Are record inflows into gold ETPs a problem for precious metals bulls?

Summary

-

Gold prices recently topped USD 1,800 per ounce, with the metal matching its highest ever quarterly close in USD in June.

- Gold exchange traded products (ETPs) have seen record inflows in 2020, with total holdings rising by more than 700 tonnes in the first six months of this year.

- Despite strong inflows, gold allocations at a portfolio level remain modest, and well below historical levels.

- Investor appetite for bullion will be supported in H2 2020 given continued concerns regarding COVID-19, expensive absolute valuation levels for risk assets and negative real yields on sovereign debt.

Full article

Gold investors have enjoyed a stellar 2020, with the yellow metal rising by 16% in USD terms (19% in AUD terms) in the first six months of the year, ending June 2020 trading at more than USD 1760 per ounce.

Gold has continued to move higher in early July, now trading at more than USD 1,800 per troy ounce. Since the cyclical bear market bottom seen in late 2015, the gold price has now risen by more than 70%.

From a demand perspective, the standout feature of 2020 has been the record inflows seen into gold ETPs, with over 700 tonnes of gold purchased via these vehicles in the first six months of the year.

Collectively, investors now own more than 3,620 tonnes of gold, worth more than USD 205 billion, through gold ETPs. That’s more gold than the Bundesbank owns.

The increase in demand seen this year has predominantly been driven by North American investors, though strong growth has also occurred in Europe, Asia and indeed Australia, with Perth Mint Gold (ASX: PMGOLD) for example seeing holdings increase by over 50% since end December 2019.

