Asset Allocation - a good time to rebalance

Jonathan Sheridan

FIIG Securities

As the end of the financial year approaches, it is a traditional time to take stock and see how one’s portfolio has performed.

Please take a few minutes to watch our recent video on how we think you should alter your asset allocation as you age, and then consider the information below and how your portfolio has performed over the last few months, in particular with regard to its volatility.

I would expect, both from anecdotal and statistical reports, most Australian investors have been on a wild ride over the last 4 months as the coronavirus pandemic has played havoc with portfolios.

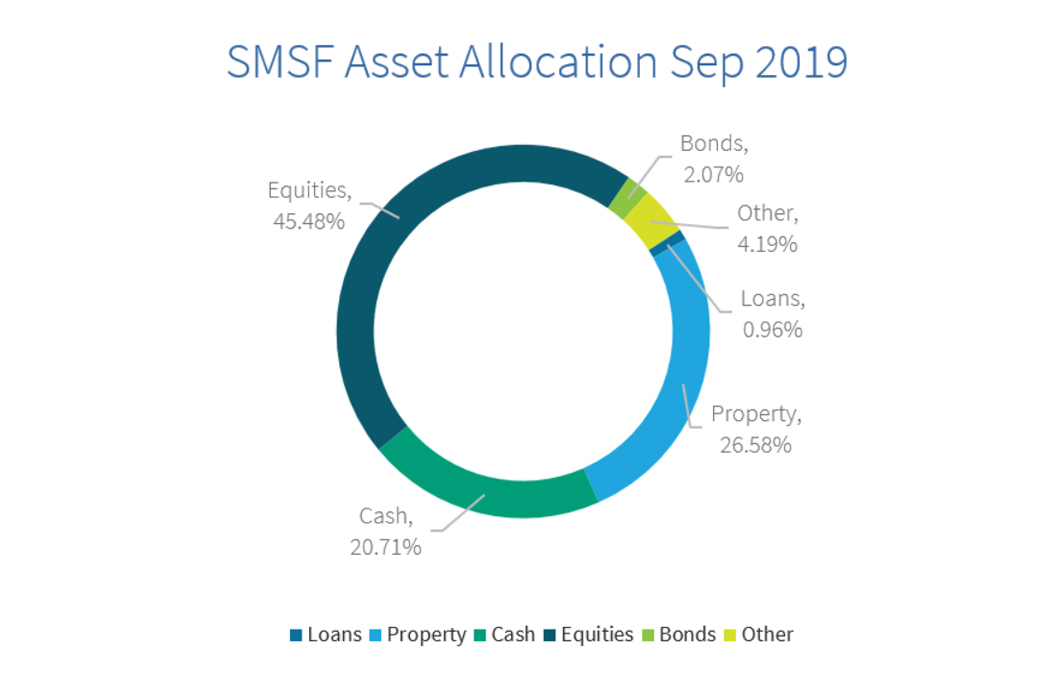

The ATO provides a quarterly update on the asset allocation of self-managed super funds (SMSF) (found here) which provides a useful look into how assets are currently split amongst self-directed superannuants.

The most current data is as at September 2019 and has been remarkably constant for a while.

It shows a huge overallocation to risky assets, being equities and property:

Managed funds, both listed and unlisted, account for 22.1% of all assets.

The key assumption here is that these managed funds are split in the same proportions as their direct holdings, i.e. Equities are 57.4% and Property is 33.5% of all managed funds. I have assumed that no cash is held in a managed fund, as cash allocations in these funds are presumably “dry powder” waiting to be applied to that particular asset class rather than a permanent allocation to cash.

The actual allocation to directly owned bonds is just 1.5% of all assets. See the end of the article for how we compare globally – it is still poor…

This risky allocation has worked relatively well for Australian investors given the hitherto uninterrupted economic expansion we have experienced for the last 29 years before the coronavirus pandemic ruined everyone’s party globally.

