Backing a microcap software winner in the global horse racing wagering industry

<1.5x ARR for a founder-led software company dominating it's Australian niche with global ambitions.

The global horse racing wagering industry is a behemoth undergoing rapid change. The industry encompasses over 50 countries with an annual wagering turnover of more than $170bn, but technology is disrupting the distribution of betting services and gambling de-regulation is leading to an arms race to expand into new geographies. Industry players are continually looking to engage and adapt to technological change and there is an ASX-listed microcap at the forefront of this trend.

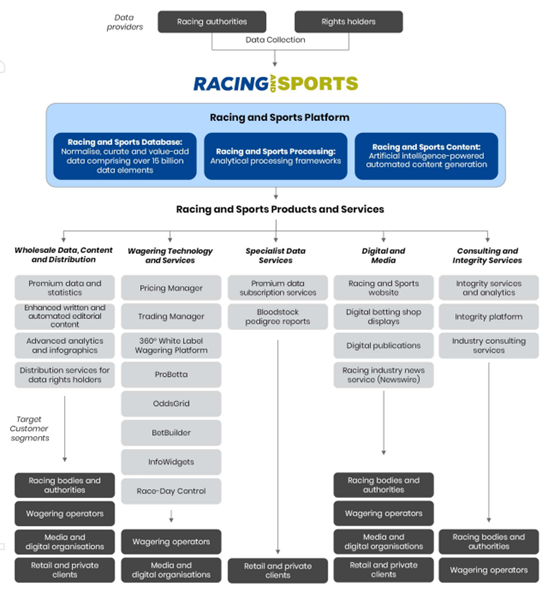

Racing and Sports Technology (ASX:RTH) was founded in 1999 by Gary Crispe and Robert Vilkaitis (who remain in the business as Chief Commercial Officer and Chief Technology Officer respectively with 17% shareholdings) as a data and information service provider across the global horse racing industry. RTH collects, processes and displays data from more than 1,800 racecourses covering over 270,000 races per year, with the company collecting more than 18bn data points since its inception. The chart below from the 2021 IPO sums up RTH’s positioning in the industry:

Growing the Core

RTH’s core business is the provision of what they term “Enhanced Information Services” to wagering and racing industry customers. RTH collects detailed data on lineage, ratings, speedmaps, race sectionals, race positions, jockeys, prices, scratchings and results. While a lot of this data is publicly available, RTH’s edge comes from the collation of the wide range of data, and the curation and presentation to create content for customers such as form guides and tips to drive wagering turnover and engagement.

Never miss an update

Get the latest insights from me in your inbox when they’re published.

Advertisement

The Enhanced Information Services segment is dominant in its core Australian market, with a ~90% market share of customers by wagering turnover. Tabcorp, Sportsbet, Ladbrokes/Neds, Bet365, PointsBet and BlueBet are all long-term customers and have expanded their agreements over time. RTH does have competition from fellow ASX-listed peer Betmakers Holdings (ASX:BET) in the segment, however unlike the founder-led RTH that has been run with fiscal discipline and the only external capital injection coming from the IPO, BET has grown through an aggressive acquisition strategy funded with frequent capital raises and large operating losses. Despite this, there is evidence RTH outcompetes BET given when BlueBet (RTH customer) and Betr (BET customer) recently merged, the combined entity chose RTH’s services and expanded its agreement. RTH management has stated they have not lost a tier one wagering operator customer in their 25 years of operation.

Emergence of Wagering Technology and UK Expansion

At the late 2021 IPO, Enhanced Information Services made up over 80% of RTH revenue, however the strategic plan was to grow an emerging "Wagering Technology" segment and embark on meaningful international expansion focused on the UK.

Wagering Technology is a segment that offers a full turnkey solution to wagering customers to outsource their trading and risk management for horse racing betting. The rapid emergence of digital channels to distribute betting services has meant the core competency for wagering operators is shifting from trading and risk management to customer acquisition and engagement. RTH has won customers such as Stake and Picklebet with Wagering Technology agreements, companies whose betting lives began in casino games and e-sports respectively. However, with an established and engaged user base they can fully outsource horse racing betting to parties such as RTH who provide a complete back-end solution and offer a new betting vertical for their customers.

Initially the Wagering Technology product used a strategic partnership with RacebookHQ to leverage their team of trading risk managers, however RTH has since built up their own automated capabilities which doesn’t require an external partner to deliver. At the conclusion of Picklebet’s initial contract at the end of 2024, RTH announced the new contract would be restructured without the involvement of RacebookHQ and I believe this restructure has been misunderstood by the market, creating the current opportunity in the share price which is discussed below.

