A profitable experience with a bitter end

Readers might well be aware of the challenges one of our long-term holdings, alternative asset manager Blue Sky (BLA), has faced since Glaucus, a US based short seller, released a scathingly negative report on the business at the end of March with the company entering into a trading halt over Easter to respond.

Broadly, the report opined that the carrying value of assets in BLA’s underlying funds have been overvalued, flowing through to an over-reporting of the company’s asset under management (AUM) which dictate, almost fully, the company’s ongoing fee revenue. In its response, the BLA Board described the report as “incorrect, fundamentally flawed and materially misleading”.

Firstly some background

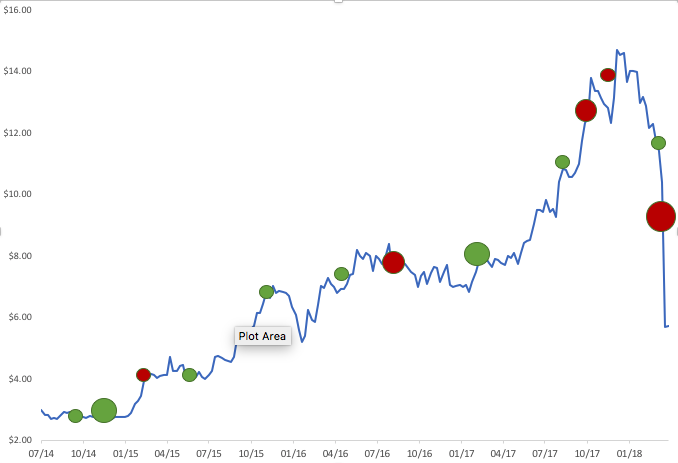

The Cyan C3G Fund made its first investment in BLA back in October 2014, at just $2.80. Since that date, the company reported an enviable set of financial results reflecting a strong and growing business. In FY15, 16 and 17 respectively, the company announced assets under management (AUM) of $1.4bn, $2.1bn and $3.3bn; underlying earnings after tax of $10.4m, $16.3m, and $25m; and paid three fully franked shareholder dividends of 11c, 16c and 23c.

We had engaged with management and staff on more than a dozen occasions through company presentations, investor briefings, product launches, phone hook-ups, along with attending their two day annual investor conference in Brisbane. In addition, we had visited and talked directly with many of their underlying investments. Whilst we will never know everything about a business, we felt that we had a good understanding of the company and we believed in the integrity of the people involved.

As the company proved itself, the Cyan C3G Fund increased its initial position, which added significant value to the Fund as the share price rose. As always, this was managed dynamically and, over the holding period, we adjusted our position more than 10 times. At the time of the Glaucus report being released, BLA was less than 4% of the Fund, less than we had held in the past, but not insignificant. Up until this time, we had no reason to doubt the success of the company. Indeed, none of this negative speculation has yet been proven correct.

However – and this is a big however – we are acutely sensitive to market sentiment and how this can seriously impact stock price movements. There has been no fundamental change to the underlying business in this short space of time, and our opinion on the short-seller research report is not particularly important, because the reality is that the investment thesis has changed due to perception around the company and the market in which it trades.

Thus when the market for BLA’s securities reopened on 4th April, we sold a significant stake immediately (above $8), and continued to sell during the day. Shortly thereafter we had sold our position completely. The price sell-off was dramatic, with BLA falling from $11.50 to as low as $4.50 in 3 trading days.

This is one of the major advantages of limiting the size of the C3G Fund, being able to exit a position when required. Because of our definitive move and manageable fund size, the impact on the Fund of the severe sell-off in BLA has been limited.

To be clear: we will never be able to buy into a stock at the very bottom and sell out at the very top.

Cyan’s Buys and Sells in Blue Sky

We endeavour to discover attractive businesses before the rest of the market and manage the weighting of those positions appropriately as the fundamentals change, new information is released and stock prices move.

Importantly, if significantly negative information is released, we take immediate and decisive action.

Along with finding attractive investments, this is another situation in which we believe we add value – to be vigilantly watching investments and acting definitively when required.

Are we happy about recent events? Of course not. But do we regret ever being invested in the company? Of course not. Because we got in early and managed our holding prudently, our investment in BLA added over 12% to the value of the Cyan C3G Fund over its investment lifespan.

We will get things wrong again. But if we get our good decisions very right, and limit the impact of our bad decisions, we will always end up well in front. We believe our history with Blue Sky (and Bellamy’s, GetSwift, M2 Telecommunications and Vita Group) has proved this.

About Cyan

Cyan is making meaningful investments in some of the most promising (and often overlooked) smaller companies listed on the ASX today. Find out how.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Dean has over 25 years experience in the funds management industry covering all major asset classes. He holds as Master of Applied Finance and is a Graduate of the Australian Institute of Company Directors.

1 topic

1 stock mentioned

Dean has over 25 years experience in the funds management industry covering all major asset classes. He holds as Master of Applied Finance and is a Graduate of the Australian Institute of Company Directors.

Expertise

Dean has over 25 years experience in the funds management industry covering all major asset classes. He holds as Master of Applied Finance and is a Graduate of the Australian Institute of Company Directors.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Investing for the biggest market shift since the GFC

Livewire Markets

Equities

Why ex-20 is the prime hunting ground for ASX returns

Livewire Markets