Australian house prices starting to fall - collapse likely averted but expect more weakness ahead

Back on 19th March when we first looked at the impact of the intensifying shutdown of the Australian economy on the housing market we concluded that the impact would depend on how high unemployment rose. Our base case was a recession that saw unemployment rise to around 7.5% and would push average home prices down around 5%, but the risk was that a deeper downturn with say 10% unemployment could see a 20% fall in prices. Subsequent government support measures along with an earlier reopening of the economy have reduced the risk of worse case scenarios for home prices.

So far so good

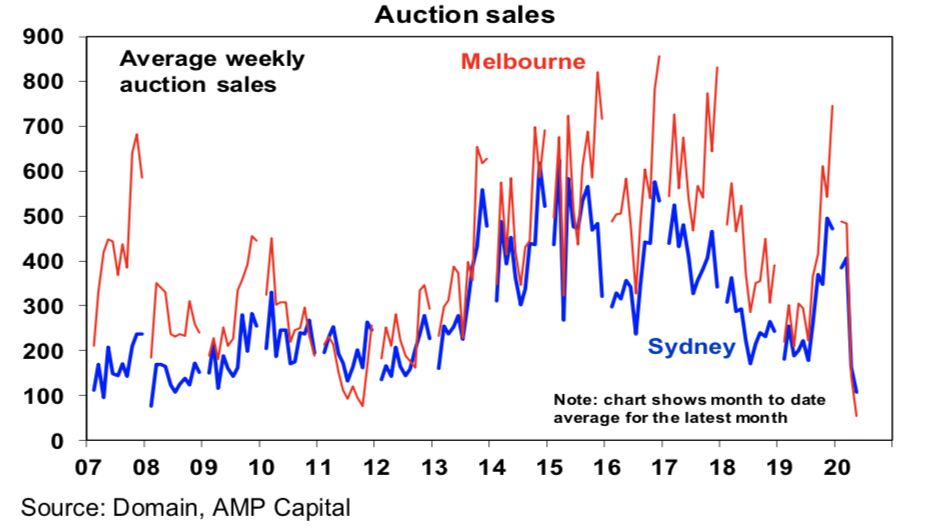

Since March property sales have slowed to a crawl.

The combination of the need for social distancing and the banning for a while of traditional on-site auctions led to a sharp decline in properties for sale. In addition to this, the Federal Government’s JobKeeper scheme keeping around 3.5 million people in paid employment and a doubling in unemployment benefits along with bank mortgage payment holidays, all of which are for the six months to September, have helped head off an increase in forced sales that might have occurred given the size of the hit to the economy. So, while property demand has fallen, it’s been matched by a collapse in supply, which has left the property market in a bit of a twilight zone.

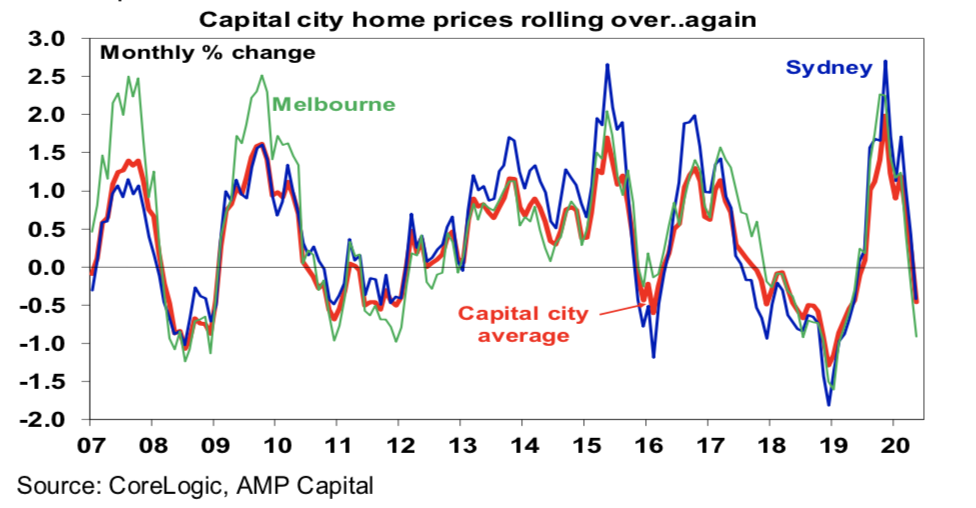

While listings have started to pick up a bit lately, they are still very low and this has all helped soften the blow to house prices that would have otherwise occurred, but prices are still starting to fall. According to CoreLogic, after slowing to just 0.2% growth in April, average capital city home prices fell -0.5% in May. Prices fell in all cities except Adelaide, Hobart and Canberra, with Melbourne -0.9%, Sydney -0.4% and Perth -0.6%. This has seen the monthly change in capital city home prices collapse from a peak of 2% in November.