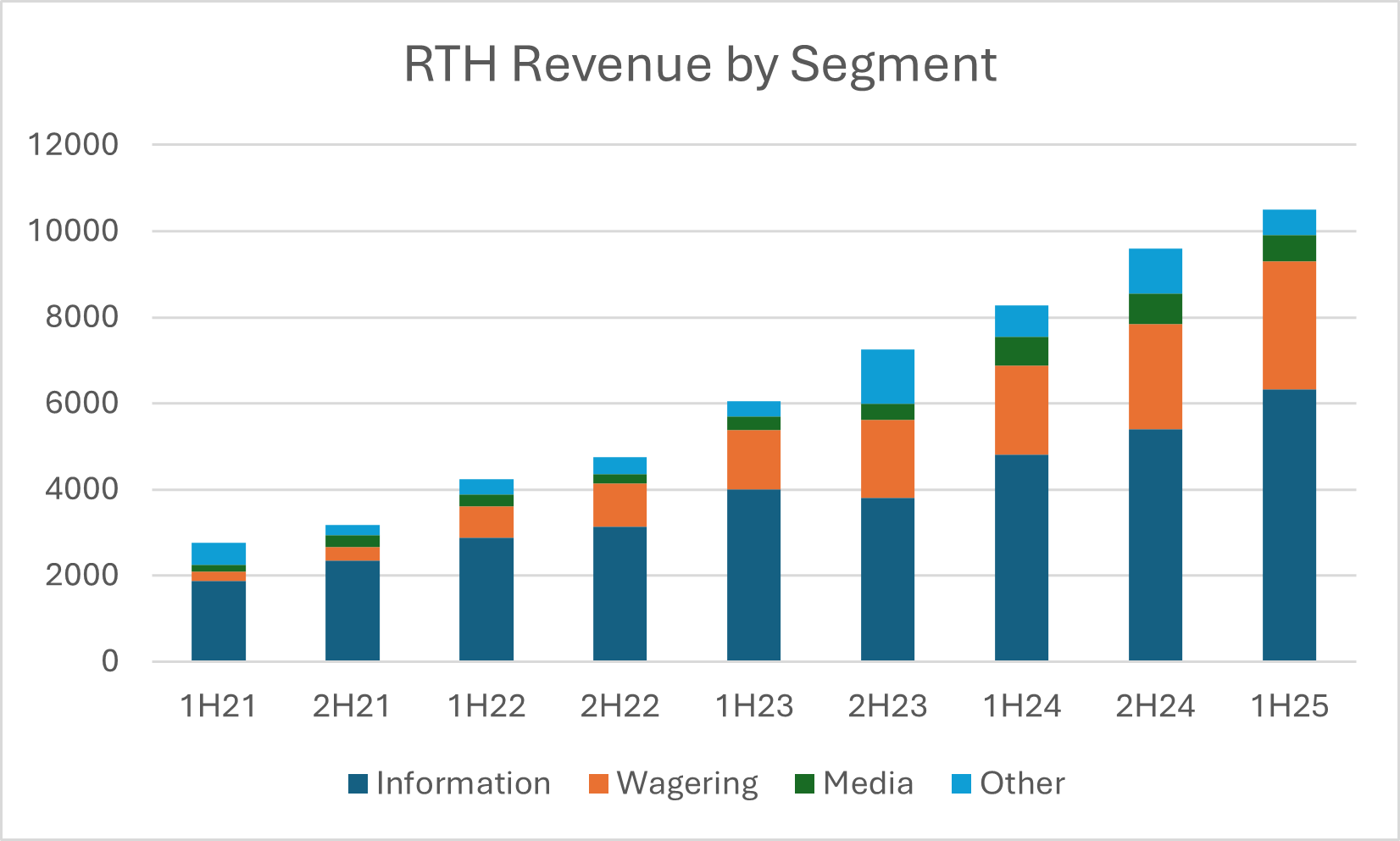

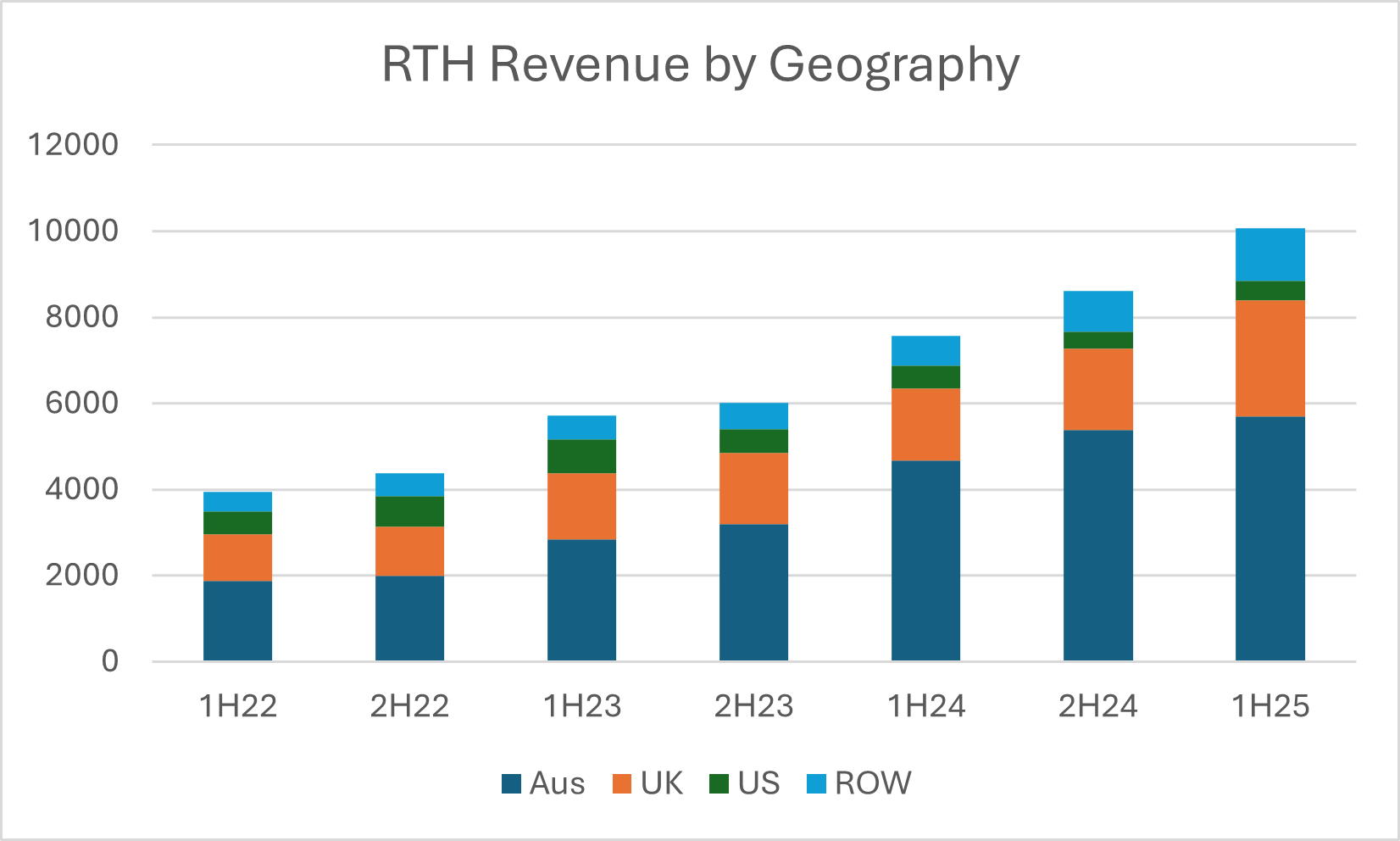

From IPO to FY24, RTH’s revenue has grown at 45% per year driven by contract expansions and the two growth pillars outlined at the IPO; Wagering Technology and UK expansion:

