-term horizon.

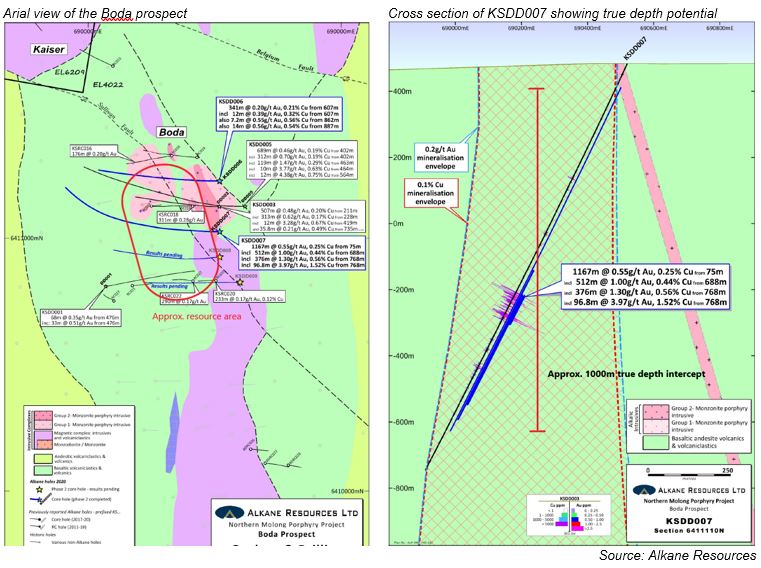

ALK has continued to deliver great results from the gold rich Boda porphyry discovery just southwest of Dubbo, NSW. The most impressive hit of the assays released under the current exploration program was from drill hole KSDD007 (100m south of discovery hole KSDD003), which intercepted 1,167m at 0.55g/t and 0.25% copper.

Whilst the northern step out hole KSDD006 did not look as flattering at first glance, the mineralisation is consistent with the outer halo of the porphyry. It could either suggest the strike is pinching off to the north (worst case) or that the deposit starts to curl under at depth rather than continue at surface, which will require further depth testing in the follow up drill program later this year.

The remaining 2 drill holes in the initial exploration program, both ~100m southern step outs, are awaiting assay results and are due this month. The company has stated that these drill results have intercepted mineralisation consistent with prior assayed holes.

When it is this early in the exploration piece, it can be very hard to determine the size and grade of the ore body, particularly when there are key assays yet to be released, let alone ascribing a specific value. As a mental exercise, assuming the remaining results are consistent with those delivered to date, the Boda porphyry could shape up to be between 191Mt to 502Mt covering rough dimensions of up to 500m (L) by 400m (W) by 1000m (D) on this first pass drill campaign. I note the high-grade core still hasn’t been found yet, which would likely only improve the quality, economics and value of the deposit even if it is found at a materially deeper point. These rough dimensions are illustrated from the aerial and cross sections provided by the company.

Even though it is quite early in the piece, you’re probably still asking “What is this worth?” as it is an important answer to determine how compelling the investment opportunity may be. It is hard to work out with a high degree of certainty this early in the delineation of a deposit. What I can say is that if the above dimensions are somewhat accurate of the deposit and overall grades are no worse than those indicated in the assays, then Boda could be worth comfortably $1b+. However, I reserve the right to be grossly wrong to both the up and downside.

A better way to approach this question would be to work out how much you are paying for the exploration risk when buying ALK shares. For this, a Sum-of-the-Parts (SotP) valuation is most practical. Key notes about the other assets are:

- At TGO, ALK has done material exploration in surrounding tenements areas and is on track to identify ~1Moz of additional resources (~500koz to 600koz of reserves to potentially be converted) to put through the plant in CY21. With the potential to upgrade the plant to process 1.5Mtpa (from current max ~1.2Mtpa), which is allowed under the original operating permits, TGO has the potential to be producing ~90koz p.a. for 6yr+ at an AISC of under $1250/oz. A project of this scale and cost would have an EV of ~$0.66/sh.

- ASM will be spun out mid-2020 via an in-specie distribution to shareholders. The project has proven to be marginal despite the scale given REE pricing, however, research into improved flowsheets could change this. Whilst it would be great to see success in that regard, ASM is just worth the stub value of $0.09/sh.

- The company also has small holdings in GMD and CAI, which are worth ~$0.02/sh combined.

The sum of these three assets is an EV of ~$0.77/sh versus the current EV of $0.595 (@$0.73/sh. ALK is ~$0.14/sh net cash). As the SotP EV of these three assets is greater than the current EV of ALK, Boda has an effective EV of -$0.17/sh. An investor is getting paid to find out if it is a small but decent and economic porphyry deposit or if it is on track to be another Cadia East.

The following are the key catalysts to track to ensure the thesis is on track and to drive the share price over the medium-term:

- San Antonio maiden mineral resource, due April 2020

- Assay results for the last two holes for Boda, due April/May 2020

- In-specie distribution of ASM in mid-2020

- Infill drill program at TGO to delineate reserves at the Roswell and San Antonio deposits, 2H CY20

- Second phase drill program for Boda, due to commence late 2H CY20, with results expected to run into early CY21

- Mining and production ramp up of TGO, due late 1H CY21

With ~$78m of cash on hand, no debt and existing production from TGO (~30koz p.a. @ AISC ~$1350/oz), ALK is well funded to deliver increased and highly profitable production at TGO and turn Boda and surrounding targets into swiss cheese to determine the scale of NSW’s next porphyry precinct.

In summary, this is what I call a Bodaful amount of value on offer as I believe ALK’s prospects are overlooked by many investors. Whilst fortune favours the brave (or so the saying goes), it can be difficult to take on conviction positions in an economic and market environment that has a wide range of potential outcomes. However, given a 2 to 3 year horizon, I believe it is hard to lose on ALK, if in the short-term one can:

- Handle the potential for further gold equity and broader market volatility;

- Handle the share price going materially lower if gold & gold stocks go through another liquidation event alongside a further decline in equity markets, and/or;

- Hedge the position by shorting a low quality gold stock in the event the broader gold thematic doesn’t play out as expected, thus capturing the ‘through-the-cycle’ value from success at Boda.

Disclaimer: Any information contained in this article is limited to general information only, whilst the opinions and views detailed are those of the author only, and as such does not constitute advice or a recommendation in any capacity. The information contained in this article has not taken into consideration your specific financial needs, goals or objectives, so please consider consulting a licenced adviser before considering acting on this information.

The author owns shares in ALK at the time of publishing.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Joshua has worked as an Investment Analyst across different verticals of the financial sector for 10+ years. Experience includes equities research (long/short), manager research and multi-asset portfolios.

2 topics

1 stock mentioned

Independent Analyst

Joshua has worked as an Investment Analyst across different verticals of the financial sector for 10+ years. Experience includes equities research (long/short), manager research and multi-asset portfolios.

Expertise

Independent Analyst

Joshua has worked as an Investment Analyst across different verticals of the financial sector for 10+ years. Experience includes equities research (long/short), manager research and multi-asset portfolios.

Expertise

Comments

Comments

Sign In or Join Free to comment