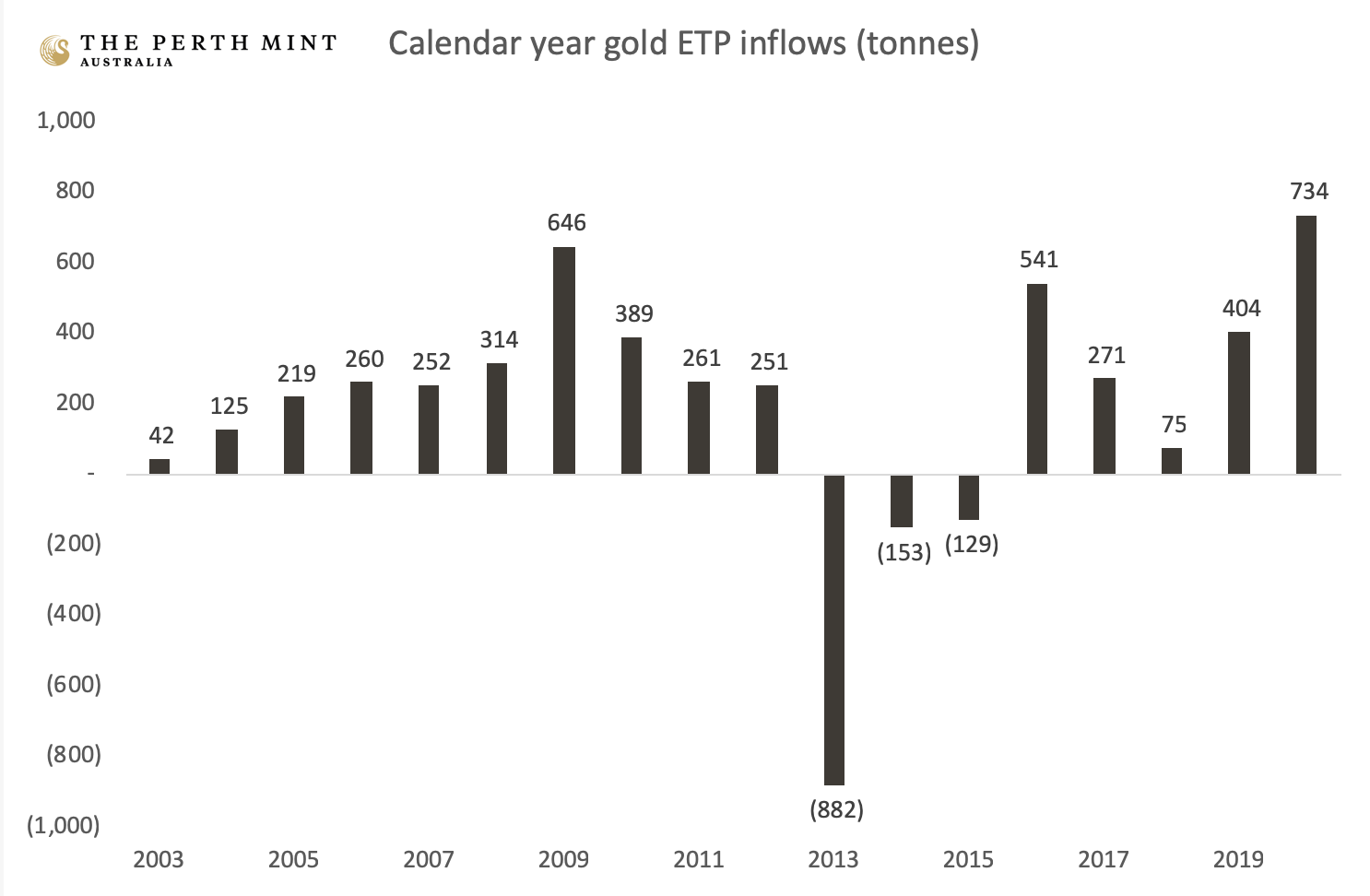

The charts below contextualise how significant the activity in the gold ETP market has been since the start of the year. The first chart highlights net inflows on a calendar year basis going all the way back to 2003.

Source: The Perth Mint, World Gold Council

Even though the year is only half complete, net inflows of more than 700 tonnes into gold ETPs are already higher than the full calendar year inflows seen in any of the past 16 years.

To further contextualise these purchases, at more than 700 tonnes, net inflows into gold ETPs this year are more substantial than the 50-year record high levels of central bank gold buying seen in 2018 and 2019. Nation states added 656 tonnes in 2018 and 650 tonnes in 2019 to their national reserves.

