ASX’s most highly rated lithium producer: Is Greenbushes enough for IGO?

ASX lithium stocks are about to enter their third year of general decline. Most of the major lithium names are down in order of magnitude 70-90% from the highs set in late 2022 – punching a substantial hole in many Aussie investors’ portfolios.

The rise and fall of this sector should serve as a reminder that not all narratives – no matter how sensible and promising – will translate into share price gains. Yes, every other car you see on the road now is an EV, but that doesn't mean every company trying to make a business out of the EV value chain is going to be sought after by investors.

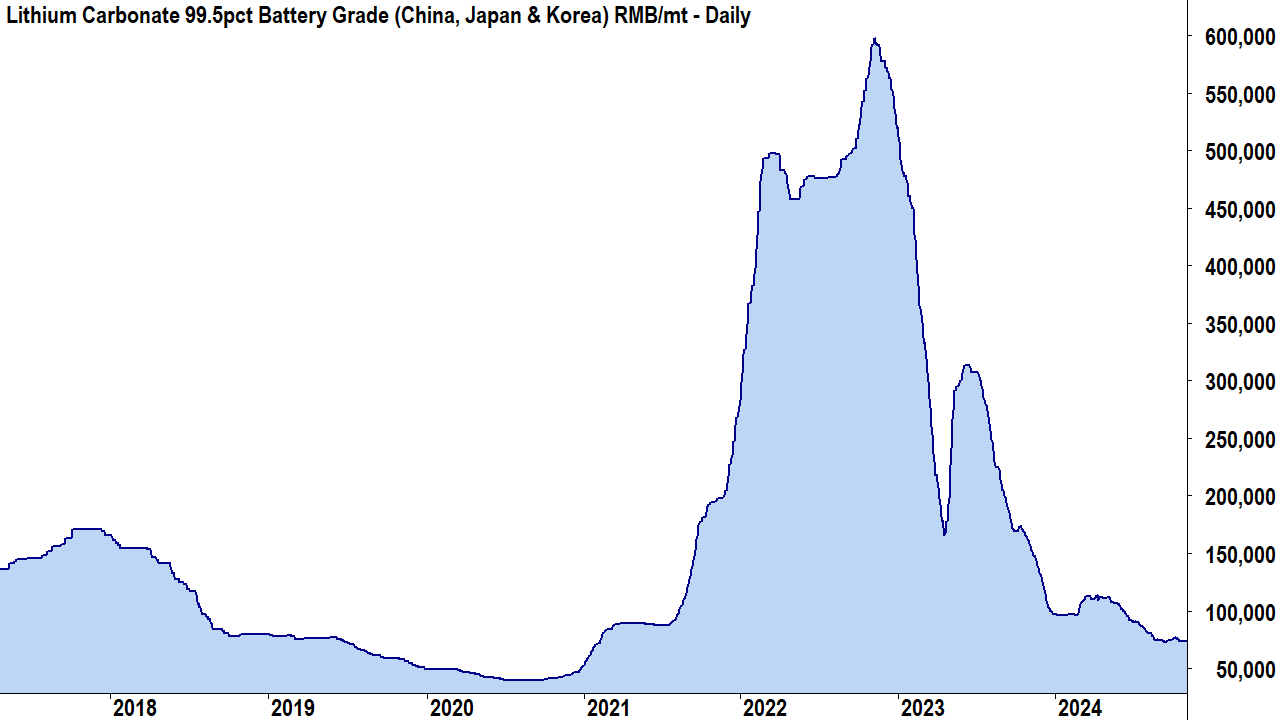

The commodity price cycle is real, it has been happening since tulips cost as much as a Dutch windmill in 1692, and it’s playing out in the lithium market as you read this sentence:

Stage 1: Scarcity of supply versus a sudden increase in demand (gosh that Tesla looks nice) creates an environment where prices can rise very quickly.

For lithium, this was the market in 2021 and 2022 – lithium minerals prices were booming. Ironically, the last lithium price cycle that peaked in late-2017 saw prices of lithium minerals crater in 2019 and 2020 – leading to a great deal of supply leaving the market around the beginning of 2021.

Stage 2: Investment in supply ramps up, and with a lag, eventually so too does supply

For lithium, this was 2021-2022 where it seemed every new IPO was a lithium hopeful and nearly every junior miner switched sides quicker than your 7-year-old barracking for this year’s premiership winner (they’ve all switched back to gold and silver now!).

Stage 3: Supply and demand move to equilibrium and prices flatten out.

In the case of lithium, the market moved quickly into oversupply as Chinese producers in particular ramped up production, but also several massive projects in Australia and South America can online around the same time. Most of these remain in ramp up phases, and so the market moved into a large surplus.

Stage 4: Prices plunge, supply is disincentivised, the cycle begins again!

