All aboard the risk train

Vimal Gor

Pendal Group

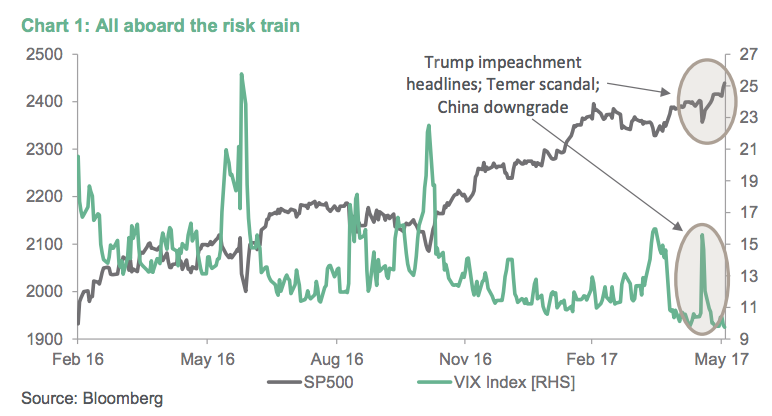

Perhaps to say that there is complacency in the market is too broad a generalisation, it just seems like there are just so many contradictions out there currently. Equities and fixed income markets are saying very different things; while the S+P 500 and VIX are very sanguine, US bonds are rallying which tells of a much more concerning picture, but even here volatility is falling.

As sentiment and expectations continue to gyrate between extremes, the underlying economic data is still playing out in much the way that we had anticipated. I would argue that it is not so much the economic data that have been volatile and unpredictable, but rather the pendulum swings in market moods, coupled with headline grabbing political dramas, which have led to the kind of fake breaks that we saw in May. I have written over the last couple of newsletters about the unwind of the Trumpflation trade, and it seems like this has now been pretty much all priced out.

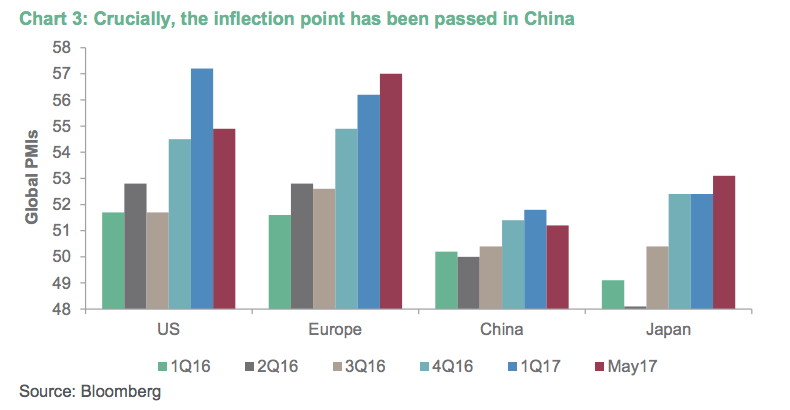

Nevertheless, these are indeed some very confused times for markets, and to complicate matters further, global growth is not in synch. US data continues to disappoint versus high expectations (set by some very strong soft data prints that I wrote about in previous Newsletters), but more importantly the positive Q1 momentum seen out of EM and Asia has begun to wane (as China’s policy tightening starts to bite).

European and Japanese data look to be on fire, apart from the one indicator that everyone cares about the most, inflation. But the GFC has altered the way that the market perceives the balance of risks (the behavioural finance term is pain memory): we now have a tendency to overestimate long term volatility (“it’s all going to crap”), hence placing a heavier weight on downside risks. Also, with the economic green shoots in Europe and Japan being so green, we don’t know if we can trust them yet, or if they can gather enough momentum to offset the potential drag from China and the US.

In last month’s Newsletter I went very deep into the intricacies of Chinese financial plumbing and we got feedback that I lost a few people on the journey, so this month I wanted to step back and take a big picture view. In this note I aim to pull together our current thoughts on China and, given the growth inflection point looks to be clearly behind us, investigate what they mean for the rest of the world’s economies and markets. Access our newsletter here.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Appointed Head of Income & Fixed Interest in June 2010, Vimal is responsible for setting strategy, processes and risk management. He oversees $16.4 billion invested across Income, Composite, Pure Alpha, Global and Australian Government strategies.

1 topic

Vimal Gor

Head of Income & Fixed Interest

Pendal Group

Appointed Head of Income & Fixed Interest in June 2010, Vimal is responsible for setting strategy, processes and risk management. He oversees $16.4 billion invested across Income, Composite, Pure Alpha, Global and Australian Government strategies.

Expertise

Vimal Gor

Head of Income & Fixed Interest

Pendal Group

Appointed Head of Income & Fixed Interest in June 2010, Vimal is responsible for setting strategy, processes and risk management. He oversees $16.4 billion invested across Income, Composite, Pure Alpha, Global and Australian Government strategies.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Funds

The 5 best-performing super funds of the year

Livewire Markets

Equities

Buy Hold Sell: 5 ASX stayers built to go the distance

Livewire Markets