A simple investing framework

Charlie Aitken

Aitken Investment Management

With the number of headlines hitting the newswires on what feels like a minute-by-minute basis, it’s easy to get lost in chasing data points. Instead, I believe that having a well-defined and broadly applicable framework to assess the long-term outlook of a business as an investment opportunity is very helpful in times like these.

In my previous note I wrote focused on having a framework to assess the big picture; this note focuses in on some more company specific considerations and presents a simplified approach that is hopefully helpful. To make it a bit less theoretical, I also present the framework applied to a real-world example by looking into one of the businesses we added to our fund during the March sell-off: Accenture.

A Simple Framework

If the current period has highlighted anything, it is that focusing exclusively on earnings (and earnings growth) has several shortcomings. The full picture needed to assess an investment opportunity must consider the ability of a business to generate cash flows after working and fixed capital requirements, as well as the appropriateness of the overall capital structure relative to the cash flows generated.

At a high level, I think along four dimensions when evaluating a company for potential investment:

- Quality of the balance sheet and management team,

- Sustainability of the competitive advantage, medium- and long-term

- Growth prospects, and

- Valuation.

Quality has a straightforward definition in my book: is the business conservatively financed? The current crisis has bought into dramatic focus the risk of owning businesses that rely on excessive gearing to generate an acceptable return on shareholders’ equity. Over-optimising a balance sheet can boost shareholder returns in the near-term but proves fragile in a crisis. A business with a ‘just-in-case’ approach to its capital structure wins out over extreme financial engineering in the long run, in my opinion.

This does not imply that I recommend only owning debt-free businesses, but rather to seek out companies that have manageable debt levels and – critically – generate substantial amounts of free cash flow in order to service the debt. This will vary on an industry-by-industry basis, but anything with a net debt-to-EBITDA ratio of 3x or higher is at the riskier end of the spectrum, and requires more work to understand just how sustainable the cash flow profile is during a downturn. (EBITDA has the flaw of ignoring capital investment requirements but using this ratio as a starting point for deciding which companies are worth more work is a good rule of thumb).

Strong governance and a top-notch management team is also an important indicator of quality, albeit a more subjective one, which makes it trickier to assess. Discussing this topic in depth is likely beyond the scope of this note, but if I had to highlight just two measures to consider, look for management teams that act rationally when it comes to allocating capital, and communicate candidly with shareholders about their results of doing so – both the successes and failures.

With regards to sustainability, I refer to businesses that have a competitive advantage that allows them to earn an economic profit over a long period of time. An economic profit is different to accounting profit reported on the income statement, because it measures whether the return on invested capital exceeds the cost of invested capital (which is essentially your opportunity cost).

If there is no sustainable competitive advantage, the ability to earn an economic profit will be eroded over time due to the iron law of economics: excess profits attracts competition, which will see all players eventually earn the cost of capital and no more. A business that repeatedly earns an economic profit has to be in possession of some factor that allows it to fend off the competition: a very good indicator that the company likely has a moat of some sort, justifying further analysis.

When assessing companies for this trait, I prefer assessing the return on invested capital (ROIC) as opposed to the return on equity (ROE). The former measures the return on all sources of capital (i.e. debt and equity) and is arguably a tougher yardstick by which to measure management and their capital allocation record. Put differently, return on equity can be artificially inflated by simply taking on substantial amounts of debt. In fact, given how low interest rates have been over the past several years, many companies have done exactly this. ROIC does a better job of evaluating whether a company earns an economic profit in my opinion. (That is not to say ROE has no value as a signal – just do not look at it in isolation of the ROIC and the gearing).

Regardless of which ratio you choose, keep in mind that the traditional methods for calculating ROIC or ROE uses accounting profits, which can differ materially from cash flows. At a minimum, one should make adjustments that account for the working and fixed capital investment needs of the business. In a pinch, using traditional free cash flow (cash from operations minus capital expenditures) will do, though other derivations of free cash flow (such as free cash flow to the firm) will be more accurate when measuring ROIC. If analysing the ROE, consider using the ‘owners earnings’ approach favoured by Warren Buffett (accounting profit plus depreciation and amortisation, less capital expenditures). In both cases, you may wish to make further adjustments for other non-cash or truly non-recurring items, as appropriate.

There is no hard and fast rule for the absolute level of cash return on invested capital to look for, but I would say any business that can sustainably generate a ROIC of 15% or higher over a very long period of time is of great interest, as it likely indicates the presence of an economic moat.

On the topic of growth, I think in terms of both revenue and free cash flow. For the former, I look for businesses that can generate organic growth that consistently exceeds GDP and inflation, generally in industries that have superior growth prospects to the general economy. It is critical to understand exactly what is driving this superior revenue growth profile (e.g. entering new markets, a secular shift in consumer or business needs, acquisitions, pricing power, volume growth, the strength of the economic cycle, etc.) to evaluate how long it can last.

With regards to free cash flow, spending time on understanding the capital reinvestment requirement of the business is particularly important. If a company aims to create economic value, the capital retained and invested by management must earn an economic profit (ROIC greater than the cost of capital). It may sound counter-intuitive, but there is absolutely such a thing as growth that destroys economic value.

