ASX 200 to rise, S&P 500 bounces + Fortescue at a two-month high

Get up to date on overnight market activity and the big events for the day.

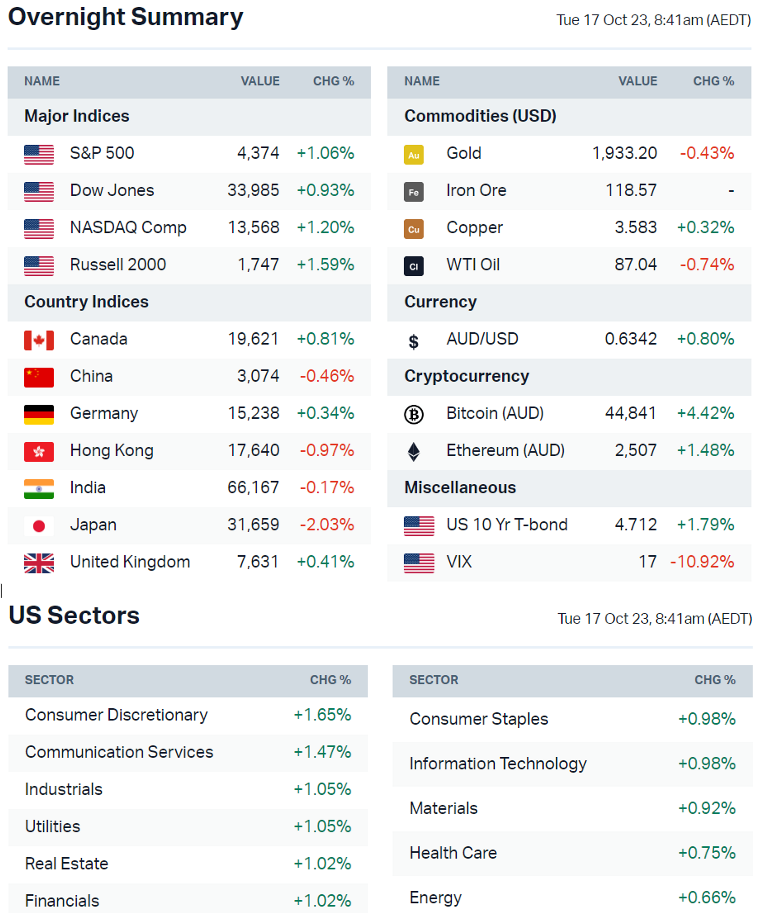

ASX 200 futures are trading 48 points higher, up 0.68% as of 8:30 am AEST.

S&P 500 SESSION CHART

MARKETS

- Major US benchmarks finished higher and near best levels

- At ~440, the S&P 500 marked its strongest breadth day since late March

- Consumer and defensive sectors were some of the strongest areas

- Apple was the main laggard amid reports of weaker China iPhone demand

- Yields are bouncing, with the 10-year back above 4.7% from 4.5% last week

- Gold pulled back after rallying more than 5% last week

- No real change in market narrative despite some renewed upward pressure on yields

- Bullish focus points include the recent dovish shift in Fedspeak, positive start to Q3 earnings season, expectations of more earnings growth in Q4, fund flows and seasonality tailwinds

- Markets brace for potential broader regional conflict that may deal fresh blow to global economy (Bloomberg)

- Money managers increasingly underweight or shorting bonds (Bloomberg)

STOCKS

- Apple iPhone 15 sales down 4.5% compared with the iPhone 14 over the first 17 days after released (Bloomberg)

- LinkedIn to lay off more than 660 across multiple teams (Axios)

- Ford Chairman warns UAW strikes threaten the livelihood of company (CNBC)

- BlackRock says SEC still reviewing Bitcoin ETF, after approval rumours (Bloomberg)

- Lululemon shares surge amid S&P 500 Index inclusion (CNBC)

- Pfizer cuts full-year guidance on weakening demand for Covid products (WSJ)

- Snap rallies as internal CEO memo offered 2024 goals including 20% full-year revenue growth and $500 million in non-ad revenue (CNBC)

EARNINGS

Off to a good start: Blended Q3 earnings growth for the S&P 500 stands at +0.4%, on track to mark the first year-on-year in earnings growth in a year. According to FactSet, 84% of results have so far surpassed consensus expectations, ahead of the 74% one-year average. In aggregate, results have topped earnings estimates by 10.1%.

Charles Schwab (+4.7%): Mixed report; deposit balances beat estimates at US$284.4bn vs. US$268.8bn expected, earnings beat but revenue missed, net revenue down 24% due to cash shuffling as customers moved funds to money markets from cash.

