A busy year for takeovers

Despite continuing equity market volatility and ongoing geo-political uncertainty (both domestically and overseas), corporate activity again remained elevated towards the end of 2018 as an array of Australian businesses were either subject to takeover announcements or sought to raise capital to fund their own growth initiatives.

NZ online classifieds business Trade Me Group (TME) was sold to UK-based Apax Partners for ~NZ$2.56bn following a brief bidding war from rival US bidder Hellman & Friedman. Listed vet clinic and pet store roll-up Greencross (GXL) accepted a $675m offer for the company from private equity player TPG Capital, while intellectual property law firms Xenith IP (XIP) and Qantm Intellectual Property (QIP) agreed to a $285m merger. After an exceptionally challenging few years, discount retailer The Reject Shop (TRS) even garnered corporate interest this month, with Pact Group founder Ruffy Geminder offering $78m for the company via a private investment vehicle.

The prevalence of more financial-orientated acquirers (versus traditional trade buyers) across corporate transactions is interesting and possibly reflects the increasingly large amounts of capital inflows into private equity investment strategies in recent years. With more capital globally seeking to find avenues for a suitable return (and access/cost of capital continuing to sit at generational lows), one would expect this activity to continue to remain prevalent. The proposed $2.4bn acquisition of bulk grain handler Graincorp (GNC) in early December perhaps adds another dimension to this – the bidder being a newly established consortium of buyers with no previous joint ownership of assets and an intention of funding the acquisition entirely out of debt (with no immediate plans to divest any assets to service the outstanding liabilities). For a business that can experience highly cyclical earnings, the structure does appear somewhat aggressive and market cynics might suggest that some of this activity is reminiscent of later-stage market activity.

