Bellbottoms and the Nifty Fifty

It was the 1970s - ‘72 to be exact, and apart from Gough Whitlam coming to power in Australia, Watergate in the US, and bellbottoms everywhere, it was the height of the Nifty Fifty (not to be confused with the Nifty 50 Index of India stocks). The idea that investors needed only to buy 50 of the most popular growth stocks and hold them forever.

Plenty bought in and with good reason, with the index including names such as Xerox, IBM and Coca-Cola - all with proven growth records and continual increases in dividends.

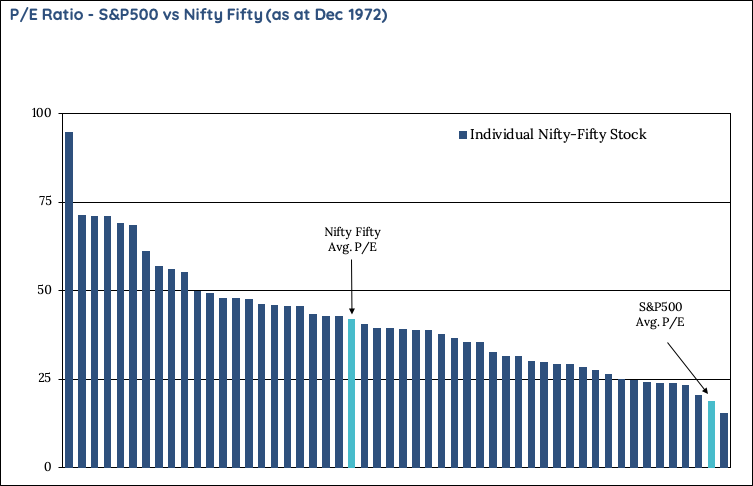

However, at their peak in 1972, the Nifty Fifty traded at 41.9 times earnings, more than double the S&P's then average of 18.9x.

Source: AAII Journal October 1998

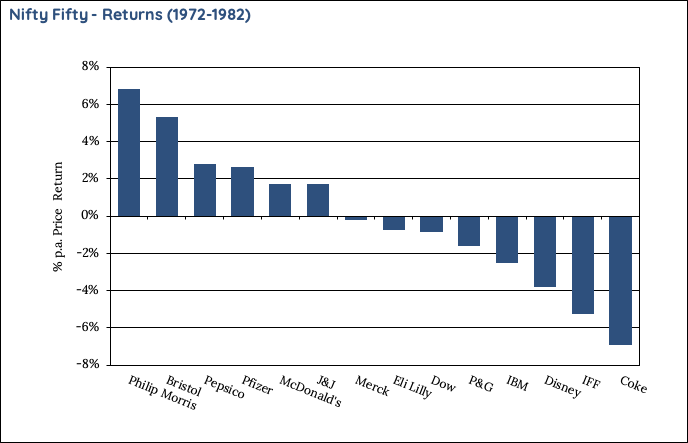

Two years later, the same year President Nixon resigned, those investors who had bought in 1972 had lost 60% of their investment. While they were mostly still good companies, for some of them such as Coke, Disney and Merck they still hadn’t recovered their price 10 years later. By then bellbottoms were also out of favour.

Importantly inflation averaged around 8% p.a. throughout this period, further highlighting the extent of real wealth that was destroyed.

Source: Bloomberg, AAII Journal October 1998

So what drove this lacklustre 10 years?

A combination of factors was likely at play including geo-political tension, inflation, rising interest rates (peaking at 19.1% in June 1981) and a series of oil shocks. These factors are arguably all at play today for those buying the index.

As I’ve written before, the current S&P 500 FAANMGs are dominating and therefore skewing the overall performance of the index, with an average P/E of over 44x, against just around 26x for the index – and 23x for the index excluding the FAANMGs. In addition, the environment today for a period of inflation, even minor is the strongest in decades.

If any of these factors from the 1970s take hold, those that have bought in recently might have a long wait to recover their investment.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Chad is the Co-Chief Investment Officer and co-founder of Talaria Asset Management. He has more than 21 years of experience in the financial services industry in the UK, South Africa and Australia. Talaria's investment strategy seeks to increase the certainty of global equity returns for investors through its:

> Unique and structurally lower-risk investment approach that combines capital growth and income generation to deliver a more consistent return profile (smoothing).

> Portfolio of up to 45 large, globally listed companies.

> Internationally experienced and personally invested leadership team.

www.talariacapital.com.au

........

The information in this article is general information only and is not based on the objectives, financial situation or needs of any particular investor. In deciding whether to acquire, hold or dispose of the product you should obtain a copy of the current Product Disclosure Statement (PDS) for the Fund and consider whether the product is appropriate for you.

Wholesale Units in the Talaria Global Equity Fund (the Fund) are issued by Australian Unity Funds Management Limited ABN 60 071 497 115, AFS Licence No. 234454. Talaria Asset Management Pty Ltd ABN 67 130 534 342, AFS Licence No, 333732 is the investment manager and distributor of the Fund. References to “we” means Talaria Asset Management Pty Ltd, the investment manager. A copy of the PDS is available at australianunity.com.au/wealth or by calling Australian Unity Wealth Investor Services team on 13 29 39. Investment decisions should not be made upon the basis of the Fund’s past performance or distribution rate, or any ratings given by a rating agency, since each of these can vary. In addition, ratings need to be understood in the context of the full report issued by the rating agency itself. The information provided in the document is current at the time of publication.

3 topics

Chad is the Co-Chief Investment Officer and co-founder of Talaria Asset Management. He has more than 21 years of experience in the financial services industry in the UK, South Africa and Australia. Talaria's investment strategy seeks to increase...

Expertise

Chad is the Co-Chief Investment Officer and co-founder of Talaria Asset Management. He has more than 21 years of experience in the financial services industry in the UK, South Africa and Australia. Talaria's investment strategy seeks to increase...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

What a 40% year taught us: 4 lessons from the past 12 months (and 3 new stocks to buy)

Seneca Financial Solutions