GEOPOLITICS

- Biden mulls visit to Israel in coming days (Bloomberg)

- Gaza border crossing set to reopen as Israeli troops prepare ground assault (Reuters)

- US puts 2,000 troops on alert to deploy to Israel for medical and advisory purposes, no infantry included (AP)

CHINA

- PBOC offers most cash support since 2020 as debt sales surge (Bloomberg)

- China stock regulator announces restrictions on securities lending (Reuters)

- IMF warning on China puts risk of "Japanization" in spotlight (Reuters)

- China local governments are finding it no longer cheap to borrow, the latest signs of rising stress (Bloomberg)

ECONOMY

- New York Fed's Empire State factory gauge weaker than expected in October, slips back into contraction (MarketWatch)

Peak Fed, Upside for Stocks (if things don't break)

Market rebounds this year have been driven by the fact that major economic concerns such as a hard landing, Chinese economic collapse, geopolitical tensions or systemic failures, have not materialised.

One of the bullish themes this year has been the dovish tilt in Fedspeak. Multiple policymakers flagged that the tightening of financial conditions as the reason why they're patient.

The data for peak Fed points to some solid gains ahead, provided things don't break.

Never miss an update

Get the latest insights from me in your inbox when they’re published.

Advertisement

- The end of the tightening cycle has returned has returned 6.6% over the first three months and 8.7% over six months for the S&P 500, according to JPMorgan

- US markets typically rally following peak hawkishness, subject to the economy avoiding a recession, according to Goldman Sachs

- Following the peak in 2-year bond yields, the S&P 500 has rallied 8% in the following three months and 23% in subsequent 12 months, says Goldman Sachs

- However, stocks tend to sell off if a recession happens in the subsequent 12 months

Sectors to Watch

Iron Ore: Despite all the headlines about China's property market and the rising US dollar, Fortescue (ASX: FMG) is quietly breaking out to a two-month high. China dished out added US$39.6bn into the financial system this week, the largest monthly injection since December 2020.

Gold: Gold experienced a sharp spike last Friday amid rising geopolitical tensions and short covering. It struggled to push over the below channel and eased overnight.

Coal: Teck came out with a surprise production miss overnight, with third quarter steelmaking coal sales of 5.2 million tonnes, below the 5.6 million to 6.0 million expected due to "slower than anticipated supply chain recovery ... and the labour disruption at BC ports and plant challenges." The average realised steelmaking coal price in Q3 was US$229 a tonne. We also have Stanmore (ASX: SMR ) reporting its quarterly today.

Growth is Lagging, Breadth is Poor

A bit of a small chart but all you need to pay attention to are the trendlines. The below chart depicts:

- Top left: SPDR S&P 400 Midcap Growth ETF

- Top right: ARKK Innovation ETF

- Bottom left: S&P 500 Equal Weight ETF

- Bottom right: Nasdaq 100 Equal Weighted Index

The below charts aren't really supportive of a bull case or a broad-based rally. Are stocks struggling because they're trying to price in a recession or are they repricing purely due to higher rates?

Source: TradingView

KEY EVENTS

ASX corporate actions occurring today:

- Trading ex-div: Horizon Oil (HZN) – $0.02, WAM Capital (WAM) – $0.077, WAM Leaders (WLE) – $0.045

- Dividends paid: Ambertech (AMO) – $0.01, SKS Technologies (SKS) – $0.002, Qube Holdings (QUB) – $0.04, Bluescope Steel (BSL) – $0.25, Garda Property (GDF) – $0.01

- Listing: None

Economic calendar (AEDT):

- 11:30 am: RBA Meeting minutes

- 5:00 pm: UK Unemployment

- 8:00 pm: Germany ZEW Economic Sentiment Index

- 11:30 pm: Canada Inflation Rate

- 11:30 pm: US Retail Sales

This Morning Wrap was written by Kerry Sun.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Livewire and Market Index's pre-opening bell news and analysis wrap. Available weekday mornings and written by Kerry Sun.

........

Livewire gives readers access to information and educational content provided by financial services professionals and companies (“Livewire Contributors”). Livewire does not operate under an Australian financial services licence and relies on the exemption available under section 911A(2)(eb) of the Corporations Act 2001 (Cth) in respect of any advice given. Any advice on this site is general in nature and does not take into consideration your objectives, financial situation or needs. Before making a decision please consider these and any relevant Product Disclosure Statement. Livewire has commercial relationships with some Livewire Contributors.

2 stocks mentioned

1 contributor mentioned

Livewire and Market Index's pre-opening bell news and analysis wrap. Available weekday mornings and written by Kerry Sun.

Expertise

Livewire and Market Index's pre-opening bell news and analysis wrap. Available weekday mornings and written by Kerry Sun.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

The 4 biotech firms the experts are most excited about

Livewire Markets