Cheapest vs most expensive ASX sectors – Where are the bargains?

We investigate the cheapest and most expensive ASX sectors as we move into what is typically the strongest period of the year for stocks.

October often gets a bad rap in terms of stock market performance, given the month has hosted some of the biggest market crashes in history. Fortunately, this October was far from a disaster, although its 1.3% decline in the S&P/ASX 200 (XJO) was the second worst monthly performance in the benchmark index in a year.

Perhaps the disappointment for Aussie investors this October, is that the month contained a string of record highs with the XJO tipping 8,300 for the first time. Yes, we were only down 1.3% for the month, but by Friday’s close we were down 3.2% from the 8384.5 all-time high set on 17 October.

I ran a poll last week to test investors' resolve when the market makes a new high. 33.7% said that their mindset was generally “Too late to buy/Stay out”, 18.8% said it’s “Time to sell/Go short”, and 47.5% said it was time to “Buy/Full risk position”. It seems investors are roughly 52.5-47.5 skewed to abstaining or selling around a new market high.

Some of the recent concerns over Aussie stocks making new highs have been around valuations. An article I wrote recently suggested that stock prices were not rising commensurately with earnings. If you’re one of the investors who is concerned about whether the Australian share market is presently representing good or bad value, then this is the article for you.

Let’s check in to see where the major ASX sectors are placed as we head into the end of the year in terms of valuations and earnings growth forecasts. Q: Are there any bargain sectors left for Aussie investors to choose from?

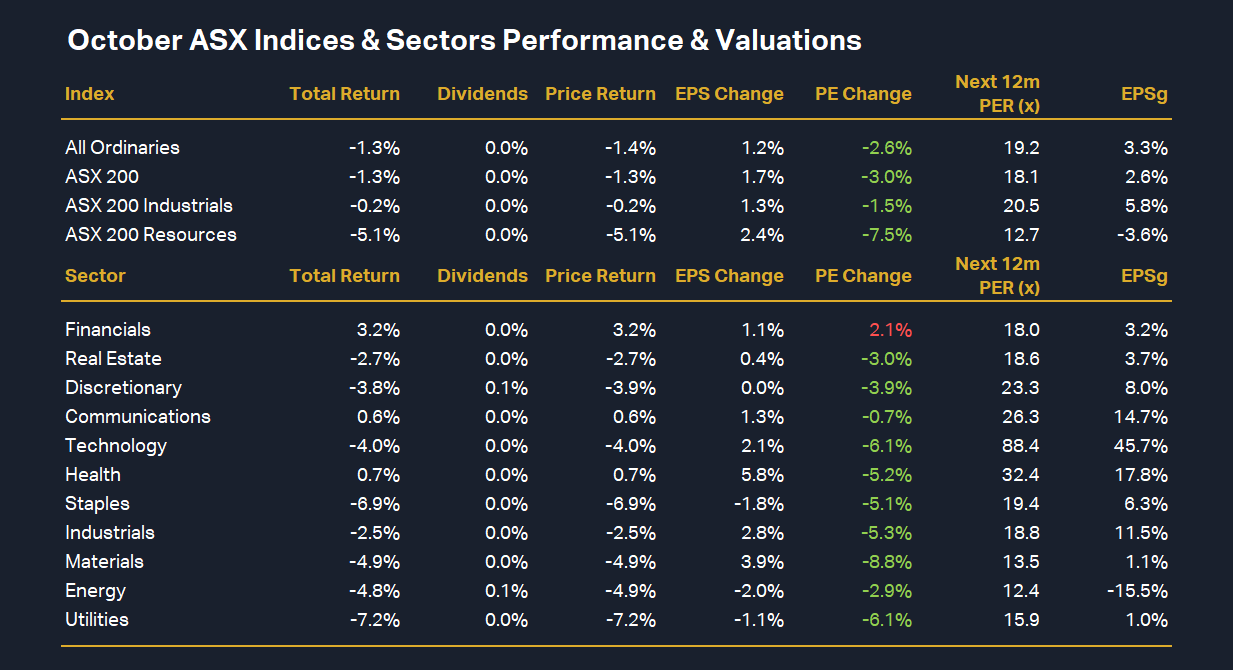

Cheap versus Expensive ASX Sectors

Cheap versus Expensive ASX Sectors Table. Sources: FactSet, Macquarie Research, November 2024. (From Macquarie Research, “Australian Equity Strategy October Equity Market Review”, 1 November 2024) (click here for full size image)

How to read the Cheap versus Expensive ASX Sectors Table

- Total Return: The percentage change in the index/sector in October

- Dividends: The percentage return from dividends only paid by stocks within the index/sector in October

- Price Return: The percentage return from the change in the price only of the index/sector in October

- EPS Change: The percentage change in the Next 12 Month Consensus forecast earnings per share (EPS) for the index/sector in October

- PE Change: The percentage change in the Next 12 Month Consensus forecast price to earnings ratio (P/E Ratio) for the index/sector in October

- PER (x): The Next 12 Month Consensus forecast P/E Ratio for the index/sector in October (“x” stands for “times earnings”)

- EPSg: The Next 12 Month Consensus forecast earnings per share growth for the index/sector in October (note this is how much the index/sector’s earnings is expected to grow in the next 12 months)

Good news Aussie investors, from an index point of view, the Cheap versus Expensive ASX Sectors Table suggests Australian stocks generally got cheaper in October.

