A bright outlook for Japan

Nikko AM

Amova AM

We often read that Abenomics continues to divide people as to whether it is working, and if this policy platform advocated strongly by Prime Minister Abe since his election in 2012 will ever achieve its objective of moving Japan’s economy forward. We believe that Abenomics is working, however we feel that its success cannot be determined by viewing government policy frameworks in isolation.

Global demand is key

For Abenomics to achieve its ambitious targets, it needs to be supported by a larger recovery in global aggregate demand.

In the current environment, we believe that it will be the US – more specifically, the US consumer – that will be the key to further improvements in global demand over the short to medium term.

The US economy appears quite healthy, with GDP growth expected to be between 2-3% this year, unemployment falling to around 4.5% and the recent wage hikes being likely to continue.

As the only developed nation that can effectively increase interest rates, the US Federal Reserve reacted confidently in March by raising its official rate by 25 basis points, the second rise in three months.

Tax reform in the US should also help the US consumer, although the US administration’s protectionist sentiment is likely to create some uncertainty for its key trading partners, such as Japan.

Our view is that the US consumption-led recovery will drive an increase in US trade volumes, which should then lead to export volume rises in Europe, Asia and Japan.

The increasing importance of the consumer in China and India is also worth noting, and we would expect this group to play a vital role in the sustainable growth of the global economy.

The ongoing recovery in Japan

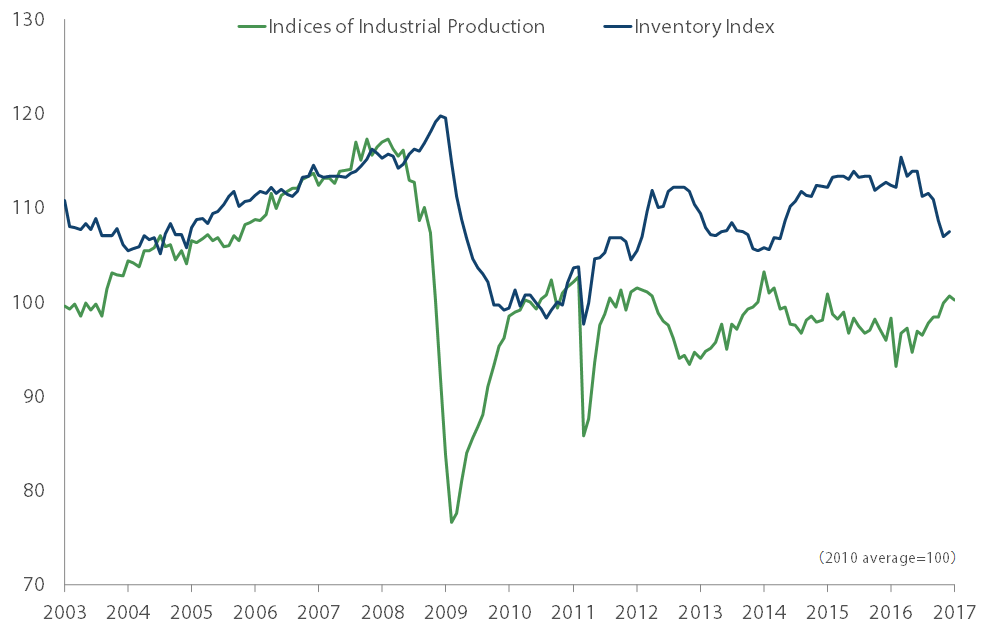

Economic data in Japan is showing signs of improvement, with production and export volumes increasing, and inventory decreasing, albeit still at lower levels than before the GFC (see Chart 1).

Chart 1: Growth in demand is needed

Source: Ministry of Economy, Trade and Industry

While wages have also increased, this has not inspired Japanese consumers to increase spending, which is something we would normally expect.

Such a response has, to some extent, limited the effect of Abenomics, given that household spending and consumption accounts for around 60% of Japan’s GDP. This highlights how important an increase in global aggregate demand is to its success.

That is also why the ongoing improvement in Japan’s corporate earnings is so important, as we expect that corporate capital expenditure will play an increasing role in driving Japan’s economic recovery.

What Abenomics has achieved

It may be surprising to some, however there is data to confirm that Japan is far better positioned now, as a result of Abenomics, than it has been for some time.

