A 'Priceless' investment case

Charlie Aitken

Aitken Investment Management

The great investor Peter Lynch who ran the Fidelity Magellan Fund is often quoted saying: “the best investment ideas you see with your own eyes in everyday life”

I believe this investment research approach remains appropriate today, and potentially more critical than ever, as the rate of change in consumer behaviour increases due to rapid advances in handheld devices, application technology and telecommunication networks (5G).

My advice to investors is to pay close attention to the products and services your children and grandchildren use. They are the early adopters of “megatrends” and also the early “canaries” for traditional business models that are being disrupted.

A megatrend in our everyday life

One of the “megatrends” I believe you can observe with your own eyes is the structural trend towards a “cashless society”. I strongly believe my children won’t use cash and today, we can operate without cash in our wallets.

A classic example I recently encountered was a local café who used to have a “$10.00 minimum” for EFTPOS and “tap & go” card payments. Last week the sign was mysteriously gone and I asked the café owner why? He told me he was losing customers who simply couldn’t and wouldn’t pay for their $4.50 latte any other way, than by card. They had no cash and no intention of getting any cash to pay and were prepared to find another coffee shop that accepts low value card transactions. The lesson is, you can only fight structural change for so long.

Banking on this oligopoly delivering impressive results

Our belief in this megatrend is reflected in the portfolio and we have tested our assumptions with leading US payment and technology analysts, following Q4 results of Visa (V.US) and MasterCard (MA.US). The structural growth dynamics of the industry are worth illustrating.

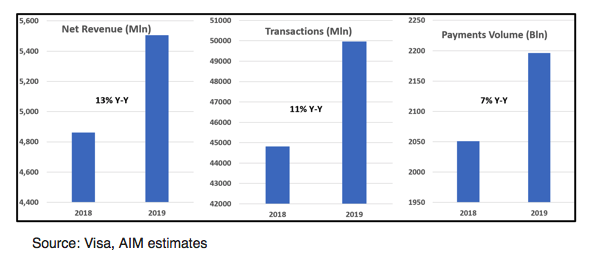

Visa operates in more than 200 countries and facilitates the transfer of value between consumers, businesses, merchants, financial partners, and governments. There are more than 500 million transactions per day on the Visa network and there will be $11 trillion of payments this year. This represents the equivalent of 15% of global GDP.

Whilst these numbers are large on any metric, we believe there is substantial room for continued growth in the medium term. This business is an oligopoly and continues to deliver impressive results, with volumes higher by 11% y-y, net income increasing 17% y-y and earnings per share growth of 21% y-y. The macro and micro tailwinds remain healthy, barriers to entry are high and financial performance, incredibly impressive.

The growth in online transactions and e-commerce is another positive tailwind. E-commerce is growing at 3x the rate on non-ecommerce, largely led by mobile. Mobile payments account for 50% of online transactions and we forecast this to grow 20% each year for the next five years. If this trend continues, card providers like Visa and Mastercard will be clear beneficiaries, as 90% of e-commerce transactions use card. If you purchase anything online, it is highly likely it goes through the Visa and MasterCard platform. MasterCard’s Maestro card (500m outstanding, 20% of stock) has a drawback, as it is not accepted by many online vendors. However customers are transitioning to the traditional MasterCard, which will result in higher usage, margin and profitability.

The B2B market remains dominated by cheque payments. This is a $120 trillion market that could be ripe for disruption. Card payments only represent 1% of volumes and penetration of cards is about 10%. This compares to a penetration rate in the retail market of 45%. A core strategy of MasterCard is to take share in B2B and we think the market may be underestimating the upside. Despite the strong fundamentals and growth outlook, this business is not expensive. MasterCard is valued at 24x earnings and will increase net income by 20% y-y, with operating margins continuing to expand, the company will generate an ROE of 120%.

A cashless society

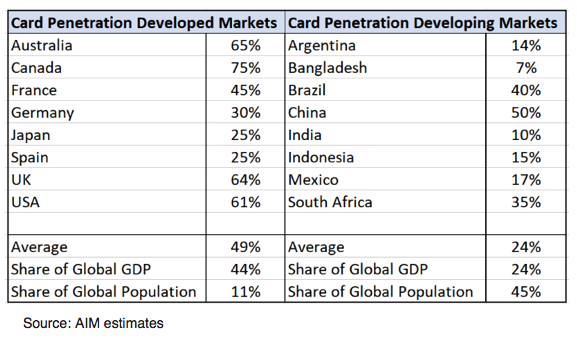

Our analysis indicates that leaders in a “cashless society” are likely to become stronger over time, as more and more people swap cash for card. This is a secular trend. The data below illustrates card penetration as a share of consumer payment volume in both developed and developing markets. There is substantial room for growth across both segments. Only 24% of all payments in major developing markets are conducted on cards. For context, there are $17 trillion of cash transactions, which are subject to disruption from payment providers like Visa and MasterCard. The prize is big. These businesses generate operating margins of 68% and 55% respectively (yes, that is correct), so any customer acquisition is highly profitable.

Over time, much of the growth in the cashless economy will come from developing markets, where an additional 1 billion people are expected to move into the middle class by 2025. More specifically in India, 10% of consumer payments occur on a card today. Visa is the market leader and its business is growing 30% y-y. We expect penetration to continue as it has joint ventures to accelerate distribution through SBI and ICICI, which are two of the largest credit issuers and banks in the country. Even if card usage were to increase 3x in India from current levels, it would still only represent half of the proportional share of usage in the US. As people become wealthier, they will spend on card.

We can’t overemphasize these structural trends and why businesses that are leaders and facilitators of a cashless society are core positions within the portfolio. Further, we don’t think the valuation for these non-credit sensitive businesses are excessive given the growth outlook. Visa, for example, is priced at 23x next year’s earnings. We forecast a total shareholder return of 24%, as management has increased scope for another $8.5bln of buybacks. To put this into context, the S&P 500 earnings growth is forecast at +1% this year.

Next time you buy an aeroplane ticket, clothes online, order an Uber, or buy a coffee, it is highly likely that this payment will be cashless and conducted by a facilitator and technology company like Visa (V.US) and MasterCard (MA.US). We forecast the digital payments sector to increase at a multiple of GDP growth and the key players to continue to grow at a multiple of that multiple. This is genuine structural growth driven by a clear megatrend towards a “cashless society”. We are positioned accordingly in the dominant players who do not take credit risk.

Never miss an update

Stay up to date with the latest news from Aitken Investment Management by hitting the 'follow' button below and you'll be notified every time I post a wire.

Aitken Investment Management employ a high-conviction thematic long-short strategy, investing primarily in listed global equities, as well as selected commodities, currencies and derivatives. For more information please visit our website

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire