Beating inflation with private debt: who’s in your starting 11?

Recently, there’s been a lot of discussion about whether the significant government stimulus, combined with record low interest rates and unconventional monetary policy such as Quantitative Easing (QE) will finally result in rising inflation, something markets have not experienced for some time. After a number of false starts, it appears that almost every central bank is committed to these measures until they achieve their objective of realised inflation.

It’s a risk of which investors should be aware. On a practical level, it means taking a look to see whether the assets in your portfolio are still match-fit in an environment of rising inflation.

We have previously written on the critical role of the attacking defender as it relates to private debt illustrated through soccer, so we’ll extend this soccer team analogy to explore this dynamic and the role private debt can play to help investors navigate an environment of rising inflation.

Never miss an update

Get the latest insights from me in your inbox when they’re published.

Advertisement

Moving market dynamics

Long-duration assets like government bonds, infrastructure, property, and high-growth equities benefit when interest rates fall by lowering the discount rate applied to all their future cashflows. These are the first assets selected in your team when rates are falling. We have seen these champion investments perform exceptionally well over the bull market of the last 40-years when interest rates have dropped from double digits to near-zero levels.

With the potential for rates to rise from zero and with the prospect of inflation, it’s time for the coach and team manager – in markets, the portfolio manager – to make some difficult decisions about whether champion players in the twilight years of their career – for example sovereign bonds – should still be on the field, at least for the whole match. It may be time to re-evaluate whether your best past players are really your top choices going into a new season, or whether they should be retired, rested, or spend less time on the pitch because they’ve lost a yard of pace.

When inflation expectations rise, interest rates tend to increase, and the yield curve steepens. In these conditions, it’s an opportunity to reconsider whether some of the long duration assets that have been tried and tested players in the portfolio are still fit for purpose. It might be time for short duration asset classes such as private debt to step into their role in the team.

In a rising interest rate environment, the value of long-duration assets like fixed-rate corporate and sovereign bonds fall in value because their future cash flows are discounted further than before. This isn’t the case with private debt, which is short duration and senior secured debt, and in a rising interest rate environment does not fall in value, giving true diversification benefit.

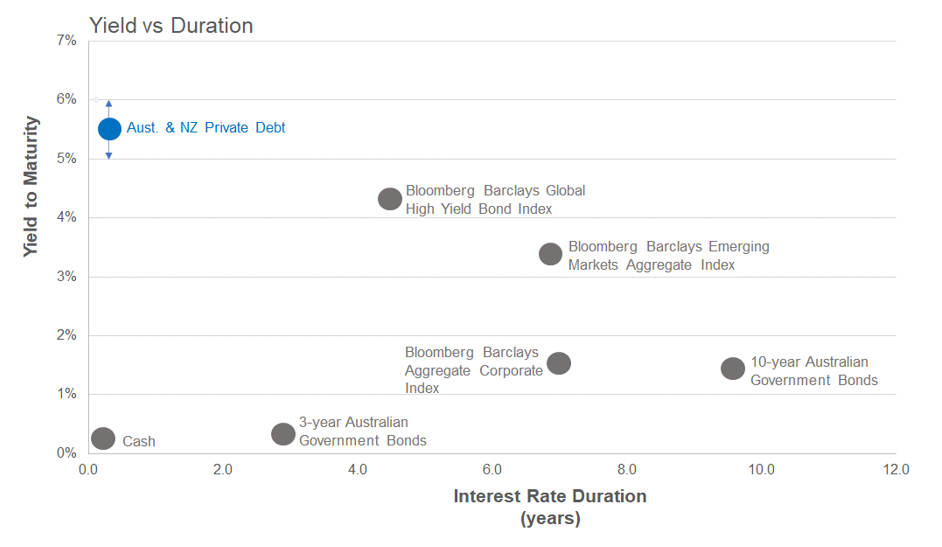

Australian & New Zealand Private Debt: Appeal in a rising rate environment

The chart below illustrates various credit and fixed income investments with differing levels of duration. The longer the duration, the more sensitive the investment valuation will be to interest rate changes.

Source: Revolution Asset Management and Bloomberg. ‘Aust & NZ Private Debt’ is based on realised investment experience of the Revolution private debt strategy from December 2018 to May 2021.