So where to from here?

The positives for the property outlook

There are basically five “positives” for property prices.

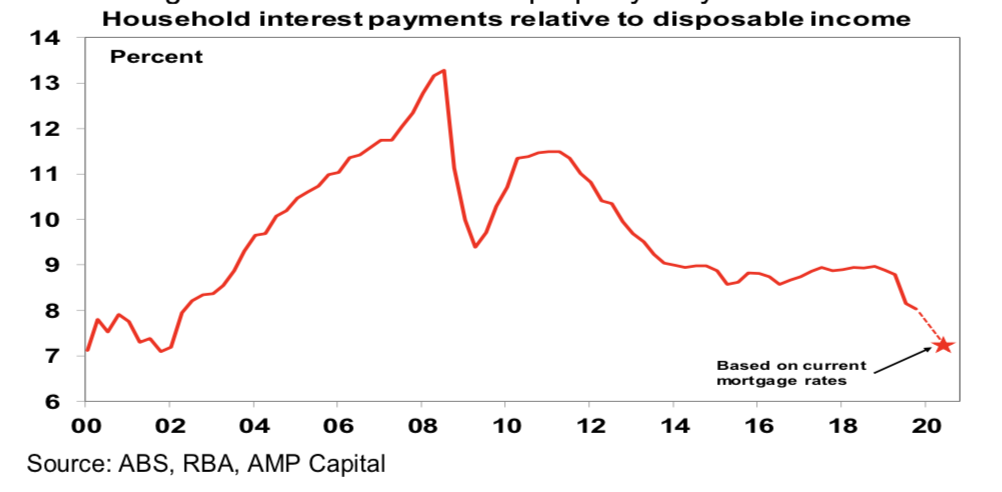

- Mortgage rates have fallen to record lows with deals around 2 to 3%. This is keeping mortgage debt interest costs as a share of household income well below historic highs even though the ratio of household debt to income is at a record high of around 200%. Low mortgage costs also make the funding costs for an investment property very low.

-

As noted above, while listings remain low.

-

Government support measures have provided a huge boost to household income, supported businesses, supported employment for around 3.5 million workers, prevented a confidence zapping surge in measured unemployment & with bank mortgage payment holidays (which has seen around 440,000 mortgage deferrals) are preventing a sharp rise in mortgage delinquencies and hence forced sales.

The shutdown, impacting mostly services jobs, has hit women and younger workers harder in contrast to past recessions which have hit male breadwinners harder and this may have helped keep down debt servicing problems.

China is running 2-3 months ahead of Australia with respect to the coronavirus shock and its experience provides some guide. While property sales were near zero in the peak lockdown month of February average property price growth slowed but did not go negative and is now picking up a bit.

The negatives

Against these positives there are these big “negatives” for property prices flowing from the coronavirus shock.

-

High unemployment. We have long regarded the combination of high house prices and high household debt as Australia’s Achilles heel and so we feared back in March that a large rise in unemployment could trigger debt servicing problems, forced sales and so sharp falls in prices. As it’s turned out, measured unemployment is being suppressed and household incomes supported by stimulus measures. This is by design to help businesses, jobs and incomes hold up through the shutdown period. It’s likely headed off the worst case 20% decline in house prices scenario we saw in March. But once the support measures end later this year, measured unemployment will likely rise to around 8% and take a long time to fall back to the pre coronavirus levels around 5.2%. This in turn is likely to lead to some increase in mortgage defaults as bank payment holidays (for around 440,000 mortgages) end, boosting forced sales and act as a drag on property demand, albeit it’s unlikely to be anywhere near what would have occurred in the absence of support measures through the shutdown.