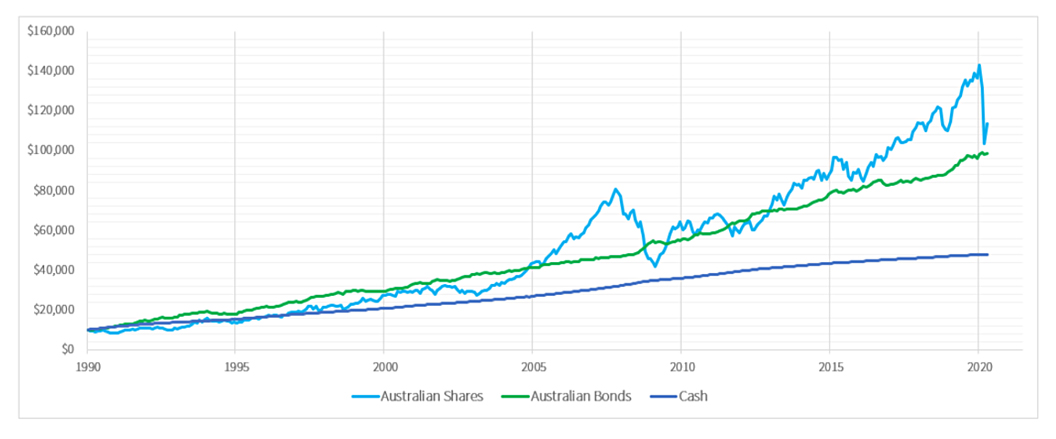

In the Vanguard returns chart below, Australian shares are now back close to the long term bond index level:

Source: (VIEW LINK)

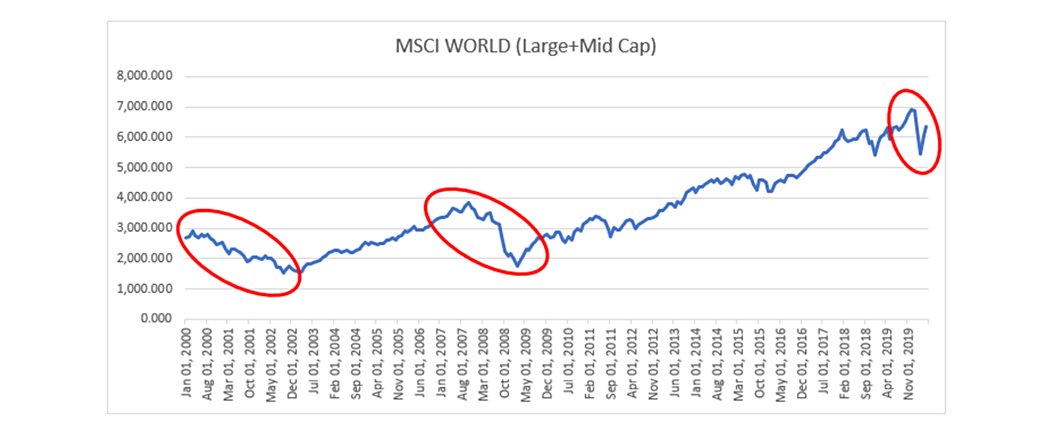

For the rest of the world this is just another recession to deal with, to go along with the early 2000s tech wreck, the GFC in 2008/9 and now this one in 2020. 3 recessions in 20 years seems a lot to me…

As you can see from the below chart, in each case global equities declined by approximately 50% from peak to trough and lasted approximately 2 years.

Source: (VIEW LINK)

I expect the economic damage from this pandemic to persist longer than is currently priced in, and so there is potential for risk asset prices to fall further from here given the speed of the recovery being based on hope not reality.

Based on history, which as we know does not repeat but it sure does rhyme, we can likely expect another 18 months or so of economic pain before we really start to see a proper recovery.

Conclusion - take the opportunity when it exists

Like in previous recessions, there has been a classic ‘bear market bounce’. This offers investors another opportunity, very recently since the last all-time highs in stocks, to exit these riskier positions and move their asset allocations to a less risky position for the next few years and avoid the pain of potential future drawdowns in risky asset prices.

Clearly there has been unprecedented central bank intervention and fiscal stimulus but remember that all of this support is just to plug the short-term gap – it is not necessarily a total net stimulus. The world economy was slowing long before coronavirus became the straw that broke that particular camel’s back.

