TOL - 10th Dec, 2024

Big brokers warn of “generational” overvaluations in ANZ, Commonwealth Bank, NAB and Westpac

Should you hold your bank shares? Should you sell them? Should you buy more, and if so, which ones?

In Part 1 of this three-part foray into the performance, valuations, and potential future direction of ASX bank stocks, we investigated just how good their returns over the last 12-months have been.

We learned that for several of our major ASX banks, like ANZ Group (ASX: ANZ), Commonwealth Bank of Australia (ASX: CBA), National Australia Bank (ASX: NAB), and Westpac Banking Corporation (ASX: WBC), their 2024 returns are many standard deviations from the mean as measured over the last decade.

The data suggests the collective performance of ASX bank stocks this year is extraordinary from a historical perspective, but as they say in the investment disclaimer classics – past performance is no indicator of future performance. There’s no reason these stocks cannot pull off a repeat in 2025, take a breather, or crash and burn.

This is the topic of the concluding articles in this series: What can investors expect from their ASX bank stocks in 2025? To answer this question, today we’ll investigate what the biggest and most respected market analysts think about the prospects for ASX bank stocks. On Monday we’ll finish by conducting an in-depth technical analysis of each of their charts.

Do the big brokers believe ASX bank stocks can repeat 2024’s stellar performance in 2025?

Let’s check in with what the big brokers say about the banks collectively.

UBS

(From: “Australian Banks - Will 2025 offer a second bite at the cherry?”, 2 December 2024)

- UBS notes that Australian bank share prices outperformed the broader market as measured by the S&P/ASX200 by around 30% year to date, despite sector aggregate return on equity (“ROE”) contracting 79 basis points and FY24 earnings dipping 5% compared to the same period last year.

- The broker points to “animal spirits” and “flow-driven momentum” as the two major reasons behind bank sector outperformance.

- Looking forward, the outlook for sector earnings and ROE for 2025 is “not much better” than 2024, with cash earnings per share (“EPS”) expected to grow just 2%, and ROE to be flat.

- Despite this, the broker is looking to “gain exposure” to the sector’s strong performance via WBC, which it upgrades to BUY from NEUTRAL.

Citi

From: “Australia Banks 2024 in Review: The dislocating effect of inflation on total returns”, 29 November 2024)

- The broker describes the performance of ASX banks as “stunning” and as “undoubtedly the investment story of 2024”. Also, this is their best year’s performance since 2009 (as the whole market was emerging from the GFC).

- The sector’s massive market-beating returns occurred “much to the chagrin of many institutional investors” because EPS and dividend growth “was almost non-existent”.

- The only key financial metric that did grow for the bank sector (is one which, as an investor, you’d prefer not to grow) was its PE Ratio, which increased to an “unprecedented” 18.6 times earnings.

- The broker suspects the driver of the outperformance was “likely the dislocating impact of excess inflation, which increased equity market inflows, which found its way into banks.”

- Looking into 2025, the broker expects “generational high” valuations, combined with “downside risks to earnings”, justifies continued caution towards the sector, as well as the broker’s blanket SELL rating on each of its major constituents.

Macquarie

(From: “Australian Banks - Less than meets the eye”, 29 November 2024)

- “While lacking a negative short-term catalyst, we see medium-term downside risks to earnings and share prices as eventual RBA cuts weigh on margins and sentiment. Given stretched valuations, we retain our Underweight view of the sector”

- The broker maintains its blanket sell rating on the sector

Broker Consensus for ASX bank stocks

Let’s now cast the net wider on the broker views and valuations front. Find below the latest Broker Consensus tables for each of the major ASX bank stocks. Note, all broker ratings and targets are taken from broker research notes collected since July 1 for currency. There are two components of Market Index’s Broker Consensus data: Broker Consensus Rating and Broker Consensus Target.

To obtain a stock’s Broker Consensus Rating, we assign a value of +1 to any rating better than HOLD/NEUTRAL/MARKETWEIGHT, a value of 0 for any rating equivalent to HOLD/NEUTRAL/MARKETWEIGHT, and a value of -1 to any rating worse than HOLD/NEUTRAL/MARKETWEIGHT.