Lithium minerals prices are cratering again, and yes, there has been talk for a couple of months now about supply (particularly marginal supply from Chinese lepidolite producers) leaving the market. It’s a cycle, right? So that means we must be close to the bottom again?

Perhaps. If this is the case, you’ll want to know which ASX lithium producers to buy for the next ride on the lithium price cycle. In this article, and in Part 2 tomorrow, I’ll investigate which lithium stocks are the most highly rated by the brokers. Let’s kick off with IGO, which has a major stake in the world’s largest and lowest cost hard-rock lithium mine, the Greenbushes mine in Western Australia. IGO reported its September quarter production and activities yesterday.

IGO September Quarter Results Highlights

- Spodumene concentrate (SC6) production was 406kt, +22% vs previous quarter, no change to FY25 guidance of 1,350 – 1,550kt

- Spodumene sales 392kt, -26% (no guidance provided)

- Cash costs $277/t, -18% vs previous quarter, no change to FY25 guidance $320 – $380/t

- Realised spodumene price of US$872/t FOB Australia

- Lithium hydroxide production 1502t, +13% (no guidance provided)

- Nickel production 3.6kt, -42% vs previous quarter, no change to FY25 guidance 16kt – 18kt

- Copper production 1.7kt, -43% vs previous quarter, no change to FY25 guidance 6.25kt – 7.25kt

- Nickel/Copper sales $101 million, -30% vs previous quarter (no guidance provided)

- Nickel cash costs $6.50/lb Ni, +1.21% vs previous quarter, no change to FY25 guidance $4.80/lb - $5.80/lb

- Group Underlying EBITDA -$3 million -104% vs previous quarter

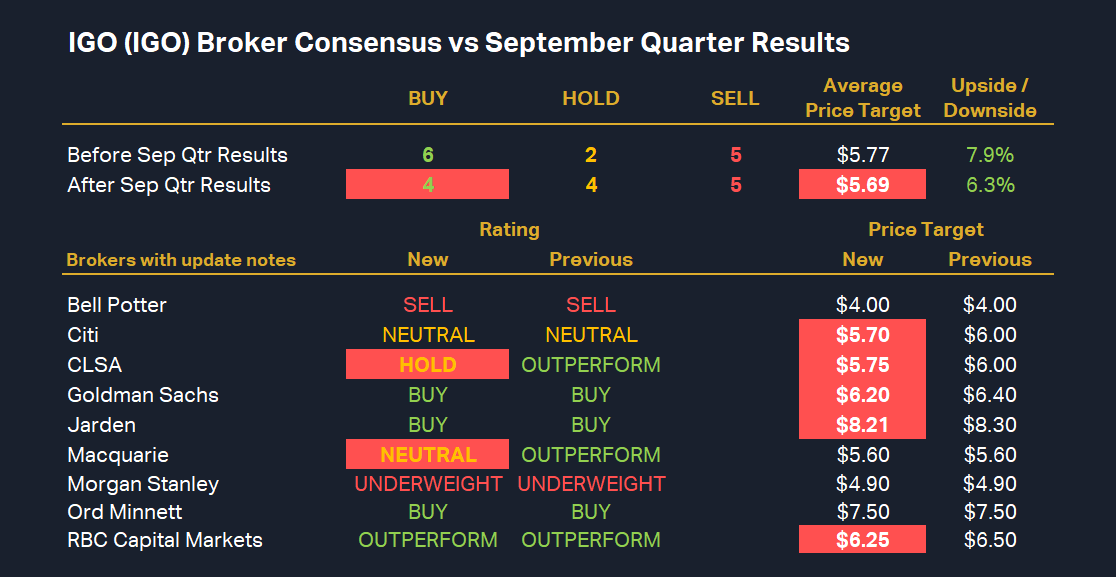

Individual broker views

Bell Potter: Retain SELL | Target price: $4.00

Broker notes that current IGO share price implies a much higher spodumene price than the spot price, (US$1,400/t vs US$750/t) suggesting that IGO is significantly overvalued on this metric. “The downside risk is that the longer weak lithium pricing persists, the more likely the market is to lose patience for a price recovery”. However, the broker notes the “quality” of Greenbushes which “will catalyse the share price once lithium prices begin to recover”.

Citi: Retain NEUTRAL | Target Price: $5.70⬇️ vs $6.00

Broker notes reduced disclosures from the company regarding the TLEA (Tianqi Lithium) joint venture. This created increased uncertainties around associated ongoing dividend payments, and therefore the broker’s own confidence in the stock. The broker is neutral on lithium in general, and this is reflected in its view on IGO.

CLSA: Downgrade to HOLD from OUTPERFORM | Target price: $5.75⬇️ vs $6.00

Broker notes the lack of TLEA dividend equates with a cautious approach as the focus for IGO shifts towards lithium minerals and away from nickel. Acknowledges quality of Greenbushes asset, but the company’s increasing reliance on lithium also creates risks and FY25 earnings visibility remains limited given current pricing environment.

