A contrarian play on the aged care sector

Tim Hannon

Conrad Capital Group

"We're focussed on valuing the business rather than just the stock. Underlying that is our estimate of private market value, which is what an informed, rational investor would pay for the entire company" ~John Rogers, investor, philanthropist and founder of Ariel Capital Management

The Aged Care Industry

The aged care industry provides a non-discretionary, essential service to the community. It provides accommodation, clinical care, meals and living services to the elderly who can no longer live unassisted.

There are about 900 aged care operators in Australia, operating 2,700 facilities. These facilities hold about 200,000 beds, which are generally fully occupied by residents that stay on average two to three years. The average size of a facility is 60 beds, employing 110 people.

The industry is highly fragmented with 600 operators only owning one aged care facility.

Over 2018, the industry was hit by significant budget cuts by the Government. Then at the end of 2018, ABC’s Four Corners launched an investigation into poor treatment of the elderly in aged care homes.

In response to these revelations, a Royal Commission into the sector was announced. The terms are wide-ranging to allow the Commissioners to investigate current quality and safety issues along with determining how best to deliver care in future. The interim report is due in about six months’ time, on the 31st October 2019.

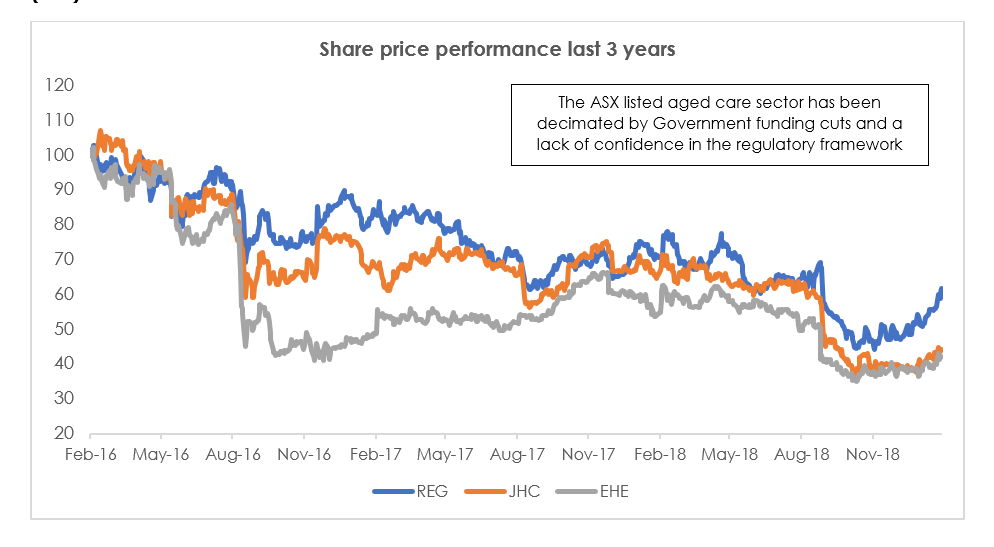

These three events have decimated the listed aged care operators. Over the past two years Japara Healthcare (JHC) has fallen 60%, Regis Healthcare (REG) has halved, and Estia Healthcare (EHE) is down 70%.

In this note we will provide a high-level background to the industry and how it operates. We will then discuss how the incidents of poor resident treatment are likely to be extremely isolated and not representative of the sector. We will then make the case that the most probable outcome from the Royal Commission is increased regulatory certainty and funding to the sector to improve staffing levels and consequently lower risk of poor resident care.

Finally, we will illustrate the case for investing in the aged care sector, despite the risks and uncertainty. We note strongly that an investment in the aged care sector at this point of time is a higher risk proposition. Being contrarian can mean owning shares that exhibit high degrees of volatility, and bad news (even if it is expected) can cause short term capital losses

“Value investing is a large-scale arbitrage between security prices and underlying business value”

Seth Klarman, US investor and hedge fund manager

Industry Fundamentals

With a stable regulatory environment, the residential aged care sector offers investors exposure to a sector with highly defensive earnings supported by attractive demographic trends through an ageing population. Australia’s population over 85 is forecast to double over the next 15 years with this demographic characterised by higher rates of chronic disease and increased reliance on specialised care services.

The growing elderly population together with increasingly complex care requirements provide strong structural support for the residential aged care industry.

The capital requirements are significant

On the back of this demographic tailwind, we have reviewed numerous studies that suggest over the next ten years 80,000 more places, are required to meet aged care demand.

The capital requirement is substantial, approximately $2 billion per annum over the next ten years. The other consideration is many existing facilities need refurbishment. Half of the facilities in Australia are more than 20 years old, the Government estimates 90,000 beds need substantial upgrading, adding to the required capital spend.