We then take the average of all assigned rating values and assign a Broker Consensus Rating of BUY to values greater than +0.5, a rating of HOLD for values between -0.5 and +0.5, and a rating of SELL for values less than -0.5.

The Broker Consensus Target is simply the average of the target prices we have on file for each broker. Typically, brokers define their target prices as a 12-month forecast. Each target price is based on fundamental valuation assumptions.

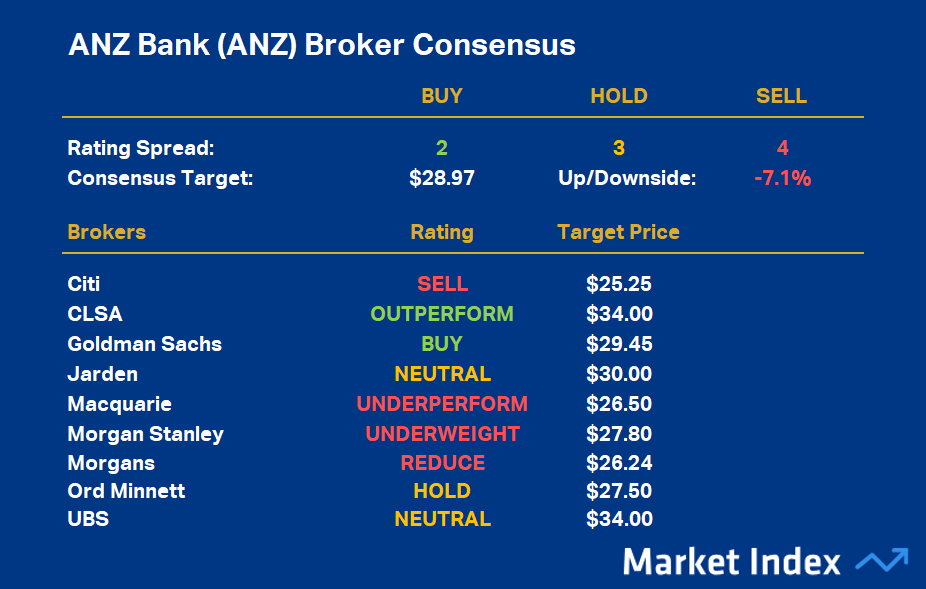

ANZ Group (ASX: ANZ)

%20Broker%20Consensus.png)

ANZ’s broker consensus rating is -0.22, resulting in a Broker Consensus Rating of HOLD. Its Broker Consensus Target is $28.97. This suggests brokers collectively believe the stock is around 7.1% overvalued based upon the closing price on Thursday, 5 December of $31.18.

Bendigo and Adelaide Bank (ASX: BEN)

%20Broker%20Consensus.png)

BEN’s broker consensus rating is -0.10, resulting in a Broker Consensus Rating of HOLD. Its Broker Consensus Target is $11.11. This suggests brokers collectively believe the stock is around 18.1% overvalued based upon the closing price on Thursday, 5 December of $13.56.