Consider a business with a cost of capital of 10%. If management invests $100 in a growth project, it should at least earn $10 in free cash flow to break-even from an economic perspective. If the return is below $10, the decision to invest in growth has generated an economic loss and shareholder value has been destroyed – despite the revenue, profit and cash flow growth sure to be reflected in the financial statements. This is precisely why understanding capital intensity is so vital.

Look for companies that can reinvest a portion – or all – of their excess economic profits back into the business, and still earn a high return on the capital invested. Over time, this is the surest way for a business to compound shareholder wealth – essentially generating more than a dollar of economic value for every dollar invested.

Finally, valuation cannot be ignored. If you accept that earnings do not tell the full picture because it ignores the reinvestment requirements of a business, then using a P/E ratio has limitations. Instead, consider using the free cash flow yield (free cash flow per share divided by the share price), which can be compared to both other equities and long-term interest rates.

Consider an equity purchased on a free cash flow yield of 6.0%, which equates to a P/FCF multiple of 16.7x (1/6.0%). Assuming one has confidence in the sustainability of the competitive advantage to underpin healthy free cash flow growth over the medium-to-long term, what one has effectively purchased is the ownership of a stream of cash flows yielding 6.0% on the purchase price – but critically, this stream of cash flows can grow ahead of inflation. Compare this to purchasing a government bond with either a 10- or 30-year maturity: a guaranteed return of well below 2% at present, with no chance of growth in the stream of cash flows generated. Any pickup in inflation will mechanically erode the real value of the principal and the annual income earned.

Using the above example, one can debate whether there is a sufficient equity risk premium built into a free cash flow yield of 6.0%; clearly, if one desires a larger margin of safety, just wait for the stock to trade on a higher free cash flow yield.

This valuation approach can and should be supplemented by additional valuation methods, such as a discounted cash flow valuation. It also works better for established business; earlier stage investments that are not yet generating positive free cash flows need to be fully modelled out and a net present value of cash flows calculated. However, as a starting point, I believe the focus on free cash flow provides a more reliable buying signal than earnings, because the former considers the investment needs of the business whilst the latter does not.

By incorporating the four considerations outlined above, the framework presented seeks to identify and own quality sustainable growth businesses, purchased at a margin of safety. While substantially simplified, it is the approach we employ at my firm in evaluating investment opportunities.

Applying the Framework: Accenture

Accenture is a name I would wager most investors would recognise, though likely only as a consulting firm. In reality, consulting comprises a bit more than half of total revenues, with the balance earned from outsourcing.

For most people, the latter conjures up images of highly commoditised services performed at paper-thin margins. In Accenture’s case, this belief is misplaced: many of the outsourcing activities they provide see them effectively assume end-to-end responsibility of certain key business functions for their clients. This includes activities as varied as supply chain management for manufacturers, assuming claims lifecycle management for health care providers, or managing, maintaining and modernising the range of software applications deployed throughout a large organisation. Given the complexity of some of these activities (and keeping in mind how essential they are to the day-to-day operations for many of Accenture’s clients), there is substantial switching cost involved.

On the consulting side, Accenture has built up deep industry- and domain-specific expertise and professional networks, drawing on decades of institutional knowledge to provide an intangible asset that is incredibly difficult to replicate at a global scale.

The challenges posed to large businesses by an ever-changing technological landscape will not diminish, but when adding to that the need for a substantial re-think of global supply chains – particularly in the wake of the US-China trade war and the impact of COVID-19 – we believe the services Accenture offers will remain relevant to its customers for a very long time to come. We assess the business as having very strong competitive advantages, underpinned by the high switching cost and process- and knowledge-based intangible assets developed over many years.

Quality

From a balance sheet quality perspective, Accenture scores very highly. The company has historically operated with almost no debt. As at its most recent quarterly result, the company had US$5.44bn in cash and short-term investments, compared to only US$20mn in debt. Even when including other obligations such as operating lease liabilities and net pension benefit obligations, the company has surplus cash. As a result, we believe the capital structure is robust enough to withstand the inevitable slowdown in revenues and profitability that the coming recession will cause.

As a management team, we believe Accenture has always dealt with adversity and criticism in a constructive fashion, and has been clear in communicating good and bad news with investors. The track record of successful capital allocation rates highly, as can be observed in the economic profit the business has consistently earned for many years.