In fact, the overall yield of private debt rises in line with interest rate movements upwards because the total interest earned on the assets is the floating rate benchmark plus the credit margin, instead of a fixed-rate coupon. This is one of the most compelling reasons to consider an allocation to private debt in your current portfolio. The trade-off is that investors need to be comfortable with increased credit risk and the illiquidity that comes along with investing in private debt.

Like any soccer team, sometimes the coach or manager needs to bench certain assets because they don’t suit the playing conditions. But when conditions turn, it could be time to bring them back into the team. Gold is a good example, which has historically served as a store of value when inflation rises. Perhaps it’s also time to have an eye to the future and consider whether to promote up-and-coming players from the youth team. In this example, the coach or portfolio manager might examine whether an allocation to cryptocurrencies may add diversification to your portfolio in a QE world, but we’ll leave it to others to continue this debate.

Re-positioning for the times

Overall, what’s important is to have the right balance of attacking and defensive assets in a portfolio for the current conditions. You pick a different team when the game is played in rain and snow compared to when the conditions are fine. When it comes to investing, what’s important is to choose the right assets for the prevailing economic and market environment.

Think of private debt as the attacking defender or wingback in the team, it provides the right balance in a portfolio because it produces uncorrelated returns to other assets, as we demonstrated in our previous article. It’s an investment that’s first and foremost a defender that aims to preserve capital, but at the same time, it can contribute to the attack and goals in the form of regular income that can either be spent or used to re-balance.

Just as with soccer players, consistency is the key to selecting a fund manager that has the form for managing a portfolio through different conditions. At the same time, a good fund manager – and good players – will be well-balanced, durable and without weaknesses.

Private debt as an asset class is an especially attractive option, particularly when inflation is rising, something with which markets have not had to grapple for some time. Our goal is to be the attacking defender in investor portfolios by providing that winning and balanced combination of attack in the form of potential income, and defence in the form of aiming to provide capital preservation through all market cycles.

Not an existing Livewire subscriber?

If you're not an existing Livewire subscriber you can sign up to get free access to investment ideas and strategies from Australia's leading investors.

And you can follow my profile to stay up to date with other wires as they're published – don't forget to give them a “like

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Simon is responsible for portfolio selection and management and a co-founder of Revolution. Simon is an experienced private debt portfolio manager specialising in asset backed securities such as RMBS, CLOs, Consumer and Equipment ABS.

........

This article is for institutional and professional investors only and has been prepared by Revolution Asset Management Pty Ltd ACN 623 140 607 AFSL 507353 (‘Revolution’) who is the appointed investment manager of the Revolution Private Debt Fund I, the Revolution Private Debt Fund II and the Revolution Wholesale Private Debt Fund II (together ‘the Funds’). Channel Investment Management Limited ACN 163 234 240 AFSL 439007 (‘CIML’) is the Trustee and issuer of units for the Funds. Channel Capital Pty Ltd ACN 162 591 568 AR No. 001274413 (‘Channel’) provides investment infrastructure services to Revolution and Channel and is the holding company of CIML. None of CIML, Channel or Revolution, their officers, or employees make any representations or warranties, express or implied as to the accuracy, reliability or completeness of the information, including forecast information, contained in this document and nothing contained in this document is or shall be relied upon as a promise or representation, whether as to the past or the future. Past performance is not a reliable indication of future performance. All investments contain risk. This information is given in summary form and does not purport to be complete. To the extent that information in this document is considered advice or a recommendation to investors or potential investors in relation to holding, purchasing or selling units in the Funds please note that it does not take into account your particular investment objectives, financial situation or needs. Before acting on any information you should consider the appropriateness of the information having regard to these matters, any relevant offer document and in particular, you should seek independent financial advice. For further information and before investing, please read the relevant Information Memorandum available on request.

4 topics

1 contributor mentioned

Simon is responsible for portfolio selection and management and a co-founder of Revolution. Simon is an experienced private debt portfolio manager specialising in asset backed securities such as RMBS, CLOs, Consumer and Equipment ABS.

Expertise

Simon is responsible for portfolio selection and management and a co-founder of Revolution. Simon is an experienced private debt portfolio manager specialising in asset backed securities such as RMBS, CLOs, Consumer and Equipment ABS.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Investing for the biggest market shift since the GFC

Livewire Markets

Equities

Why ex-20 is the prime hunting ground for ASX returns

Livewire Markets