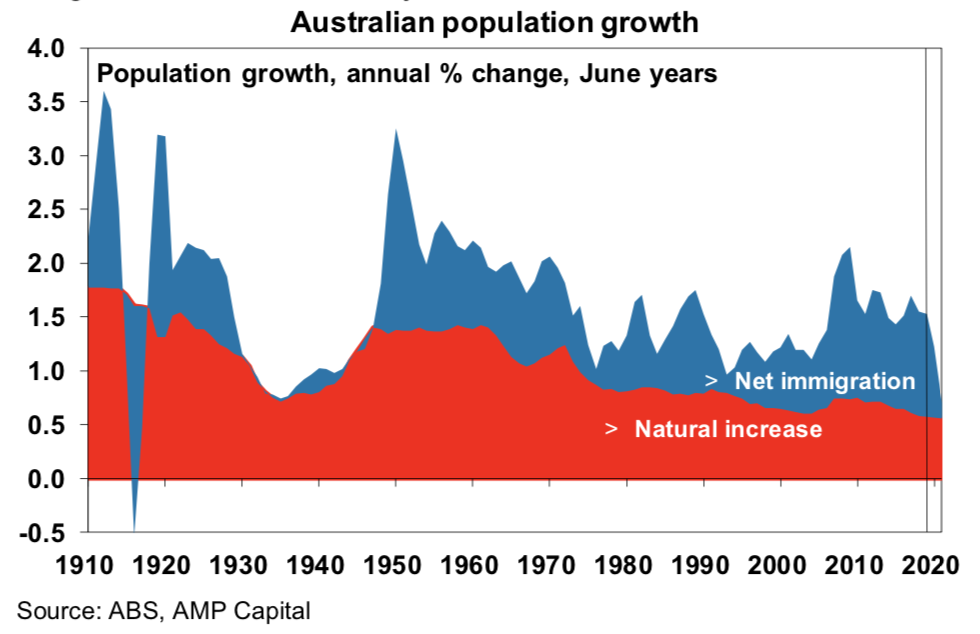

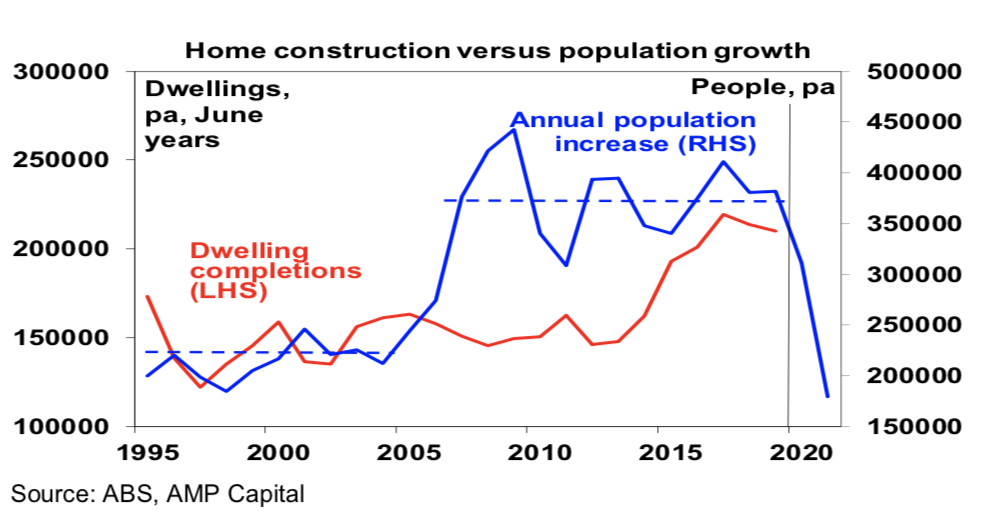

A big drop in immigration. Thanks to travel bans, the Government expects net immigration to fall to just below 170,000 this financial year and to around 35,000 next financial year from 240,000 last financial year. This is a huge hit and if it occurs – the Government could always allow a faster return of immigration – it will take population growth over 2020-21 to just 0.7%, its lowest since 1917.

It will imply a hit to underlying dwelling demand of around 80,000 dwellings over the next 12 months taking it down to around 120,000 compared to underlying demand last year of around 200,000. This risks resulting in a significant oversupply of dwellings, reversing years of undersupply that has maintained very high house prices since mid-last decade. A cut to immigration is not something China has had to deal with, so its property market experience is not directly translatable to Australia.

