Afterpay: What’s a billion-dollar revenue line worth?

We acknowledge Afterpay (APT) has been one of the most talked about stocks in the Australian market. Everyone loves a 20 bagger - which is what Afterpay has been since IPO. Years of investing experience has taught us that such attention and investor enthusiasm often ends poorly for those who join ‘the party’ late. However, we still see significant upside in Afterpay over the next 3 years. Let’s take a look why.

In February, the company revealed a target Gross Merchandise Value (GMV) of $20B++ by FY2022 (see below).

Source: Afterpay 1H19 results presentation

This is an incredible target given:

- APT only did $2.3B of GMV in 1h19 and;

- Management's track record of exceeding expectations

Whilst APT hasn't broken-down the geographic split of this GMV target, our analysis would suggest it doesn't assume any contribution from the UK business. Perhaps the UK is the '++'?

Assuming a successful launch in the UK, the $20B GMV target could be significantly understated. This would see material upgrades to consensus GMV and customer numbers over the next 18 months. Indeed, we think it’s possible that the US business alone could generate close to $20b GMV by FY2022.

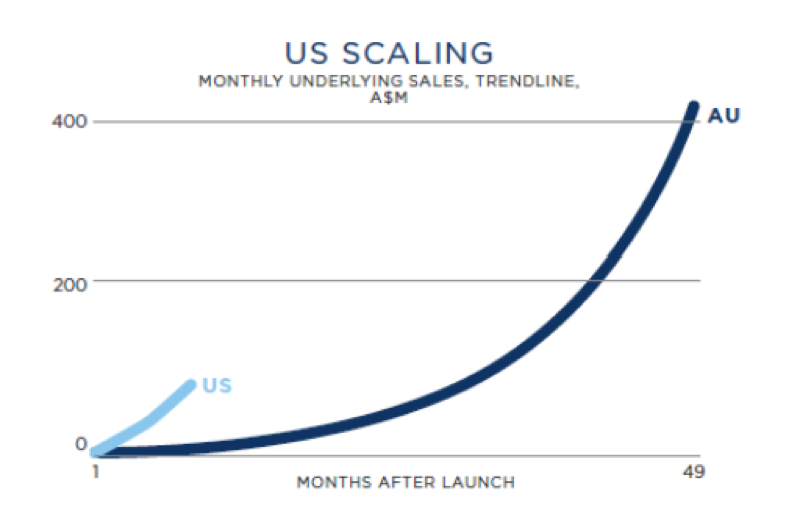

US business traction

The chart below highlights the US is scaling significantly faster than the Australian business did. We think the market is underestimating the implications this has for US GMV.

Source: Afterpay 1H19 results presentation

It is undeniable that the product is resonating with US millennials. One million customers have used the service within eleven months of launch and new customers grew at 4-5k per day in the first two months of the year. We think the US business has passed an inflection point, as the Australian business did, where the value of the product to merchants and consumers increases dramatically with user growth.

If it plays out like it did in Australia, customer growth could accelerate to 10k a day and beyond. This equates to ~3.5m new customers in the US over the next 12 months, a doubling of APT total customer base. To put it simply, the US is scaling roughly 5x faster than Australia, in a market >10x the size.

If we assume APT deliver $25B GMV at ~ 4% merchant fee, then APT will generate $1b of revenue.

APT has also guided to a 2% net transaction margin (NTM) on this revenue, implying $500m of NTM. Assuming $150m of corporate overheads would imply 350m profit before tax or NPAT of ~$250m. Given the growth profile, customer unit economics and global growth opportunity that APT will still have at this point, we would expect APT to trade on a PE of 30-40x. This would imply a market capitalisation of $7.5-$10B or $30-40 a share.

US investors are likely to be the marginal buyers of the stock and set the share price from here. Australian companies that have resonated with US investors have seen significant re-ratings e.g. Altium (ALU) and NextDC (NXT). US investors represent 30-40% of the NXT and ALU share registers. US investors only represent 15% of the APT register today.

What about the Australian business?

The Australian business has been somewhat overlooked in recent times. However, there has been some pleasing developments as the company has entered an optimisation phase here:

- Gross losses have declined to 1.1% of underlying sales from 1.7% (outperforming most traditional credit products)

- Growth in average customer spend per month has risen to $400 from $200

- Percentage of customers transacting each month has doubled from ~20% to >40%

- In store has grown from 9% of GMV in FY18 to 15% in 1h19 (outpacing online growth) and the market opportunity is 8x larger

- NTM has expanded from 2.1% to 2.3%

Recent initiatives

Afterpay has also quietly undertaken the following initiatives recently:

- Launched PLAY (with LayAway Travel), a new travel service with longer and more flexible instalment periods (2-12 months) and higher values. A move into the more traditional layby market.

- Launched cross border transacting which will allow the large Australian customer base to transact with previously inaccessible US retailers via APT overtime.

- Diversified beyond fashion into health, wellness and entertainment

These initiatives will continue to see demographics evolve beyond the millennial cohort and expand the addressable market. The Australian business also provides insight into the earnings potential for the US and the UK when they move into optimisation phase.

A note on the people

With assistance from Matrix Partners, Afterpay has recently hired:

- Director of Engineering at Uber

- Head of Risk Management at Uber

- General Manager of ShopStyle

- Head of Paypal UK

It is rare for an Australian company to attract the calibre of talent that APT has over the last 12 months. Shareholders should take comfort that APT has been building a world-class global team to optimise the company’s increasingly global footprint and deliver on the stated medium-term targets. It’s an endorsement of the product, the opportunity and senior executives/board.

Want to learn more about investing in small caps?

Eley Griffiths have delivered consistent out performance through all market conditions for 15 years. We are style agnostic and can own both growth and value companies to construct portfolios that will outperform. Click the 'follow' button below and you'll be notified as soon as we publish out latest insights on Livewire.

*Disclosure: Eley Griffiths Group Small Companies Fund owns shares in Afterpay

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

David Allingham is a Portfolio Manager at Eley Griffiths Group and has over 16 years’ experience analysing small and emerging companies at Eley Griffiths Group. Prior to joining EGG in 2004, David worked in marketing at EMI Music Australia. David holds a Bachelor of Commerce from the University of Sydney.

Featuring

David Allingham,

Eley Griffiths Group

David Allingham is a Portfolio Manager at Eley Griffiths Group and has over 16 years’ experience analysing small and emerging companies at Eley Griffiths Group. Prior to joining EGG in 2004, David worked in marketing at EMI Music Australia. David holds a Bachelor of Commerce from the University of Sydney.

1 stock mentioned

David Allingham is a Portfolio Manager at Eley Griffiths Group and has over 16 years’ experience analysing small and emerging companies at Eley Griffiths Group. Prior to joining EGG in 2004, David worked in marketing at EMI Music Australia. David...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management