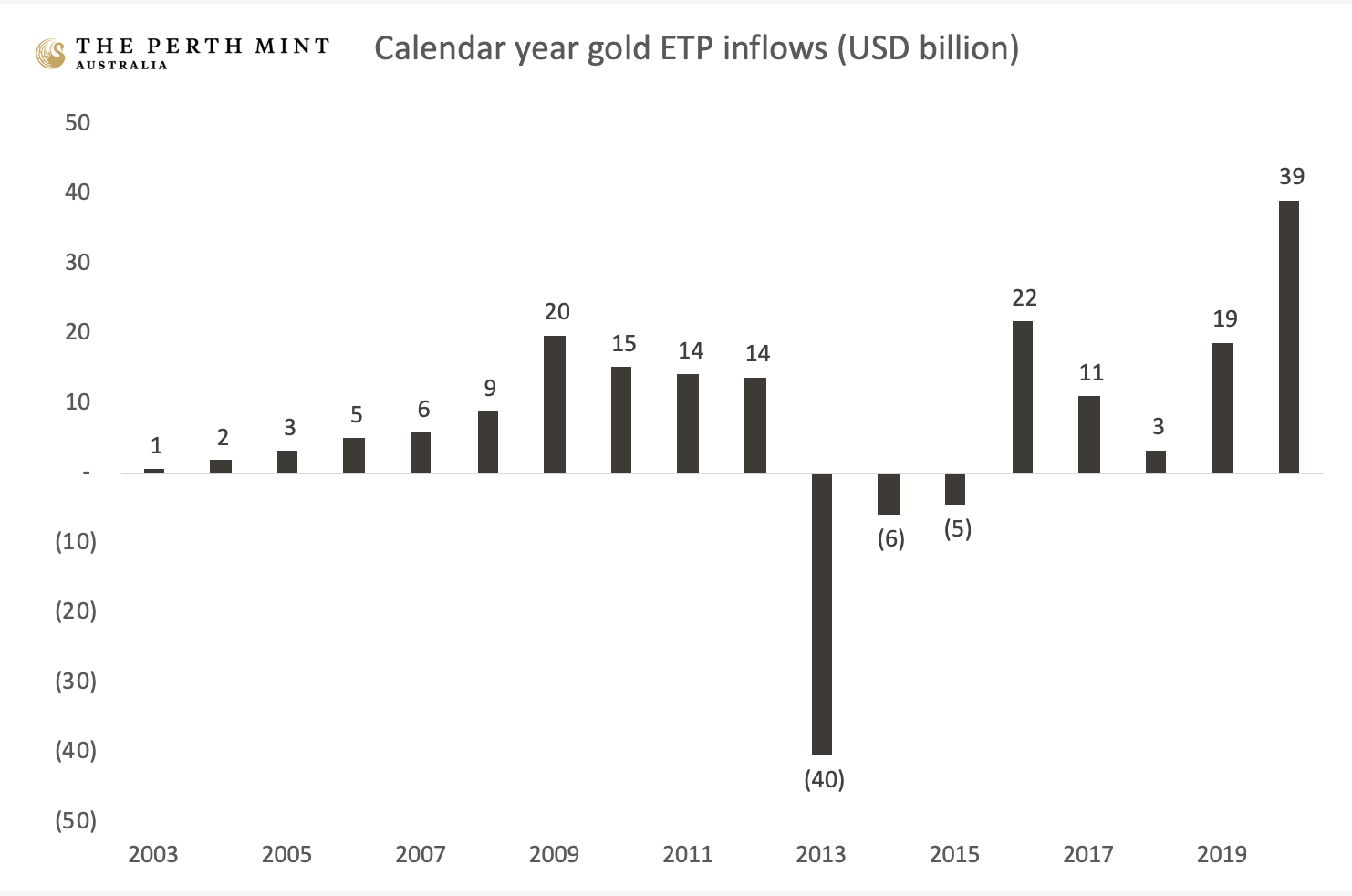

Impressive as the 2020 inflows are when looked at in pure tonnage terms, the chart below is arguably an even better illustration of the scale of the investment into these products today. It looks at calendar year inflows into gold ETPs as measured in billions of US dollars.

Source: The Perth Mint, World Gold Council

At just under USD 40 billion, inflows into gold ETPs in the first six months of 2020 have almost doubled the previous records set in the full 2009 and 2016 calendar years.

Whether it be due to the threat from COVID-19, uncertainty regarding the consequences of the monetary and fiscal stimulus being deployed, the lack of real return available in traditional safe havens, or a combination of these factors, there can be no doubting the investor appetite for gold bullion today.

Looking forward, the question is whether or not these inflows, and the strong price action seen in gold in 2020 are a warning sign for the bulls, or if they are merely the beginning of a multi-year trend that may see gold prices, and gold demand, continue to head higher.

To answer this, it’s important to analyse two key factors

-

How important gold ETPs are to the gold market.

- How large gold ETPs are in the context of broader portfolios.

How important are gold ETPs to the gold market?

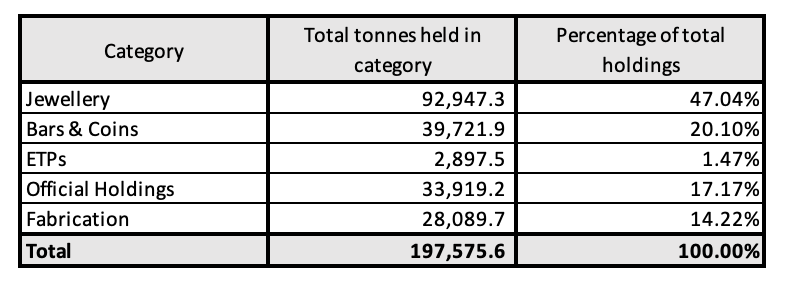

The best estimates suggest that by the end of 2019 more than 197,000 tonnes of gold had been mined across the course of human history. This gold is owned in a variety of forms which can be grouped into several major categories, including:

- Jewellery

- Physical bars and coins

- ETP holdings

- Official holdings (central bank reserves)

- Fabrication (industrial demand)

These are highlighted in the table below which indicate the tonnage and percentage of gold held in each category, with gold ETPs accounting for slightly less than 1.50% of total gold holdings at the end of 2019.