As a result of this policy focus from Japan’s strong, well-supported government, we would expect there to be less volatility in markets over the medium to long-term than has been experienced after previous rallies, given:

1. An end to deflation has come into view

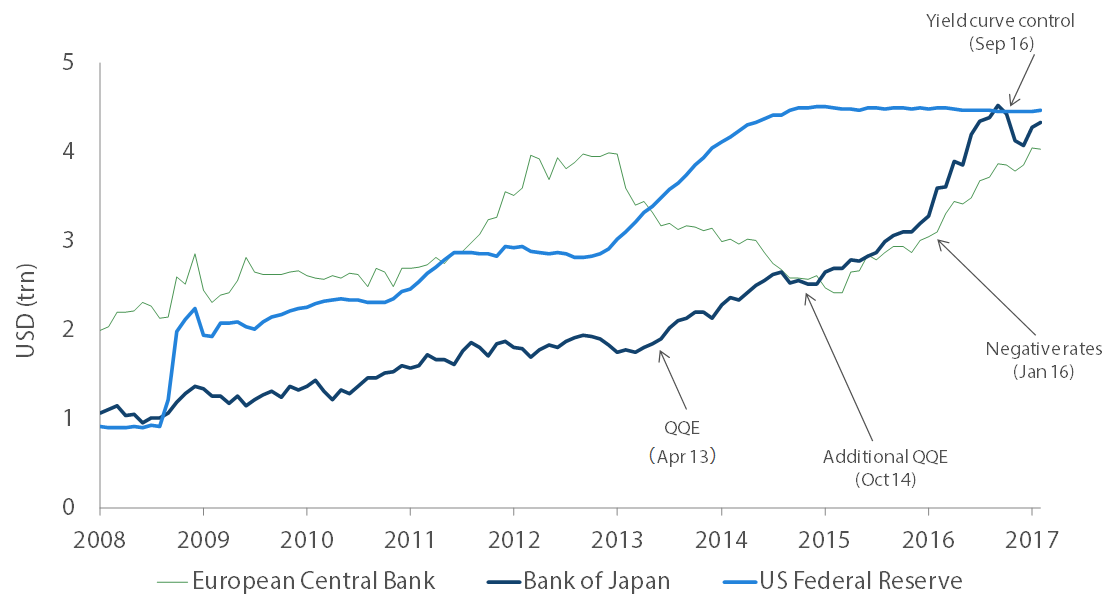

The Bank of Japan’s aggressive quantitative and qualitative easing program, and its focus on a two per cent inflation target, has helped to normalise the Yen, which we believed was too strong given economic conditions.

The BOJ’s yield curve control program, which involves keeping Japan’s 10-year government bond yield at zero, should also help to generate sustainable inflation over the short to medium term (see Chart 2).

The expectation that the BOJ should achieve its inflation target by fiscal 2018 is really important for the Japanese economy and investment markets, as it means the threat of negative inflation that has plagued Japan for decades has faded.

Chart 2: Central bank assets maintained in US, Japan and Europe catching up

Source: Nikko AM based on data deemed reliable. USD transferred by the month-end exchange rate