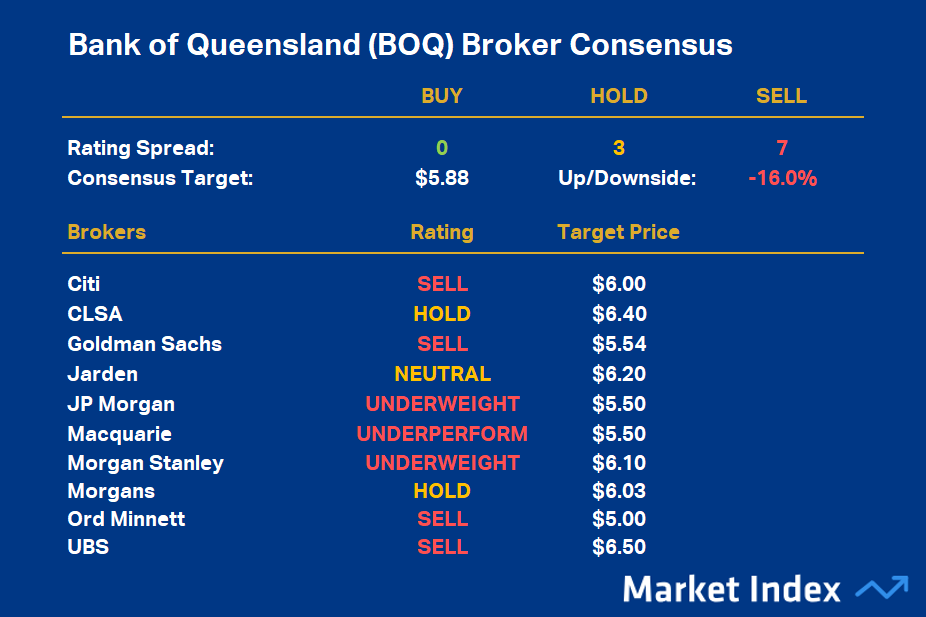

Bank of Queensland (ASX: BOQ)

%20Broker%20Consensus.png)

BOQ’s broker consensus rating is -0.70, resulting in a Broker Consensus Rating of SELL. Its Broker Consensus Target is $5.88. This suggests brokers collectively believe the stock is around 16.0% overvalued based upon the closing price on Thursday, 5 December of $7.00.

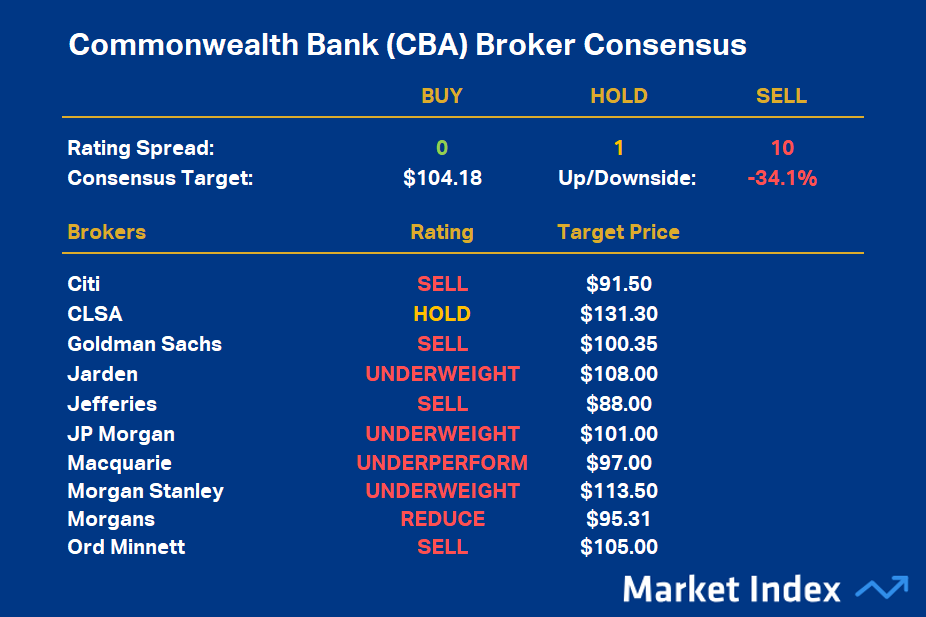

Commonwealth Bank of Australia (ASX: CBA)

%20Broker%20Consensus.png)

CBA’s broker consensus rating is -0.91, resulting in a Broker Consensus Rating of SELL. Its Broker Consensus Target is $104.18. This suggests brokers collectively believe the stock is around 34.1% overvalued based upon the closing price on Thursday, 5 December of $157.99.

National Australia Bank (ASX: NAB)

%20Broker%20Consensus.png)

NAB’s broker consensus rating is -0.20, resulting in a Broker Consensus Rating of HOLD. Its Broker Consensus Target is $33.81. This suggests brokers collectively believe the stock is around 13.2% overvalued based upon the closing price on Thursday, 5 December of $38.94.