“The Aged Care Financing Authority puts the total bill at $30 billion over the next decade”

To put this capital requirement into context, the current Government spending on residential aged care is $12 billion. From a capital markets perspective, the three listed players, Regis Healthcare (REG), Estia Health (EHE) and Japara Healthcare (JHC) have a combined market capitalisation of around $2 billion.

When these three companies listed on the ASX early 2015, the equity market viewed them as the conduit for private capital to fund the required supply of aged care facilities.

Since then, policy instability, funding cuts and now a Royal Commission into the sector have destroyed any confidence equity capital markets had in the sector. It will require the Government to create a stable and supportive regulatory framework so private capital markets can invest in the sector to fund the impending demand requirements.

“The extent of government funding remains unclear and this will continue to be problematic until there is clarity”

CLSA Note, November 2017

The Regulatory Environment

We expect the Royal Commission will conclude the aged care sector is chronically underfunded and inefficiently run. These will likely be the explanations for accounts of unacceptable care levels.

The average aged care sector operator earns wafer-thin margins, with many losing money. We expect the Royal Commission may see the finger pointed at Government funding cuts for insufficient staffing levels and isolated cases of poor care. This is when it becomes a political issue.

This may be the reason behind the curious timing of the Federal Government’s surprise announcement this month of a $662 million increase in aged care funding.

“You can’t repair the aged care system while you’re cutting funding at the same time”

Bill Shorten, Head of the Labor Party and likely future Prime Minister

Requirement One - Funding for aged care needs to increase

The first step to improving care levels is ensuring there are enough well-trained staff relative to the number of residents.

The industry has a solid base to build on, employing 360,000 registered nurses, personal care attendants, and other various health professionals.

The 2017 Aged Care Workforce Report from the Department of Health found that these aged care employees are well trained and highly committed to working in the sector.

“The sense of fulfilment gained from knowing that they were making an important difference to the quality of the lives of older people was a further important aspect of job satisfaction for the workers interviewed”

Most aged care employees work in the sector because they genuinely want to help people. There are millions of interactions between aged carers and residents every day, and most of them are positive.

While the examples of neglect revealed by the Royal Commission will create strong emotional reactions, the fact is they are highly isolated and do not represent a systemic problem of low morale and neglectful care:

“Findings from the previous aged care worker surveys indicated widespread job satisfaction amongst the home care and home support workforce”

We expect the Royal Commission may recommend increased requirements for staffing levels in the industry, particularly more registered nurses. There may also be a requirement for increased pay for aged care workers.

These increased staffing costs must be supported by Government funding. This is because such a large proportion of the aged care industry does not have the resources to bear these increased costs without Government assistance. The average profit per bed in an aged care facility is approximately $3,000. When you consider the cost of building a bed of nearly $300,000, you can see the problem. A return on capital of just 1% not enough for private capital to enter the sector and build the aged care facilities for our growing elderly population.

Requirement Two - Monitoring of outcomes and productivity must improve

We believe the second recommendation of the Royal Commission will be the implementation of technology and monitoring capabilities.

The Royal Commission recommendations will likely suggest implementation of practice management solutions, replacing legacy paper-based systems and information technology.

The other key recommendation will be the implementation of far more advanced monitoring of resident health via wearable technology, with the outputs monitored by healthcare professionals as well as family members.

Let’s summarise the outcome:

Our view is the Royal Commission will:

- Recommend increased funding to the sector with changes to staffing ratios and greater transparency in how funding is being utilised. There may be the recommendation that wealthier Australians contribute more to their aged care costs - a user pays model.

- Seek monitoring of care outcomes and argue for the use of technology to improve productivity.

The overall imperative is the Royal Commission creates certainty in the regulatory environment. This will provide the private capital markets the confidence to invest in the aged care sector.

What has happened to the listed aged care operators?

With a review of the aged care industry and a better understanding of the likely outcomes from the Royal Commission, we can now review the investment metrics of the listed aged care operators.

The reason for the fall in capital value by the listed aged care operators:

- Revenue has been flat because of government funding cuts

- Costs of labour and materials have been increasing by 2-3% per annum

- Margin contraction has ensued driving substantial earnings downgrades

- The threat of potential draconian Government regulation stemming from the Royal Commission

- Lower occupancy due to negative media coverage

As we stand now, the three listed aged care operators trade on price earnings multiples of 15-16 times, have reasonable balance sheets and pay 5-7% fully franked yields.

There is likely to be continued earnings volatility over the coming months on the back of Royal Commission headlines and potentially weaker than expected profit results on the back of lacklustre occupancy rates.

