Adding value, not risk

•

Sponsored

Print Wire

Ahead of the Pinnacle 2020 Virtual Summit, we asked two Australian Fixed Income managers to share a chart from their presentation and explain its importance.

Coolabah Capital’s Christopher Joye says investors face an existential challenge in cash and defensive asset classes as deposit rates converge towards zero amid volatile market conditions. This has prompted many investors to rethink their fixed income allocations. But what should their next move be? Metrics Credit Partner’s Andrew Lockhart challenges the old adage of the fixed income market that to generate higher levels on income, you must take on more risk.

The outlook for this asset class is mixed but our experts will ensure you add value rather than risk to your decision-making.

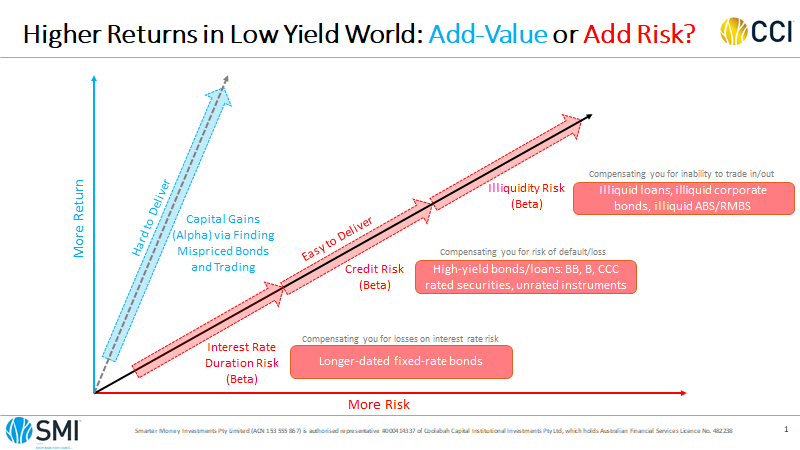

Bond market investors must chase value not yield

Christopher Joye, CIO, Coolabah Capital

Click on the image to enlarge

Investors face an existential challenge in cash and defensive asset classes as deposit rates have converged towards zero. Longer-term interest rates/yields are near all-time lows. As discount rates plummet, the valuations of all investments are being stretched to extreme levels.

This situation is unlikely to change any time soon. So, how do investors get decent returns above and beyond the current rate of inflation - expected to be around 1% to 2% annually? In the bond market there are essentially two choices: add-value or add-risk. Adding value is very difficult. By way of contrast, adding risk is easy.

Investors can chase higher yields by taking on three different forms of bond market risk (or beta). The most obvious is by investing in bonds/loans with higher risks of default and loss.

Virgin’s senior unsecured bonds listed last year were a classic example. They offered a stunning 8% yield for a senior unsecured loan from a well-known brand, but Virgin was unprofitable and highly leveraged. Today the bonds are worthless.

Another option is chasing higher yields by investing in loans facing illiquidity, such as illiquid corporate bonds, and subordinated RMBS/ABS. A third alternative for higher yields is through investing in long-term fixed-rate bonds offering superior interest rates, compensating for the risk of loss if rates rise and the value of these bonds decline.

The harder road is adding value (or alpha). This is what we do and during the Pinnacle 2020 Virtual Summit, I’ll detail our sophisticated systems which allow us to find mispriced bonds that offer capital gains (or price appreciation), not higher yields.

It means constantly revaluing thousands of bonds and actively buying and selling securities that are cheap and liquid, and which are expected to normalise back to fair-value.

The chart above highlights the benefits of adding value. In the current environment we believe this is a crucial consideration for investors – it’s about offering the prospect of safer capital gains (alpha) rendered through genuine skill, not luck.