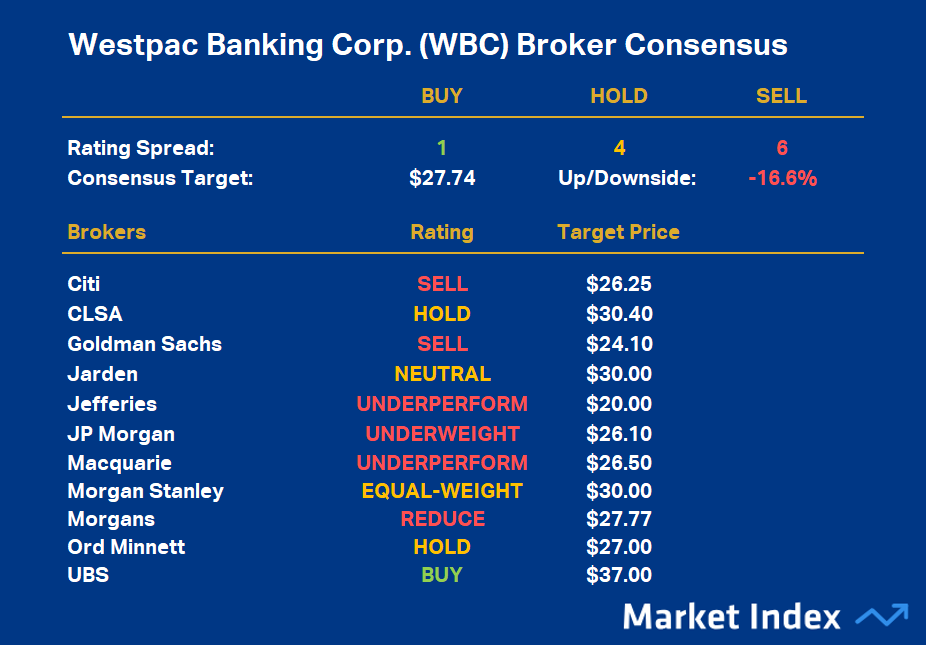

Westpac Banking Corporation (ASX: WBC)

%20Broker%20Consensus_updated.png)

WBC’s broker consensus rating is -0.45, resulting in a Broker Consensus Rating of HOLD. Its Broker Consensus Target is $27.74. This suggests brokers collectively believe the stock is around 16.6% overvalued based upon the closing price on Thursday, 5 December of $33.24.

Conclusions

Clearly, the major brokers have a very dim view of ASX bank stocks generally, with consensus HOLD-rated ANZ the least overvalued (-7.1% return at Broker Consensus Target to current price), and consensus SELL-rated CBA the most overvalued (-34.1% return at Broker Consensus Target to current price).

It’s worth noting that the most recent upgrade for any bank’s rating came just last week from UBS for WBC. As mentioned above, it upgraded the stock to BUY from NEUTRAL. Coincidentally, WBC also copped the most recent downgrade of any bank, via Morgans, who moved its rating to REDUCE from HOLD.

It’s fair to say that, for the most part, despite a few minor tweaks along the way, the brokers have generally maintained their current bearish stance towards ASX bank stocks for most of this year. Based upon the rhetoric in their most recent research reports, I personally don't get the feeling they're going to change this stance any time soon.

This implies the best informed and trained analysts that cover the Australian stock market expect the share prices of ASX bank stocks to fall in 2025.

We’ll conclude our investigation into the performance, valuations, and potential future direction of ASX bank stocks on Monday when we delve into their technical analysis factors. Has the technical approach done any better than the fundamental valuation approach discussed here, and can we expect the incredible performance of ASX bank stocks to continue in 2025?

This Part 2 of a three-part foray into the performance, valuations, and potential future direction of ASX bank stocks.

Click here to read Part 1 which investigates what the biggest and most respected market analysts think about the prospects for ASX bank stocks now and into 2025.

Click here to read Part 3 which investigates what the charts say about the prospects for ASX bank stocks with detailed technical analysis of each.

This article first appeared on Market Index on Friday 6 November 2024.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl has a passion for technical analysis and has taught his unique brand of price-action trend following to thousands of Aussie investors.

........

Investing is risky. Inevitably you will endure losses. If you can't cope with losing, don't invest.

%20Broker%20Consensus.png){kind=link}

%20Broker%20Consensus.png){kind=link}

%20Broker%20Consensus.png){kind=link}

%20Broker%20Consensus.png){kind=link}

%20Broker%20Consensus.png){kind=link}

%20Broker%20Consensus_updated.png){kind=link}

5 topics

6 stocks mentioned

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl...

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl...

Comments

Comments

Sign In or Join Free to comment