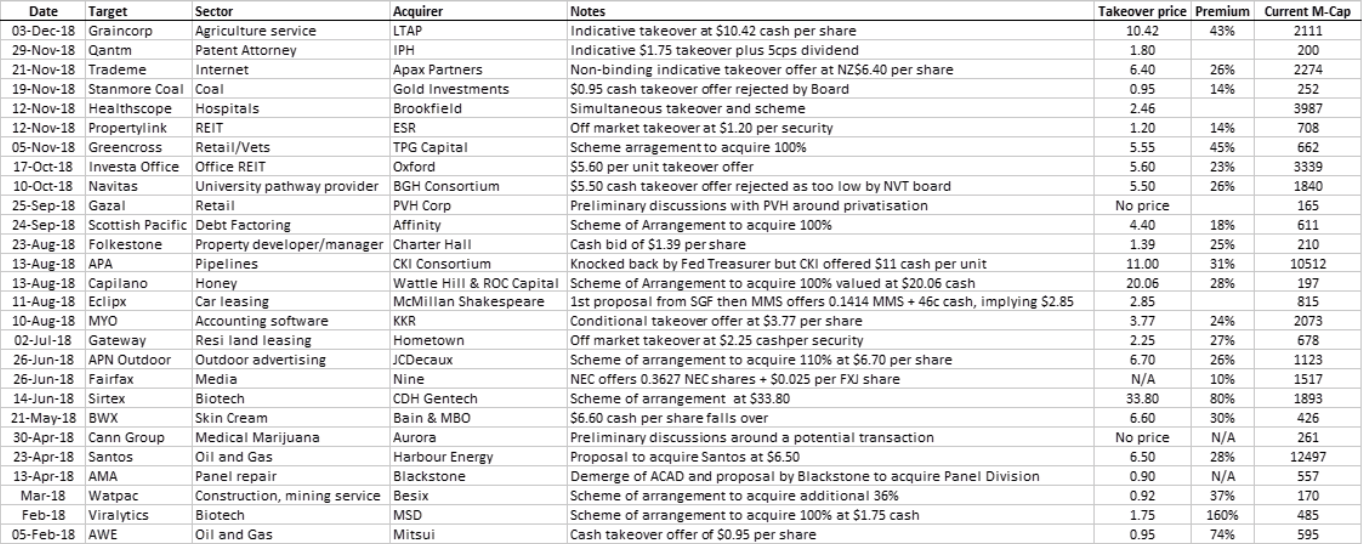

Major Announced Takeovers for CY 2018

Source: Wilsons Advisory

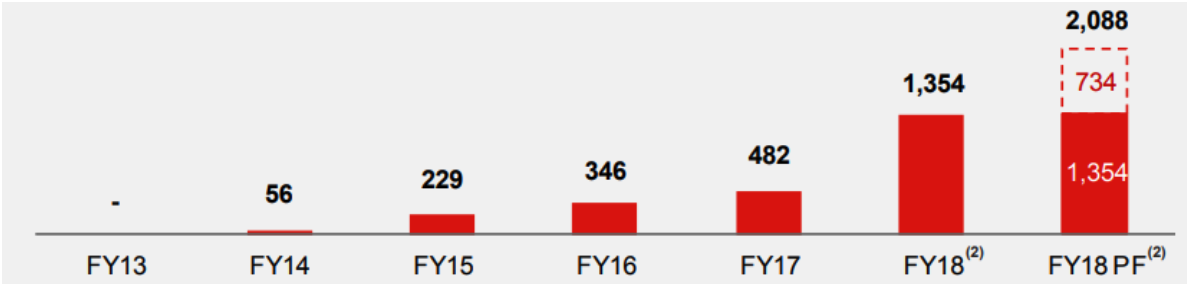

Webjet (WEB) announced a $153m entitlement issue to fund the $240m acquisition of Dubai-based business-to-business (B2B) accommodation provider ‘Destinations of the World’ (DOTW). Operating throughout the Middle East, Europe, Asia Pacific and the Americas, the business connects hoteliers with travel agents, tour operators and third-party wholesalers. Fitting nicely into WEB’s existing B2B business ‘WebBeds’, the acquisition cements Webjet’s position as the second largest provider in B2B globally, taking the business’s directly contracted hotel inventory from ~23,000 beds to ~28,500, or a +24% increase. Total transaction volume (TTV) processed by the WebBeds B2B group, inclusive of Destinations of the World, will now exceed $2.0bn on a pro forma basis.

Total Transaction Volume (TTV) – WebBeds FY13 – FY18 (Pro-forma)

Source: Company presentation

Pleasingly, the DOTW acquisition is expected to deliver ~$14m in additional annualised synergies ($10m per annum in revenue synergies via cross-selling within the WEB’s existing network and $4m per annum in cost synergies via centralisation of corporate costs, headcount reduction etc) to the broader Webjet Group. As an additional sign of confidence in the combination of the two groups, the vendors of the DOTW business also opted to take $28m of the consideration of the sale directly in WEB shares.

We like executive remuneration structures that are closely tied to shareholder outcomes and, where possible, also encourage senior executive management to have a meaningful amount of personal investment within the business on equal terms as their underlying shareholders. In this regard, we also took great comfort in Webjet CEO John Gusic personally sub-underwriting a portion of the retail component of the entitlement offer, resulting in his acquiring an additional 1.2m shares in the business post the acquisition (equating to a personal investment of a further $13.8m in the company).

Perhaps as another example of current equity market sentiment (and despite the business also reiterating its forward earnings guidance for FY19), the share price reaction to the acquisition proved relatively subdued. A comparable deal (with similar levels of co-investment from key management and insiders) in more buoyant markets would likely have resulted in a share price move well into the double-digits – this, however, is the opportunity for investors in the current market and we have been happy to join John in increasing our exposure to the business.

Similarly, Mineral Resources (MIN) produced one of the more interesting deals, agreeing to sell a half-share in its Wodgina lithium project to battery metals giant Albemarle (NYSE: ALB) for $A1.58bn. The deal certainly raised eyebrows given the Wodgina asset itself was only purchased by Mineral Resources in mid-2016 as a then- mothballed tantalum mine from Global Advanced Metals for less than $100m. Quite incredibly, the implied valuation of the Wodgina asset by the Albemarle deal (~$A3.16bn) equated to the entire market capitalisation of Mineral Resources at the time of the announcement (essentially ignoring the additional iron ore and mining services businesses that currently generate some ~$500m in EBITDA per annum).

While the share price of the business was well supported following the deal, the potential upside was somewhat impacted by an earnings downgrade announced by the business at the time of the acquisition as a result of timing delays in ramping up production across the company’s iron ore and lithium assets. While the causes of the downgrade look largely transient in nature, the current environment inevitably means greater focus is weighed to the negative, no matter how short term. Hence, despite the incredible deal value, the MIN share price only appreciated +6.5% for the month – a fairly tepid response to a deal that provides the business with significant funds for further expansion and diversifies the business away from one had become a large lithium exposure.

In a similar vein to the Webjet experience, those closest to the business haven’t allowed current market conditions to curb their enthusiasm, with the company seeing a substantial investment from company insiders post the deal: non-executive director Tim Roberts acquired $30m in new shares over the final weeks of November (via a private investment company) at an average price of $14.80. We have been similarly happy to look through the near-term earnings slip and were delighted that the market had allowed us an opportunity to purchase additional shares post the transaction without having to pay a significant premium.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Andrew has over 15 years’ experience in portfolio management of listed companies, stockbroking and economic analysis. Prior to co-founding Ophir, Andrew worked from 2007 to 2011 as a portfolio manager at Paradice Investment Management.

6 stocks mentioned

Andrew has over 15 years’ experience in portfolio management of listed companies, stockbroking and economic analysis. Prior to co-founding Ophir, Andrew worked from 2007 to 2011 as a portfolio manager at Paradice Investment Management.

Expertise

Andrew has over 15 years’ experience in portfolio management of listed companies, stockbroking and economic analysis. Prior to co-founding Ophir, Andrew worked from 2007 to 2011 as a portfolio manager at Paradice Investment Management.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Volatility creates opportunity to buy great companies at attractive prices

Auscap Asset Management

Equities

This recently triggered market signal has never failed to predict gains

Ophir Asset Management