Get ready for volatility - Vimal Gor at Livewire Live 2017

As the era of QE draws to a close, central bankers face a conundrum: Nearly a decade of money printing has suppressed volatility… So, as QE is withdrawn, is volatility inevitable?Vimal Gor, Head of Income and Fixed Interest at BT, argues that the market has a bumpy ride ahead.

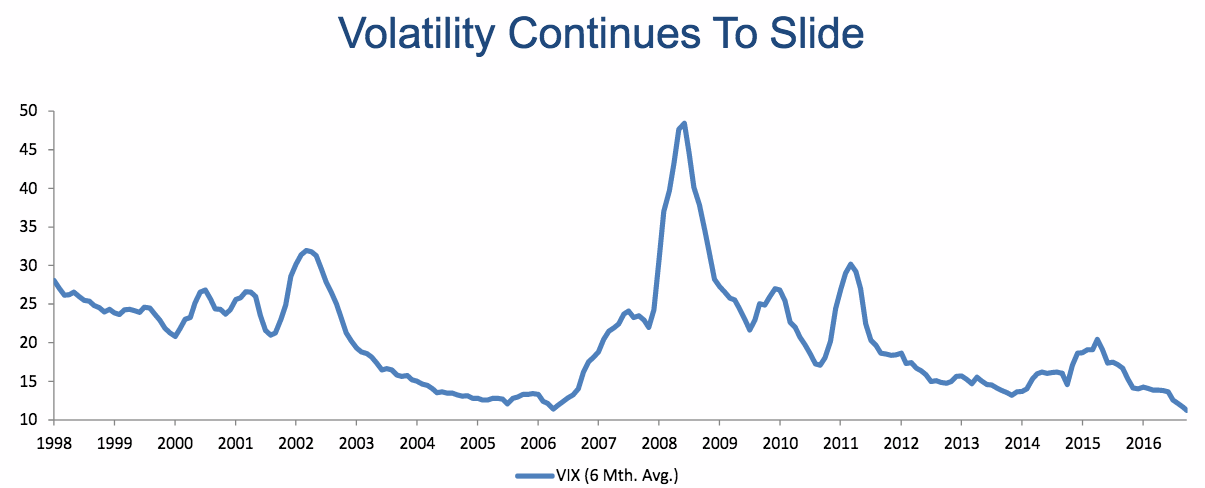

Volatility, as measured by the VIX has been in a steady downtrend for most of the last nine years. The VIX uses options on the S&P500 to measure the market’s expectations of volatility over the next month. But, even though the market is facing half a dozen major global geopolitical risks, volatility is somehow still on the floor.

“I can show you twenty or thirty other charts, all of them showing you that equity volatility is super-cheap. And it's at 9.5 on the VIX, the lowest it’s been since 1993. And the six-month moving average is the lowest its ever been.”

So why is volatility so low? For one thing, there is a new class of trader in the market playing, and contributing to, this trend:

“You can make better returns selling volatility forward and rolling it down as a systematic strategy, than you can yielding on an investment grade bond in the US”.

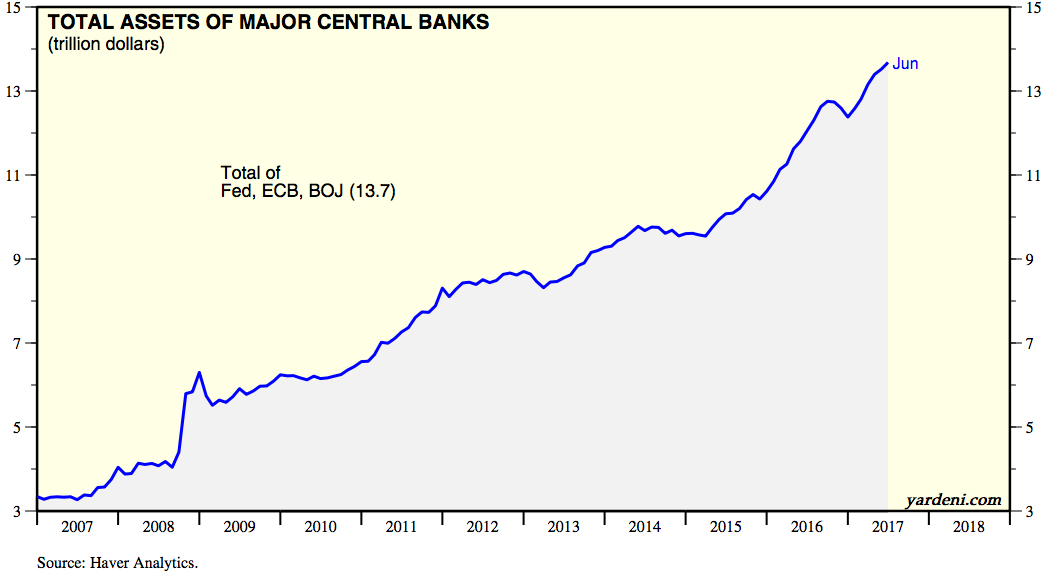

The other key driver is, of course, the river of printed money that has flowed into the market since the GFC from the main central banks. This chart published by Yardeni yesterday shows the extent of this. The aggregate balance sheet of The Fed, the Bank of Japan, and The European Central Bank has grown from $US3.2 trillion to $13.7 trillion over the last decade, with the ECB driving the growth at present.

Source: (VIEW LINK)

However, while QE was effective at averting a recession, it is proving to be less and less effective at stimulating growth, and is starting to cause the problems it was intended to solve. And as things stand today, yields have been pushed down so far that investors across all asset classes are finding it hard to generate returns.

“If you look at a balanced portfolio, 60:40, in the US or in Australia, it is unlikely to return a real return over the next ten years, that is how bad yields are, and how richly priced assets are right now. And that’s a function of QE.”

In his presentation at Livewire Live, Vimal Gor, argued that following the ECB forum on central banking in Sintra, Portugal, we are now seeing a co-ordinated response aimed at getting interest rates back up, and stopping QE.

The question is whether they can do this, without volatility returning to the market, however, as Vimal told the audience: “We are at a point where volatility should start picking up, now”.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Livewire Exclusive brings you exclusive content from a wide range of leading fund managers and investment professionals.

3 topics

Livewire Markets

Livewire Exclusive brings you exclusive content from a wide range of leading fund managers and investment professionals.

Expertise

Livewire Markets

Livewire Exclusive brings you exclusive content from a wide range of leading fund managers and investment professionals.

Expertise

Comments

Comments

Sign In or Join Free to comment