Source: The Perth Mint, World Gold Council

From a liquidity perspective, turnover in the gold market averaged more than USD 145 billion per day in 2019. Of this turnover, 54% was gold traded over-the-counter, whilst almost 45% was gold traded on the major futures exchanges, most notably COMEX. Barely 1% of the daily turnover in the gold market is directly attributable to gold ETPs.

As is stands today, gold ETPs make up only a small fraction of the total gold market, comprising less than 2% of the total market value of all gold holdings, and the daily liquidity in the gold market.

Less one interprets these statistics as a signal that gold ETPs remain relatively unimportant to the overall gold market, it’s worth remembering that humanity has been building its stockpile of gold for more than 6,000 years.

The first gold ETPs, including Perth Mint Gold, were only launched back in 2003.

It’s also worth pointing out that as per the above table, we humans like to wear and display our wealth, with almost half of total gold ownership expressed in jewellery form. Investment products that offer gold price exposure will never fully displace that.

Given these facts, it makes perfect sense that gold ETPs today remain a small portion of the total gold stockpile owned by investors, households and central banks worldwide.

Despite this, there is no doubt gold ETPs have had a profound impact on the gold market since they were first listed in the early 2000s.

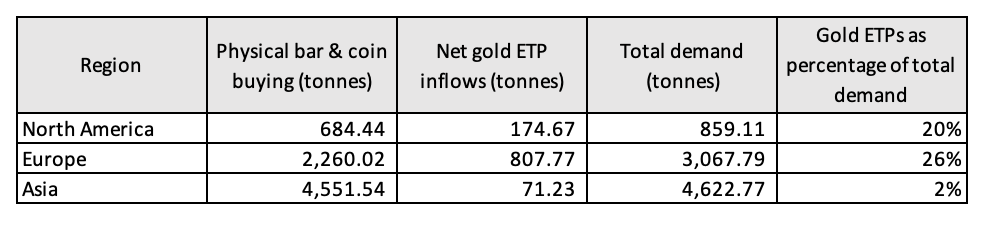

To illustrate this, consider the table below, which highlights private sector non-jewellery gold demand in North America, Europe and Asia between 2010 and 2019. Note that in the table;

- Physical bar and coin demand is calculated by summing up total buying per region in each calendar year.

- Net gold ETP inflows are calculated by subtracting total gold ETP holdings in each region at the end of 2009 from total gold ETP holdings at the end of 2019.

- Total demand is the sum of the physical bar and coin buying plus the net inflows into gold ETPs.

Source: The Perth Mint, World Gold Council

The table makes clear that over the last 10 years, when measured this way, gold ETPs have represented between 20-26% of total private sector non jewellery gold demand seen in North America and Europe.

Note these figures do not account for the record inflows seen in 2020, which will have only increased the market share of gold ETPs.

As a non-gold comparison point to help visualise that impact, consider that e-commerce sales in the United States grew from 6.4% of total US retail spending in 2010 to 16% at the end of 2019. By the end of 2018 estimates suggest Amazon had captured some 35% of the e-commerce market and roughly 6% of the addressable US retail market.

Look at it in this context and one could make case that gold ETPs have done as much if not more to disrupt the gold market than Jeff Bezos has done to disrupt the way Americans shop.

We have little doubt that the profound impact gold ETPs have had on the gold market in the last 15 plus years will continue to grow in the decade to come.