Sustainability of competitive advantage

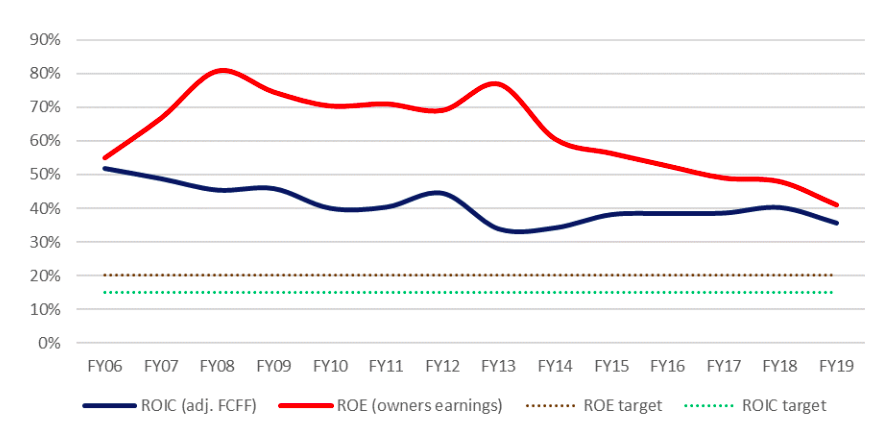

By reviewing the ROIC history and comparing it to a notional cost of capital, we believe we can objectively assess whether the fundamentals confirm our view of the business having sustainable competitive advantages.

The chart below shows the history of returns on capital over the past 14 years. The ROE (using owners’ earnings) and ROIC (using adjusted free cash flow) incorporates the adjustments outlined earlier in the note.

Source: AIM, Accenture company financials

In calculating the ROIC, we make several adjustments to the free cash flow as well as the invested capital to raise the bar. In short, we add back certain expensed items (such as leases and intangible research expenses) in favour of including them in the capital base. We also include the net pension liability in the invested capital (as it is effectively a future economic liability to the firm), as well as any previous goodwill impairments (if relevant). These adjustments generally lower the ROIC.

Even when making these adjustments, Accenture has earned a remarkably consistent cash return on invested capital for an extended period – certainly well above our 15% target ROIC (or 20% target ROE). To us, this is highly suggestive of a business with a deep competitive advantage.

Growth

From a revenue perspective, Accenture has managed to expand its sales by an average of roughly 7% per year over the last 14 years. However, this hides the fact that, due to reporting in US dollars, there has been a persistent currency headwind at play over most of the last decade. The underlying growth has generally been stronger than what has been reported.

This revenue growth has been the product of growing engagements with top-tier clients in both the consulting and outsourcing lines of business. The company has also made several modest-sized acquisitions on a regular basis over the period, which we estimate added between 1% and 3% to sales growth most years. Put differently, we believe that – in a normal operating environment – Accenture can deliver organic, currency neutral revenue growth of around 6% - well ahead of GDP and inflation. That will clearly not be the case this year, where budgets are likely to be reprioritised to focus on the most essential spend items only. In that regard, Accenture’s outsourcing operation should prove more resilient, though it will not be immune.

Ongoing margin expansion, working capital optimisation and declining capital intensity has seen free cash flows grow at a better clip than revenues over the same period: an average of roughly 10%. In fact, over the last five years, the rate of growth for free cash flows has been roughly twice that of revenue.

During the height of the global financial crisis, revenues dropped by 8.5% year over year. However, free cash flow still managed to grow modestly. Given that the current recession will likely see far steeper cuts to IT and consulting budgets, we fully expect free cash flow growth this year to be tepid at best, and more likely somewhat negative. In this regard, we trust management will act prudently in managing operating expenses, as well as the working and fixed capital investment needs of the business.

Looking beyond the next twelve months, we believe the outlook for Accenture’s consulting and outsourcing services will be particularly strong as businesses emerge from the crisis. The need to rapidly adapt to a changing world has arguably never been more immediate. Over the medium term, we believe the business can return to its pre-crisis trajectory of mid-to-high single digit revenue growth, translating to low-double digit free cash flow growth. Our confidence in this forecast is underpinned by our belief in the competitive advantages the business enjoys.

Valuation

Over the last several years, Accenture has mostly traded on a free cash flow yield of between 4% and 5% - an implied P/FCF multiple between 20x and 25x.

During the March sell-off, the implied free cash flow yield got up to roughly 6.2% (implied P/FCF of ~16.1x) - a far cry from the levels seen during the global financial crisis, but significantly cheaper than it has been for some time. Assuming we are correct about the potential for mid-to-long term free cash flows to compound around 10% beyond the next 18 months, we have effectively purchased the right to a stream of cash flows growing much faster than inflation. Compared to the real return that a bond or cash deposit will generate, we think this is very attractive.

The stock – and the market as a whole – has rallied quite sharply from the middle of March, and we are biding our time in for now. However, when supplementing the analysis above with a full DCF-based valuation, we have conviction that even disappointing results over the next few months has only a very modest impact on the long-term value of this high-quality sustainable growth business.

Conclusion

I firmly believe that having tested frameworks and processes to deploy in times of market distress leads to better decision making. The approach outlined above is repeatable and applicable to most equity opportunities, and – though simplified – reflects how we approach decision making on behalf of investors. Hopefully, it is of use or of interest.

As always, I sign off by wishing you and your family safety and good health.

Invest with conviction

Aitken Investment Management is an independent global fund manager that aims to capture long-term secular trends by investing in high quality businesses that can compound in value.

To find out more hit the 'CONTACT' button below.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Featuring