Goldman Sachs: Retain BUY | Target price: $6.20⬇️ vs $6.40

Broker notes Greenbushes production was “well above” its forecast, costs were also better than expected, but realised pricing was below expectations. Nova Nickel was below expectations. IGO is still the most highly rated lithium stock in the broker’s coverage, trading at a significant discount and with a superior cashflow outlook than its peers.

Jarden: Retain BUY | Target price: $8.21⬇️ vs $8.30

Broker notes the solid performance at Greenbushes despite a challenging pricing environment. Delayed TLEA dividend represents a cautious approach in the face of rising capital expenditures. Nickel business performance was significantly disappointing, but the key to IGO is a recovery in lithium pricing which is critical to future dividends.

Macquarie: Downgrade to NEUTRAL from OUTPERFORM | Target price: $5.60

Broker notes a “pleasing” result at Greenbushes, but the cash draw from other parts of the business “detracted from the result”. “Without clear catalysts on the horizon, we see the stock moving in line with the underlying commodity”, the broker notes, as it downgrades its rating to NEUTRAL “on valuation grounds”. This reverts the brokers upgrade to OUTPERFORM as recently as 30 August.

Morgan Stanley: Retain UNDERWEIGHT | Target price: $4.90

Broker notes strong performance at Greenbushes, but underperformance at Nova (by as much as 20% versus forecasts).

Ord Minnett: Retain BUY | Target price: $7.50

Broker notes overall result “met market expectations”, although Nova is showing “variable” performance. Suggests reduced disclosures by company is to “simplify the business and cut costs”. Greenbushes continues to generate positive margins and IGO is trading at a 20% discount to its NPV. Most of IGO’s valuation upside is expected to materialise “beyond 2025”.

RBC Capital Markets: Retain BUY | Target price: $6.25⬇️ vs $6.50

Broker sees Nova performance a drag on an otherwise strong performance by the company driven by Greenbushes. TLEA dividend delay put down to conservatism amid lithium price volatility. Operational inconsistencies trigger a cut in EBITDA forecast, hence the reduction in the target price.

IGO broker consensus: Buy, Hold, or Sell?

%20Broker%20Consensus%20vs%20September%20Quarter%20Results.png)

The above table shows all ratings and targets for IGO from broker research notes since May 1 (to keep it current). To obtain IGO’s Broker Consensus Rating, we assigned a value of +1 to any rating better than HOLD/NEUTRAL/MARKETWEIGHT, a value of 0 for any rating equivalent to HOLD/NEUTRAL/MARKETWEIGHT, and a value of -1 to any rating worse than HOLD/NEUTRAL/MARKETWEIGHT.

We then take the average of all assigned – rating values and assign a Broker Consensus Rating of BUY to average rating values greater than +0.5, a rating of HOLD for average rating values between -0.5 and +0.5, and a rating of SELL for average rating values less than -0.5.

Using this model, IGO’s average rating value is -0.08 – down from +0.08 prior to its September update but resulting in the stock’s Broker Consensus Rating remaining at HOLD.

IGO’s consensus (average) target price is $5.69, down 1.5% from $5.77 prior to its September update. This suggests brokers collectively believe the stock is around 6.3% undervalued based upon the closing price on Monday 28 October of $5.35.

It’s worth noting that the consensus price target may change over the next few days as the brokers we have on file who have not yet updated their analysis on IGO post-update may do so. Given there have been modest cuts to most brokers' target prices so far, there is a very good chance IGO’s consensus target will decline, therefore reducing its Upside potential.

Stay tuned for Part 2…

In Part 2, we’ll investigate the big brokers’ views, ratings, and price targets on IGO’s ASX lithium peers including Pilbara Minerals (ASX: PLS), Mineral Resources (ASX: MIN), Liontown Resources (ASX: LTR), Arcadium Lithium (ASX: LTM), Core Lithium (ASX: CXO), Piedmont Lithium (ASX: PLL), Sayona Mining (ASX: SYA), Ioneer (ASX: INR), Vulcan Energy Resources (ASX: VUL), Galan Lithium (ASX: GLN), and Global Lithium Resources (ASX: GL1).

This article first appeared on Market Index on Tuesday 29 October 2024.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl has a passion for technical analysis and has taught his unique brand of price-action trend following to thousands of Aussie investors.

........

Investing is risky. Inevitably you will endure losses. If you can't cope with losing, don't invest.

{kind=link}

%20Broker%20Consensus%20vs%20September%20Quarter%20Results.png){kind=link}

5 topics

12 stocks mentioned

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl...

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl...

Comments

Comments

Sign In or Join Free to comment