2. Wage growth should continue

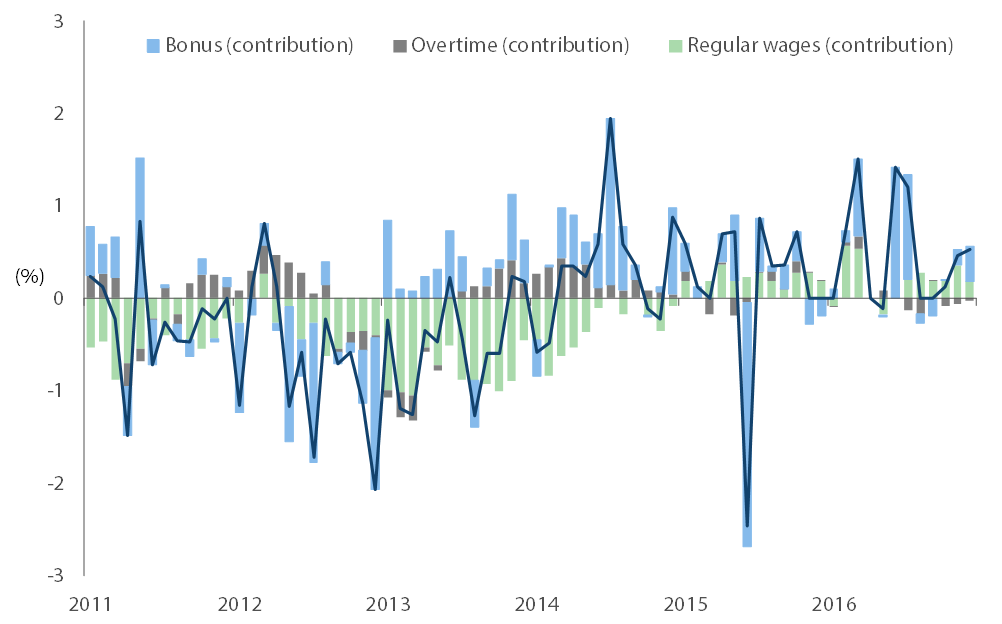

The 0.5% increase in Japanese wages in 2016, the largest increase since 2010, was led by the government, as it continued to encourage employers to raise wages in order to drive consumer spending, and therefore inflation, higher.

Chart 3: Wages growth increases led by the government

Source: Created by Nikko AM based on data from Monthly Labour Survey, Japan Ministry of Health, Labour, and Welfare

Given the uncertain business environment in some industries, however, some companies appear reluctant to raise wages, despite corporate profits being historically quite high. Unions have also preferred to concentrate on protecting jobs, rather than advocating for higher wages.

With this wage growth, and Japan’s unemployment rate now at 2.8% (its lowest level since 1994), we would have expected domestic spending to increase faster than it has.

The positive news is that, in order to harness this wage growth momentum, the government has shown a willingness to implement policies and programs that benefit households directly, in a bid to stimulate domestic consumption.

These measures include offering shopping coupons and travel vouchers, encouraging workers to leave work early and spend money on Premium Fridays, as well as delaying the proposed 10% consumption tax until late 2019.

3. Structural reform is gaining momentum

Structural reform – the Third Arrow of Abenomics – has arguably been the policy’s most successful tenet, as it is the only Arrow that has moved very quickly.

These reforms have driven a major change in corporate attitudes, with greater communication and transparency helping to improve the quality and frequency of conversations that investment managers like Nikko AM have with Japanese corporates.

New overseas investors have also introduced local investors to a more activism-based approach to investing, while many listed companies have employed Corporate Governance Officers to communicate with institutional investors, something that has been well-received.

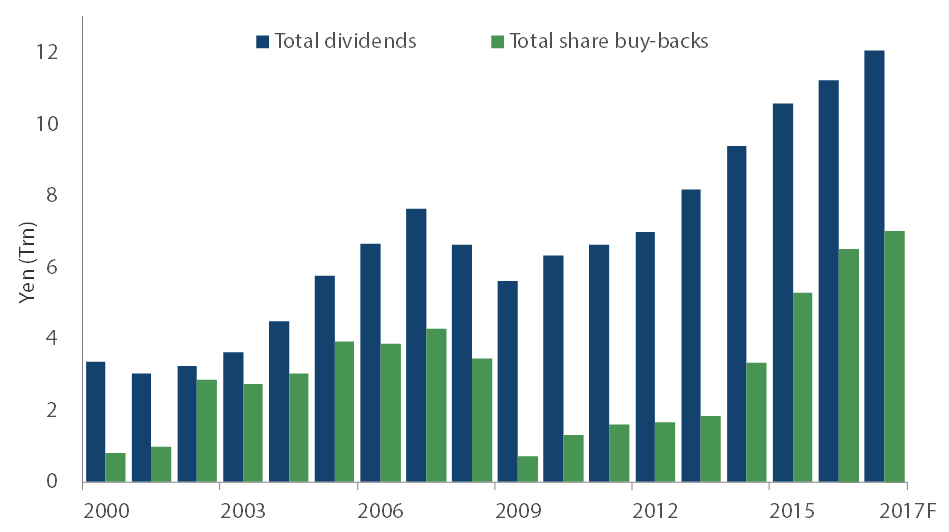

Evidence of this better communication between corporate management and investors is highlighted by the increase in shareholder returns and share buybacks, which has helped to strengthen the ‘earning power’ of Japanese corporates (see Chart 4).

Chart 4: Better communication has led to better returns

Source: Created by Nikko AM based on data deemed reliable

As a result, there is now a serious movement from domestic investors to continue pushing forward with these reforms which, in my time in the finance industry, is certainly a first.

The opportunity for investors

We believe that the Japanese government’s move to more inflationary policy settings presents a range of interesting opportunities across different sectors.