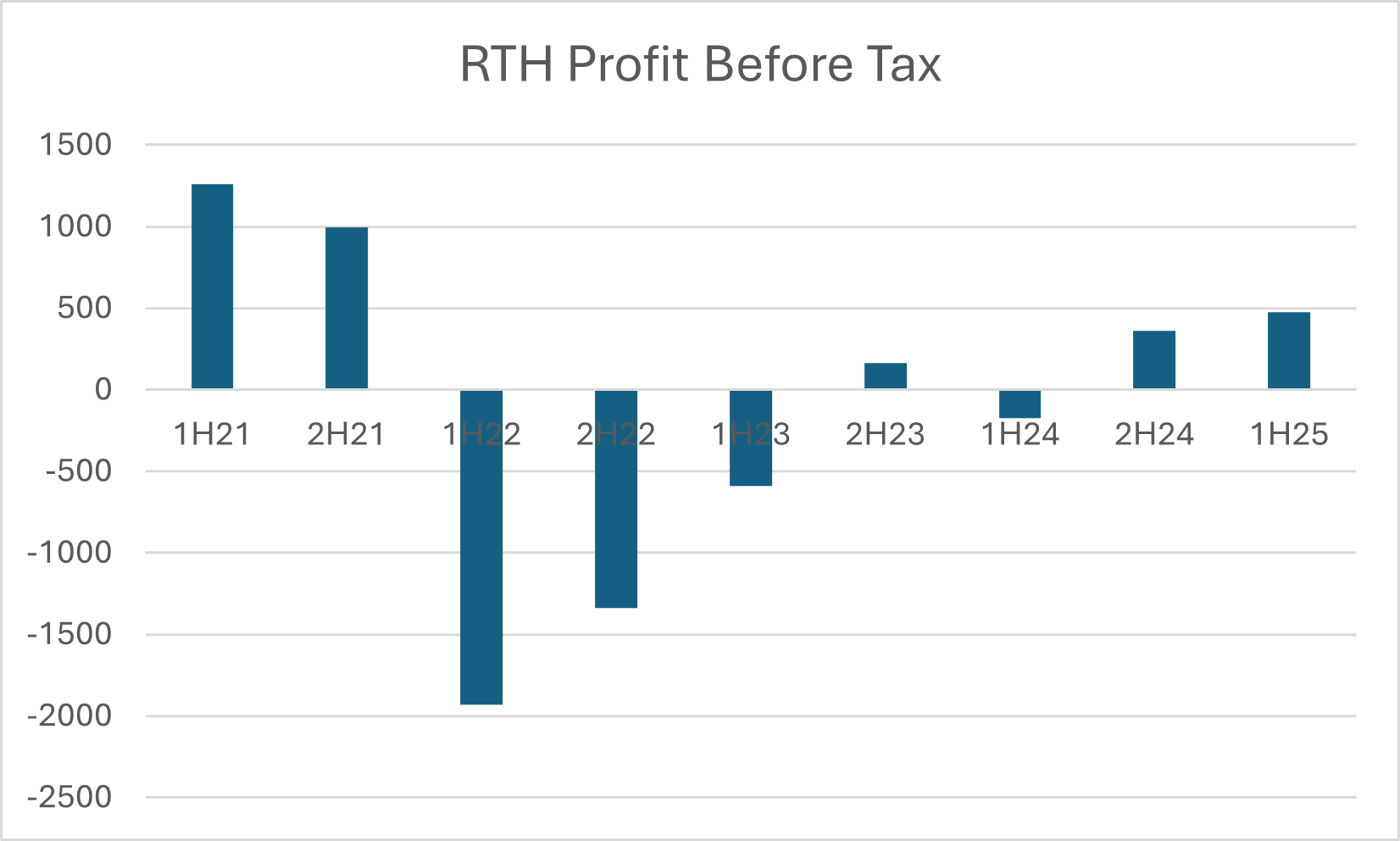

Importantly, after investing heavily to build out the capability to target international and vertical expansion, RTH is now scaling back towards profitability on the back of the impressive revenue growth. With a rolling twelve-month profit before tax of $800k, operating leverage is well and truly on show.

Falling ARR? Context is key

With any investment thesis it’s always important to take a step back and ask why does the opportunity exist? The attractive business qualities I’ve shown above aren’t completely unknown to the market, RTH’s consistent execution since listing was rewarded from mid-2023 to late-2024 as the share price rose more than three-fold from below 50c to $1.50. However, from that recent peak the share price has fallen nearly 50% to 80c today, with the fall exacerbated by the trading update for the start of the FY25 financial year provided at the recent AGM.

The main issue with the AGM update was annualised recurring revenue (ARR) falling from $18.9m at the end of June to $18.2m at the end of October. As I alluded to earlier, at the FY24 result RTH management disclosed that a key managed trading services customer (Picklebet) was transitioning to RTH’s in-house trading manager platform. The managed trading service previously offered by RTH used a delivery partner (RacebookHQ) which saw RTH charging low margin “passthrough” revenue to offset the costs of outsourced human trading risk decision-making systems.

With the launch of RTH’s in-house trading manager platform and Picklebet transitioning across to it, RTH no longer requires RacebookHQ’s trading risk team. The change impacts revenue with no material impact to profitability given the gross margin improves from ~45% to ~85%.

Despite being perfectly reasonable, the reason for the fall in ARR could have been explained better by RTH management, especially with respect to adjusting ARR growth for the change in Picklebet contract. Perhaps on the back of investor feedback, at the recent 1H25 results management provided a better like for like analysis, showing ARR growing 33% year on year when adjusted for the Picklebet transition.