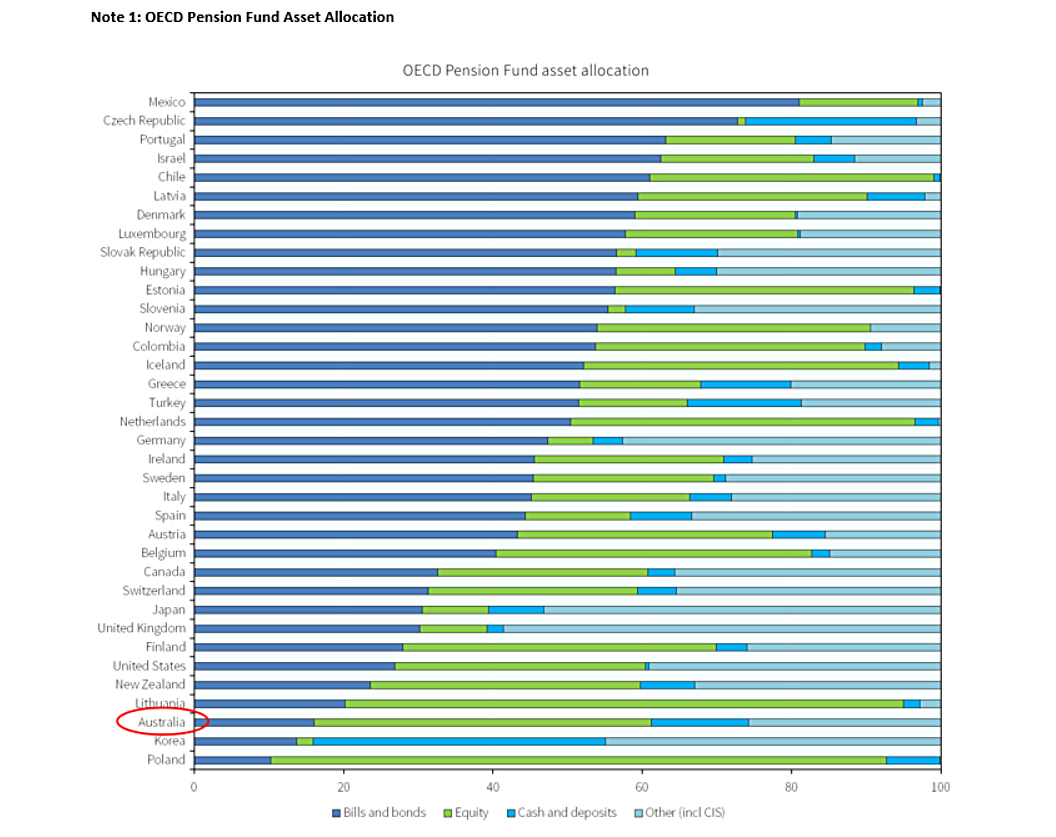

It therefore follows that now is a good time to reassess asset allocations of SMSFs in particular and bring them more into line with global best practice.

For example the UK pension fund average allocation to bonds is 30.2% and in the US it is 26.9%. The respective allocation to equities is 9.0% and 33.5%, and to cash just 2.2% and 0.5% respectively (see note 1 at the end of the article for the data).

There has been a timely reminder of what can happen to funds over exposed to risk assets, and yet there is also an opportunity to correct that misallocation without suffering a heavy loss.

This is likely to set up investors better for the probable drawdown to come and also to provide the security of capital and predictability of income from bonds versus equities (note that dividends, particularly bank dividends, have been cut significantly, in some cases to zero as with ANZ and WBC).

Source: http://www.oecd.org/daf/fin/private-pensions/globalpensionstatistics.htm

Please note that the OECD database gathers information on investments in Collective Investment Schemes (CIS) and the look-through of these investments in equities, bills and bonds, cash and deposits and other. Data on asset allocation in these figures include both direct investment in equities, bills and bonds, cash and deposits and indirect investment through CIS when the look-through of CIS investments is available. Otherwise, investments by pension funds in CIS are shown in a separate category.

Get investment insights from industry leaders

Liked this wire? Hit the follow button below to get notified every time I post a wire. Not a Livewire Member? Sign up for free today to get inside access to investment ideas and strategies from Australia’s leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Jon is FIIG Securities’ Chief Investment Strategist. Also a Chartered Accountant, Jon has been working in multi-asset class investment markets for over 15 years, and now specialises in providing fixed income solutions for FIIG’s clients.