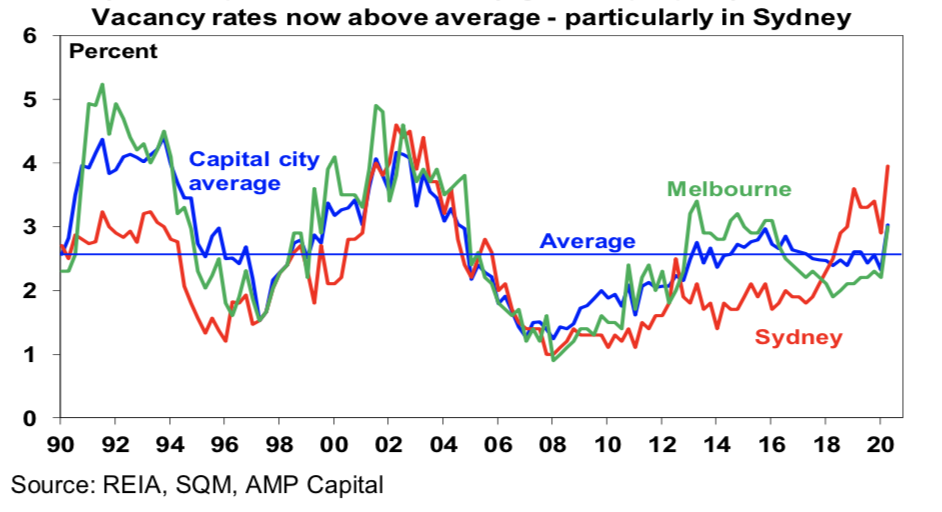

- Falling rents and rising vacancy rates. Vacancy rates rose sharply in April and this plus rent relief is putting downwards pressure on rents. This will be further impacted by very low immigration. It will further weigh on investor demand and may cause problems for heavily geared property investors.

- Measures to boost housing construction. Faced with a big reduction in housing construction activity over the year ahead, governments appear to be working on plans to boost activity to protect home builders’ jobs via new home building grants and possibly the construction of social housing. Normally first home buyer grants provide a boost in overall demand. But if the focus is just on boosting supply at a time when underlying demand is very low reflecting lower immigration it could add to downwards pressure on average prices. (Proposed moves from stamp duty to land tax in some states could provide a short-term boost to home prices but should be long term neutral if the same revenue is raised and it’s unclear whether or when it will occur.)

Our worst-case scenario for a 20% decline in prices and those of others seeing 30% plus falls are unlikely thanks to support measures and the earlier reopening of the economy. To get these worst-case scenarios would require a “second wave” of coronavirus cases & so a renewed shutdown or another down leg in the economy in response to a surge in bankruptcies.

However, further falls in prices are still likely, as “true” unemployment (to become clear after September) remains high for several years, government support measures and the bank payment holiday end after September, immigration falls and likely government measures boost housing construction. Our base case is for national average prices to fall around 5-10% into next year. Sydney & Melbourne are likely to see 10% falls as they are more exposed to immigration and have higher debt levels whereas Adelaide, Brisbane, Perth & Hobart are only likely to see small falls and Canberra prices are likely to be flat.

This may be seen as a reasonable outcome in terms of making housing more affordable but without posing a big threat to the economy (via a downwards spiral of falling prices and negative wealth effects on consumer spending) at the same time.

Never miss an update

Stay up to date with my content by hitting the 'follow' button below and you'll be notified every time I post a wire. Not already a Livewire member? Sign up today to get free access to investment ideas and strategies from Australia's leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Shane joined AMP in 1984 and is Chief Economist and Head of Investment Strategy. Shane has extensive experience analysing economic and investment cycles and what current positioning means for the return potential for different asset classes.

3 topics

Shane joined AMP in 1984 and is Chief Economist and Head of Investment Strategy. Shane has extensive experience analysing economic and investment cycles and what current positioning means for the return potential for different asset classes.

Expertise

Shane joined AMP in 1984 and is Chief Economist and Head of Investment Strategy. Shane has extensive experience analysing economic and investment cycles and what current positioning means for the return potential for different asset classes.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Investing for the biggest market shift since the GFC

Livewire Markets

Equities

Why ex-20 is the prime hunting ground for ASX returns

Livewire Markets