Growth Drivers

Though the Picklebet transition has impacted headline ARR growth temporarily, RTH management remain confident of ARR and profit growth into 2H25 and beyond. Underpinning this confidence is the continued expansion of the managed trading services contract with key customer Stake. Commentary from RTH management is that the Stake deal has the potential to be the largest contract for RTH, but rather than being traditional fixed fee software ARR, revenue is generated as a percentage of net win through RTH’s full turnkey solution provided to Stake for their global racing offering.

Despite not being well known in Australia due to not having a gambling licence in the region, Stake is a global behemoth with industry sources estimating it may be as large as Bet365 for global wagering turnover. With management commenting Stake has the potential to be their largest contract, it is worth noting the current largest customer is Tabcorp which is worth ~$2m per year. Revenue generated through the Stake offering is expected to grow incrementally over time as RTH continually offers more races, geographies and exotic bet types through Stake.

Beyond Stake, partnership deals in the UK with gaming platform providers Playbook Engineering and Pragmatic Play for RTH to be their exclusive provider of racing data and trading services are expected to drive growth internationally. Playbook Engineering and Pragmatic Play provide white label wagering platforms, primarily for sports betting and casino games operators respectively. RTH now offers another betting vertical for global horse racing with DAZN Bet the most notable customer to onboard so far, the betting arm of global sports media giant DAZN.

RTH has also recently acquired six established Hong Kong data and media assets for $4m, establishing a foothold in the lucrative Asian market (now 17% of revenue, previously just 2%). RTH management expects significant synergies from the acquisitions with increased automation and price optimisation after a modest investment to upgrade products and systems. The acquisitions underpin the creation of a new subsidiary Racing and Sports Asia to target the large Hong Kong and Japanese racing markets, and the emerging Middle East.

Risks

Even with the consistent execution since listing, an investment in RTH is not without risk. With a focus on tier one wagering operators, it does mean RTH has high customer concentration with the top four customers contributing nearly half of revenue. Mitigating this is the long-term contracts (generally five or six years) and a proven history of extending and upgrading customers.

On-going industry consolidation has the potential to hurt RTH by reducing potential customer numbers, though management have noted so far consolidation has mostly come from the second and third tier players who have emerged in recent years, with little corporate action in the tier one space they primarily target.

The wagering industry is also a high risk for regulation, potentially impacting RTH’s contracts which rely on a percentage of net win if turnover is reduced in some way.

Finally, despite success with UK expansion since the IPO, the large incumbent data and information competitor is Podium (formerly the Press Association Media), a collective of 26 regional newspapers. RTH has an agreement with Podium to access the racing data which currently underpins their UK product offering, however it is a key risk to UK expansion how RTH manages competing against the incumbent that they currently rely on their data from.

Strategic Investors

It is worth noting the strategic investors currently on the RTH register. Entain (parent company of Ladbrokes and Neds) owns 10% from the IPO and Waterhouse VC owns 2% of the company through a strategic stake purchased at $1.19 with options at $1.40 to $1.89 strike prices vesting on Waterhouse VC introducing sales referrals, acquisitions or commercial deals to RTH that generate more than $10-35m in incremental revenue to RTH. Importantly, any introduction from Waterhouse VC is at RTH’s discretion whether they wish to pursue them.

Valuation

At the time of writing, RTH trades at a $39m market capitalisation (80c per share) with around $6m in cash after the recent acquisition of the Hong Kong data and information assets. With ARR of $21.9m at 1H25 and a rolling twelve months profit before tax of $1.3m (including the pro forma contribution of Hong Kong assets ex-synergy benefits and acquisition costs), RTH trades at just 1.5x EV/ARR and 25x EV/PBT, two multiples that signal extreme value for the consistent historical growth and future potential of a business with high margin recurring revenue. Perhaps you could say I have the view that RTH is worth a punt!

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Luke is founder of Merewether Capital and Portfolio Manager of the Merewether Capital Inception Fund, a micro cap boutique funds management firm.

........

Disclaimer: Any information contained in this article is limited to general information only, whilst the opinions and views detailed are those of the author only, and as such does not constitute advice or a recommendation in any capacity. The information contained in this article has not taken into consideration your specific financial needs, goals or objectives, so please consider consulting a licenced adviser before considering acting on this information.

Never miss an update

Get the latest insights from me in your inbox when they’re published.

2 topics

1 stock mentioned

Luke is founder of Merewether Capital and Portfolio Manager of the Merewether Capital Inception Fund, a micro cap boutique funds management firm.

Expertise

Luke is founder of Merewether Capital and Portfolio Manager of the Merewether Capital Inception Fund, a micro cap boutique funds management firm.

Expertise

Comments

Comments

Sign In or Join Free to comment