TOL - 18th Oct, 2024

Bullish investor sentiment is up the most in 4 years. Here's what caused it

...and everyone is piling into stocks as a result.

When investors reflect on the last month in financial markets, it's reasonable to assume that September provided the closest thing to a "perfect storm" for market bears. The combination of a jumbo Federal Reserve rate cut, the largest Chinese fiscal and monetary stimulus announcements in four years, and resilient economic growth data sparked a 4%+ rally in the S&P 500 and a 29 basis point fall in the US 10-year bond yield (peak to trough.)

All this is made even more remarkable by the fact that September is, historically, a seasonally difficult month for risk assets.

Accordingly, professional investors told the latest edition of the Bank of America Fund Manager survey that they had shifted from bearish to bullish. The shift was the largest, by magnitude, in more than four years. And the records didn't stop falling there.

In this wire, I'll take you through the results of the latest BofA FMS.

To give you a sense of just how influential this survey is, 195 participants who manage over US$500 billion in assets under management responded to the Global Fund Manager Survey alone. Note that this does not include all the participants who participated in the regional FMSs (Australia is part of the Asian region FMS.)

Records falling all over the place

- Sentiment (a measure based on cash levels, equity allocation, and economic growth expectations) rose from 3.8 to 5.6, its largest monthly rise since June 2020.

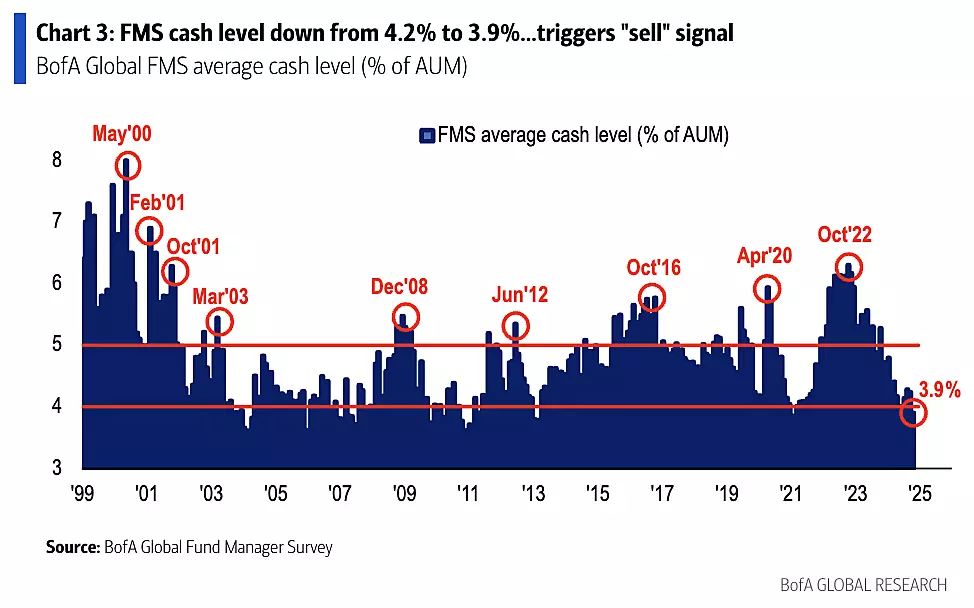

- Cash levels fell from 4.2% to 3.9%, the lowest level since February 2021

- Global growth expectations recorded its fifth (5th) largest one-month jump since 1994

Of note, global growth expectations as per this survey and the S&P 500 have had an interesting correlation in the past. But generally speaking, post the dot-com bubble of the early 2000s, rising asset prices have typically been informed by higher economic growth expectations which, in turn, inform rising asset prices and so on.

- BofA Bull & Bear Indicator up to 7.1, shy of the "sell signal" of 8.0.

...which flowed through to record asset allocation changes

- Allocation to global stocks (inflows) surged the most in one month since June 2020

- Within stocks, the move has been to move out of defensives into cyclicals. They've obviously been reading the notes of JPMorgan's Dubravko Lakos-Bujas, who noted that it was time to do exactly the same thing recently.

- Meanwhile, allocation to bonds went from +11% overweight to -15% underweight (outflows) - the biggest drop on record

But where are they allocating?

When BofA asked these fund managers where they would invest, assuming there were more Chinese stimulus announcements on the way (for the record, their team are actually advising clients to buy the dips in the Chinese stock market at the moment), the fund managers offered the following:

Most investors would pile into emerging market equities (note EM in this case means EM ex-China) and hard commodity investments. They also said the biggest losers from this trade would likely be bonds and Japanese equities - the latter is understandable given the near-24% rally we've seen in Japanese stocks over the past 12 months.

Geopolitics risk is the top tail risk - but not everyone is hedging their bets

In this survey, the BofA team also asked fund managers to share where they think the most crowded trades are, as well as the top risks and what they are doing about them.

Geopolitics is top of mind, given the US election is around the corner and the wars in Ukraine and the Middle East continue to occupy investors' attention. But what is perhaps most remarkable is how much the top tail risks have shifted in just the past couple of months. Last month, the US recession was the top tail risk for investors. It now ranks third. Concerns over accelerating inflation also continued to rise, from 18% to 26%.

But when asked if the US election was going to change their trading decisions, this is how the fundies responded:

The contrarian trades

Finally, I always like to wrap up my write-up of the Fund Manager Survey with the contrarian trades. Because who doesn't love a contrarian trade, right?

No landing scenario:

- European over US equities

- Materials stocks over healthcare stocks

Hard landing/recession scenario:

- Products that would flatten the long end of the bond yield curve (A 'flat' shape for the yield curve occurs when short-term yields are similar to long-term yields, and would imply trouble brewing on the horizon.)

- Bonds over stocks

- Long staples over industrials

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

This is an archived profile. Hans was a senior editor at Livewire Markets from April 2022 to February 2025.

........

Livewire gives readers access to information and educational content provided by financial services professionals and companies (“Livewire Contributors”). Livewire does not operate under an Australian financial services licence and relies on the exemption available under section 911A(2)(eb) of the Corporations Act 2001 (Cth) in respect of any advice given. Any advice on this site is general in nature and does not take into consideration your objectives, financial situation or needs. Before making a decision please consider these and any relevant Product Disclosure Statement. Livewire has commercial relationships with some Livewire Contributors.

2 topics

This is an archived profile. Hans was a senior editor at Livewire Markets from April 2022 to February 2025.

Expertise

This is an archived profile. Hans was a senior editor at Livewire Markets from April 2022 to February 2025.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management