Gold ETPs in the context of the total ETP market

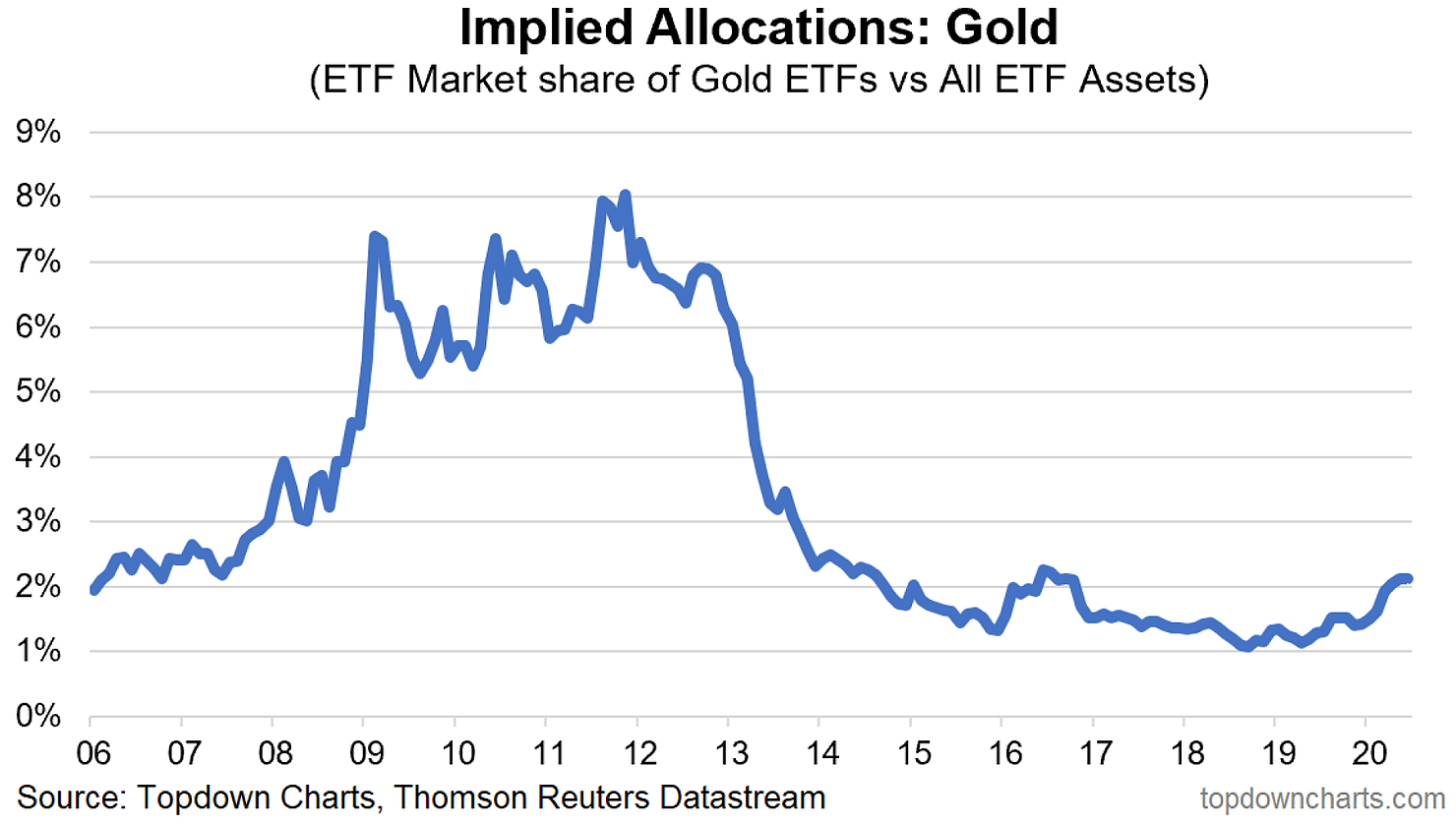

Gold ETPs currently make up just 2% of the total US ETP market, with this number barely one quarter of the market share they enjoyed just over 8 years ago.