........

This document has been prepared by FIIG Investment Strategy Group. Opinions expressed may differ from those of FIIG Credit Research.

The contents of this document are copyright. Other than under the Copyright Act 1968 (Cth), no part of it may be reproduced, distributed or provided to a third party without FIIG’s prior written permission other than to the recipient’s accountants, tax advisors and lawyers for the purpose of the recipient obtaining advice prior to making any investment decision. FIIG asserts all of its intellectual property rights in relation to this document and reserves its rights to prosecute for breaches of those rights.

FIIG Securities Limited (‘FIIG’) provides general financial product advice only. As a result, this document, and any information or advice, has been provided by FIIG without taking account of your objectives, financial situation and needs. FIIG’s AFS Licence does not authorise it to give personal advice. Because of this, you should, before acting on any advice from FIIG, consider the appropriateness of the advice, having regard to your objectives, financial situation and needs. If this document, or any advice, relates to the acquisition, or possible acquisition, of a particular financial product, you should obtain a product disclosure statement relating to the product and consider the statement before making any decision about whether to acquire the product. Neither FIIG, nor any of its directors, authorised representatives, employees, or agents, makes any representation or warranty as to the reliability, accuracy, or completeness, of this document or any advice. Nor do they accept any liability or responsibility arising in any way (including negligence) for errors in, or omissions from, this document or advice. FIIG, its staff and related parties earn fees and revenue from dealing in the securities as principal or otherwise and may have an interest in any securities mentioned in this document. Any reference to credit ratings of companies, entities or financial products must only be relied upon by a ‘wholesale client’ as that term is defined in section 761G of the Corporations Act 2001 (Cth). FIIG strongly recommends that you seek independent accounting, financial, taxation, and legal advice, tailored to your specific objectives, financial situation or needs, prior to making any investment decision. FIIG does not provide tax advice and is not a registered tax agent or tax (financial) advisor, nor are any of FIIG’s staff or authorised representatives. FIIG does not make a market in the securities or products that may be referred to in this document. A copy of FIIG’s current Financial Services Guide is available at www.fiig.com.au/fsg.

An investment in notes or corporate bonds should not be compared to a bank deposit. Notes and corporate bonds have a greater risk of loss of some or all of an investor’s capital when compared to bank deposits. Past performance of any product described on any communication from FIIG is not a reliable indication of future performance. Forecasts contained in this document are predictive in character and based on assumptions such as a 2.5% p.a. assumed rate of inflation, foreign exchange rates or forward interest rate curves generally available at the time and no reliance should be placed on the accuracy of any forecast information. The actual results may differ substantially from the forecasts and are subject to change without further notice. FIIG is not licensed to provide foreign exchange hedging or deal in foreign exchange contracts services. FIIG may quote to you an estimated yield when you purchase a bond. This yield may be calculated by FIIG on either A) a yield to maturity date basis; or B) a yield to early redemption date basis. Some bond issuances include multiple early redemption dates and prices, therefore the realised yield earned by you on the bond may differ from the yield estimated or quoted by FIIG at the time of your purchase. The information in this document is strictly confidential. If you are not the intended recipient of the information contained in this document, you may not disclose or use the information in any way. No liability is accepted for any unauthorised use of the information contained in this document. FIIG is the owner of the copyright material in this document unless otherwise specified.

4 topics

Jonathan Sheridan

Director, Fixed Income & Investment Strategy

FIIG Securities

Jon is FIIG Securities’ Chief Investment Strategist. Also a Chartered Accountant, Jon has been working in multi-asset class investment markets for over 15 years, and now specialises in providing fixed income solutions for FIIG’s clients.

Jonathan Sheridan

Director, Fixed Income & Investment Strategy

FIIG Securities

Jon is FIIG Securities’ Chief Investment Strategist. Also a Chartered Accountant, Jon has been working in multi-asset class investment markets for over 15 years, and now specialises in providing fixed income solutions for FIIG’s clients.

Comments

Comments

Sign In or Join Free to comment