Our playbook

This is how we see the next three years playing out for the listed aged care operators:

1: Regulatory risk removed - The Royal Commission increases funding to the sector. This may mean a minor earnings benefit for the listed aged care operators, but more importantly, it creates regulatory certainty

2: Productivity Improvements - The listed operators will have the scale to invest in technology to improve care levels and raise productivity

3: Growth via development - The listed operators continue to generate growth from development of aged care facilities. The development of an aged care facility by an experienced operator can generate a return on capital of 12-15%. This will create economic value for all listed operators and ensuing share price performance.

4: Growth via acquisition - The next major driver is the ability for the listed operators to grow by acquisition. We have highlighted the fragmented nature of the aged care industry. The Royal Commission findings will no doubt increase compliance costs that will see many operators exit the industry. This will create acquisition opportunities for the listed operators. If they can buy assets at discounted prices, it will create value.

Valuation

To highlight the valuation potential in the sector, we will review Japara Healthcare (JHC). On our estimates, JHC arguably has the greatest opportunity for productivity improvement.

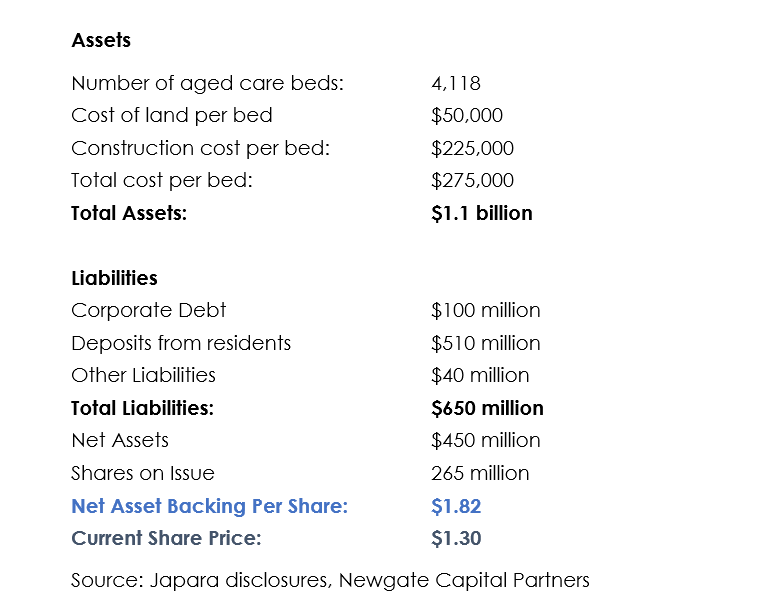

First, we will show you that JHC is trading well below the replacement cost of its asset base. This is a rare event for a company that owns hard assets such as land and buildings with low balance sheet risk. These numbers below are rounded and the balance sheet simplified, but it demonstrates that JHC trades at a 30% discount to its asset backing.

If the JHC share price trades up to the replacement cost of its physical assets, there is nearly 40% upside from its current share price.

The playbook for JHC

Illustrating that JHC trades below the replacement cost of its assets is not enough to drive share price performance. JHC will begin to perform once:

1: The regulatory environment becomes known and benign

2: Occupancy levels improve

3: They execute successfully on their development pipeline

4: They exhibit capability in acquisitions

5: The company delivers on productivity improvements

If we see these five outcomes, JHC’s share price will likely over time trade at a premium to its book value. A share price of $2.50 over the next two years is possible if our playbook is delivered, nearly twice the current share price.

A clear left field event is a takeover of JHC by a private equity group. This is a clear risk given the obvious value on offer and the optionality of the business to deliver on developments, acquisitions and productivity improvements.

Conclusion

The aged care operators have begun rising in capital value after the funding surprise last week, which has the potential to increase earnings for the listed operators of between 15% and 30%. Nonetheless, even after this increased funding, the earnings outlook for the sector remains weak. There is particular risk around occupancy falling lower.

We expect continued volatility as the sector navigates the Royal Commission and the risk of adverse outcome for aged care operators.

We accept that an investment in the aged care sector is a contrarian position, but assess on a weighted average probability outcome, the upside far exceeds the downside on a 12-18-month view.

“If you want to have a better performance than the crowd, you must do things differently from the crowd.”

Sir John Templeton

Lucern Investment Partners

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Tim has 25 years’ experience in the investment and securities markets. Tim was a partner of Goldman Sachs and during his 16-year tenure at the firm had senior experience across all areas of equities investing.

2 stocks mentioned

Tim Hannon

Managing Director

Conrad Capital Group

Tim has 25 years’ experience in the investment and securities markets. Tim was a partner of Goldman Sachs and during his 16-year tenure at the firm had senior experience across all areas of equities investing.

Expertise

Tim Hannon

Managing Director

Conrad Capital Group

Tim has 25 years’ experience in the investment and securities markets. Tim was a partner of Goldman Sachs and during his 16-year tenure at the firm had senior experience across all areas of equities investing.

Expertise

Comments

Comments

Sign In or Join Free to comment