This can be seen in the graph below from TopDown Charts (noting the chart uses the term ETF not ETP) which shows the evolution of US gold ETPs as a percentage of the total US ETP market since 2006.

In Australia, gold ETP holdings topped AUD 2.5 billion by the end of June 2020. From the end of 2015 through to end June 2020, the market value of Australian gold ETPs has increased by over AUD 2 billion, with their share of the local ETP market almost doubling, rising from 2.26% to almost 4% over this time period.

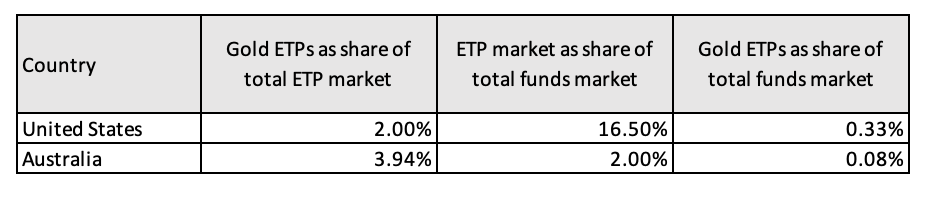

It is also worth highlighting the fact that the ETP market is just one component of the broader fund management universe. Estimates suggest that in 2019, ETPs made up just 16.5% of the total pool of regulated open-end investment funds in the United States, whilst in Australia the number was just 2%.

The table below therefore estimates total portfolio allocations to gold based on gold ETPs as a share of the total ETP market, and the ETP market as a share of the total investment funds market.

Source: The Perth Mint, ETFGI ICI 2019 annual factbook

Whilst the above table is a rough estimate, and doesn’t take into consideration gold held outside of ETPs, nor financial assets held outside of regulated investment funds, it does help to demonstrate the fact that investor allocations to gold remain incredibly modest, despite the all-time highs in gold ETP holdings and record inflows seen in 2020.

Going forward, there are of course no guarantees that total holdings in gold ETPs, nor allocations to gold at a portfolio level will rise.

Nevertheless, given the current low levels of exposure investors have, it’s fair to say that gold has much greater potential to benefit from a migration of investment capital into it, relative to the potential for it to suffer from a migration of investment capital away from it.

For an asset that is truly limited in supply, this has obvious implications for its potential price trajectory.

Jordan Eliseo

Manager – Listed Products and Investment Research

The Perth Mint

14 July 2020

Disclaimer:

Past performance does not guarantee future results.

The information in this article and the links provided are for general information only and should not be taken as constituting professional advice from The Perth Mint. The Perth Mint is not a financial adviser. You should consider seeking independent financial advice to check how the information in this article relates to your unique circumstances. All data, including prices, quotes, valuations and statistics included have been obtained from sources The Perth Mint deems to be reliable, but we do not guarantee their accuracy or completeness. The Perth Mint is not liable for any loss caused, whether due to negligence or otherwise, arising from the use of, or reliance on, the information provided directly or indirectly, by use of this article.

Get investment insights from industry leaders

Liked this wire? Hit the follow button below to get notified every time I post a wire. Not a Livewire Member? Sign up for free today to get inside access to investment ideas and strategies from Australia’s leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Gold and precious metal bull since early 2000. Have spent +25yrs working in investment analytics, research & portfolio construction, with a primary focus on the role of precious metals in investor portfolios. Author of two books on investing in gold and the causes of the GFC. Lover of markets, competition & technology

.jpg)

2 topics

.jpg)

Gold and precious metal bull since early 2000. Have spent +25yrs working in investment analytics, research & portfolio construction, with a primary focus on the role of precious metals in investor portfolios. Author of two books on investing in...

Expertise

Gold and precious metal bull since early 2000. Have spent +25yrs working in investment analytics, research & portfolio construction, with a primary focus on the role of precious metals in investor portfolios. Author of two books on investing in...

Expertise

Comments

Comments

Sign In or Join Free to comment