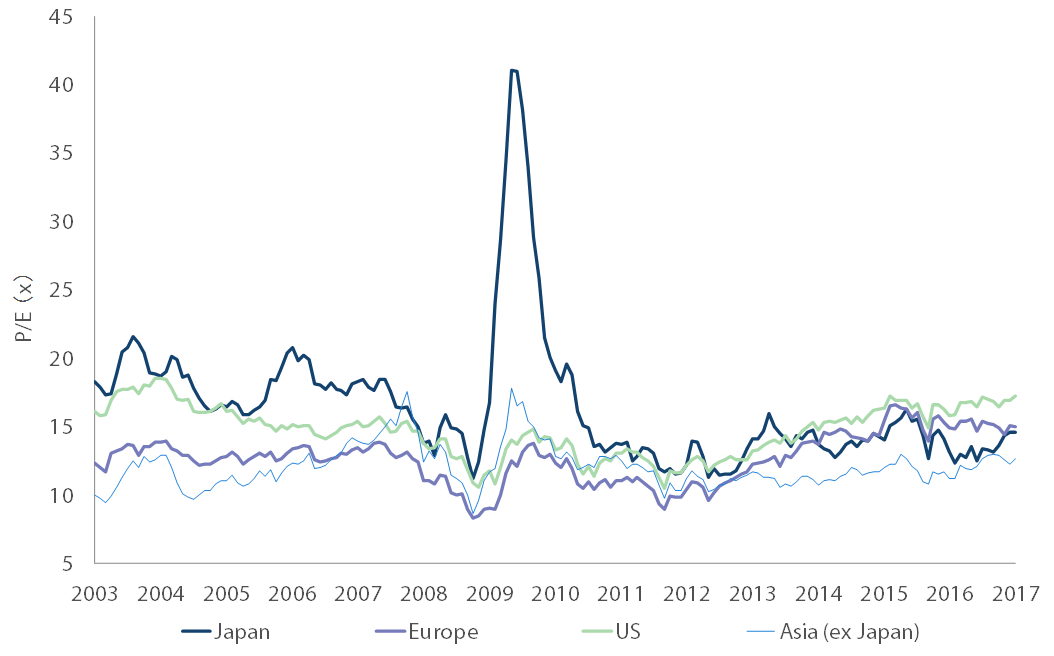

Chart 5: Japanese valuations are attractive

Source: Stock price indices: Japan – Tokyo Stock Price Index (TOPIX), Europe –

Stoxx Europe 600 Index, US – S&P 500 Index, Asia (excluding Japan) – MSCI AC Asia ex Japan Index. All Indices based on local currency, except for the Stoxx Europe 600 Index, which is based on the Euro.

These governance reforms have also encouraged corporate management to stop seeing market share as the most important metric, instead focusing on the real drivers of shareholder value, such as product mix, margin expansion and net profit.

Many Japanese companies are also adopting more ESG-related policies and practices within their operations, with evidence now suggesting that the better the ESG score, the better the performance.

A bright outlook for Japan

We believe that Japan’s economy is likely to continue its above-trend growth, as ongoing improvements in domestic consumption and corporate capital expenditure help to strengthen its underlying fundamentals and reduce the likelihood of significant volatility.

The continued growth of the global economy, especially the US and China’s portion, should also benefit Japan’s net trade performance, while the positive momentum around corporate governance, along with a weaker Yen, should help to drive corporate earnings growth higher.

Japanese equity valuations are currently attractive, relative to Europe and the US, especially as corporate earnings forecasts continue to rise on the back of a renewed focus on corporate earning power.

In this environment, we believe that quality, undervalued companies in Japan with exposure to structural growth drivers present a constructive opportunity for investors with a medium to long-term investment horizon.

Access more insights from Nikko AM here:

Advisers: (VIEW LINK)

Individuals: (VIEW LINK)

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Nikko Asset Management is one of Asia’s largest asset managers, providing high-conviction, active fund management across a range of Equity, Fixed Income, Multi-Asset and Alternative strategies.

In April 2021, Yarra Capital Management acquired Nikko Asset Management’s Australian business and assumed responsibility for the distribution of Nikko Asset Management’s funds in the Australian market.

4 topics

Nikko AM

Amova AM

Nikko Asset Management is one of Asia’s largest asset managers, providing high-conviction, active fund management across a range of Equity, Fixed Income, Multi-Asset and Alternative strategies. In April 2021, Yarra Capital Management acquired...

Expertise

Nikko AM

Amova AM

Nikko Asset Management is one of Asia’s largest asset managers, providing high-conviction, active fund management across a range of Equity, Fixed Income, Multi-Asset and Alternative strategies. In April 2021, Yarra Capital Management acquired...

Expertise

Comments

Comments

Sign In or Join Free to comment