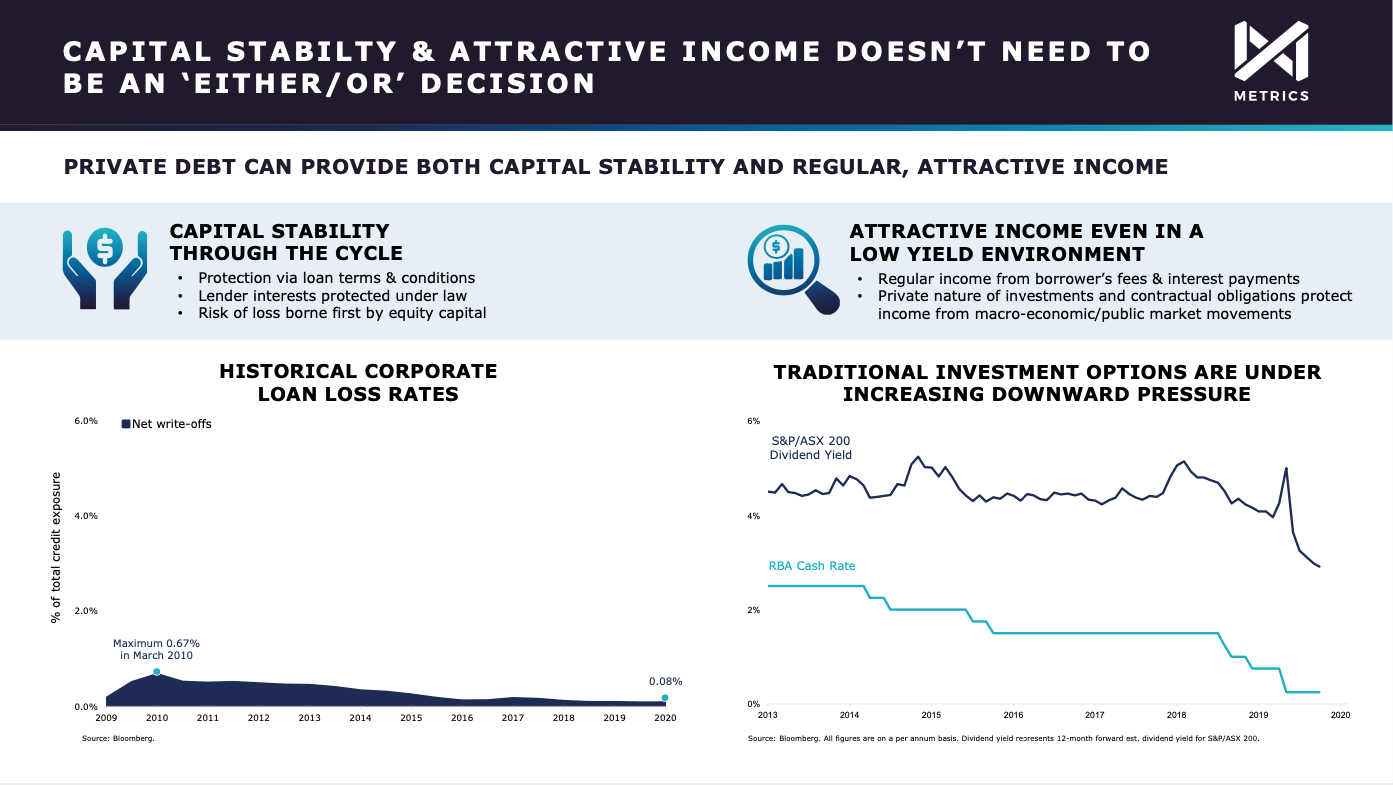

Why capital stability, attractive income doesn’t need to be a trade off

Andrew Lockhart, Manging Partner, Metrics Credit Partners

There is an old adage that still rings true in parts of the fixed income market – to generate higher levels on income, you must take on more risk. At the Pinnacle 2020 Virtual Summit I will challenge this assumption. The slide we’ve decided to share is used to highlight why capital stability and attractive income doesn’t need to be a trade off when it comes to private debt.

Click on the image to enlarge

As Australia’s largest non-bank corporate lender, we provide loans to major Australian corporates for various purposes, such as funding acquisitions, working capital, expanding and purchasing assets (capex), completing infrastructure projects or for commercial property investment, acquisition or development. These types of loans were traditionally provided by big banks. This has changed providing opportunities for non-bank lenders like Metrics to fill the void.

The chart on the left highlights the low risk generally taken in the Australian corporate loan market. Corporate loss rates in Australia are low, and further protections are achieved through a rigorous due diligence process and the negotiation of covenants, controls and security within loan agreements. Also, given where debt sits within the capital structure of a company, all such debt transactions present a lower risk compared with direct equity investment.

The right-hand-side chart illustrates the impact on investment returns from declining cash rates and dividends to equity investors. Traditional investment options have been challenged to generate income as a result of record low interest rates and significant cuts to shareholder dividends. During the summit, I’ll provide my perspective on the outlook for the market and for investors looking to generate higher levels of reliable income and reveal some of the rigorous processes Metrics uses to mitigate risk and reduce capital volatility.

Register for the Pinnacle 2020 Virtual Summit

Volatile market conditions and historic low interest rates have prompted many investors to rethink their fixed income allocations in order to achieve their investment goals. On Friday 18th September, two of Australia’s leading fixed income investors will share insights and argue the case for their unique investment strategies and the outlook for this asset class. Lonsec Senior Analyst Ron Mehmet will host a Q&A session with Andrew Lockhart and Christopher Joye following the presentations.

You can register for the session here, or view the entire event calendar here.

Important Information: Please be advised that the Pinnacle 2020 Virtual Summit is designed for sophisticated investors only

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Livewire Exclusive brings you exclusive content from a wide range of leading fund managers and investment professionals.

........

Livewire gives readers access to information and educational content provided by financial services professionals and companies ("Livewire Contributors"). Livewire does not operate under an Australian financial services licence and relies on the exemption available under section 911A(2)(eb) of the Corporations Act 2001 (Cth) in respect of any advice given. Any advice on this site is general in nature and does not take into consideration your objectives, financial situation or needs. Before making a decision please consider these and any relevant Product Disclosure Statement. Livewire has commercial relationships with some Livewire Contributors.

2 topics

2 contributors mentioned

Livewire Markets

Livewire Exclusive brings you exclusive content from a wide range of leading fund managers and investment professionals.

Expertise

Livewire Markets

Livewire Exclusive brings you exclusive content from a wide range of leading fund managers and investment professionals.

Expertise

Comments

Comments

Sign In or Join Free to comment