This is implied by a 1.3% decline in both the All Ordinaries Index (XAO) and the XJO, while at the same time forecast earnings increased by 1.2% and 1.7% respectively – therefore reducing the index PER (x) for each to 19.2 (-2.6% from 19.5) and 18.1 (-3.0% from 18.4) respectively.

To put these values into context, over a very long period of time, Australian benchmark index P/E Ratios of 10 and below have been considered cheap, 15 has been considered fair value, and 20 and above has been considered expensive. So, this data implies that Aussie shares have pulled back from near-expensive levels in October. They’re still much closer to expensive than fair value, however.

On the subject of expensive, ASX 200 Industrials stocks could be argued to be exactly this given their 20.5x PER (x). On the other hand, ASX Resources could be argued to be on the right side of fair value (perhaps even close to cheap) given their PER (x) of 12.7x.

Note though, the all important last column: the EPSg column. The consensus among analysts is that earnings of Industrial companies are expected to grow around 5.8% over the next 12 months compared to a 3.6% decline for Resources. Investors tend to pay more for growing earnings than contracting earnings.

With these metrics in mind, let’s now take a look at each of the major ASX sectors in the Cheap versus Expensive ASX Sectors Table:

Financials: a stable performer

The Financials sector emerged as the strongest performer in October by a long way – gaining 3.2% vs next best Health's 0.7% increase, and the worst performing sector Utilities' 7.2% decline. Yes, prices increased in Financials, but so too did 12 month forecast earnings, by 1.2%. Still, given prices rose faster than forecast earnings, the sector P/E Ratio rose to 18.0x from 17.5x in September. EPSg is a modest +3.2%.

Q: Cheap versus Expensive?

View: Hardly cheap, but not completely out of whack with valuations since 2020. If we look longer term, the Financial sector's P/E Ratio is typically closer to low-teens than high teens. Still, there's likely a quality and stability factor at play here Aussie investors continue to be drawn to (the sector is dominated in terms of market capitalisation by major banks and insurance companies).

Real Estate: rising rate concerns

In contrast, the Real Estate sector faced considerable headwinds in October as market yields rose sharply. Rising market yields are usually bearish for real estate stocks because it increases their costs of borrowing and also reduces the attractiveness of their income streams compared to risk-free bonds.

This resulted in the sector posting a negative total return of 2.7% in October. On a positive note, EPS change was a positive 0.4%, meaning Real Estate's PER (x) dipped to 18.6x from 19.0x. In theory, this sector got cheaper in October. Like Financials, EPSg is a modest but positive +3.7% here.

Q: Cheap versus Expensive?

View: Real Estate stocks got cheaper in October, but like many sectors, this one is trading above its long term average P/E Ratio – in this case by around 10%.

Discretionary: investors choose to sell

It was also a poor performance in Consumer Discretionary stocks in October, with the sector logging a 3.8% decline in total return (+0.1% from dividends versus -3.9% from price decline). Negligible EPS change here means the sector PER (x) declined by 3.9% to 23.3x (from 24.2x in September). EPSg is a very healthy 8%, however.

Q: Cheap versus Expensive?

View: It is often the case that above average earnings growth is associated with an above average P/E Ratio. It appears to be the case here, but based upon traditional cheap-vs-expensive pegs, Discretionary is hardly screaming value. FYI, the longer term P/E Ratio for this sector is closer to 19x.

Communications: earnings growth equals share price growth

Along with Financials and Staples, Communications was one of only three sectors to deliver price and earnings growth in October. However, unlike Financials, Communications earnings growth outpaced its price growth, allowing for a modest 0.7% reduction in the sector’s PER (x) to 26.3x from 26.5x in September. Communications sports the third strongest EPSg among the major sectors – its forecast 14.7% EPS growth will likely attract growth investors.

Q: Cheap versus Expensive?

View: Another high earnings growth-high P/E Ratio sector proving beauty is in the eye of the beholder. P/E Ratios in the mid-20’s for Communications have not been unusual since 2020, but if we look longer term, they were mid-teens for much of the last decade.

Technology: high valuation under pressure

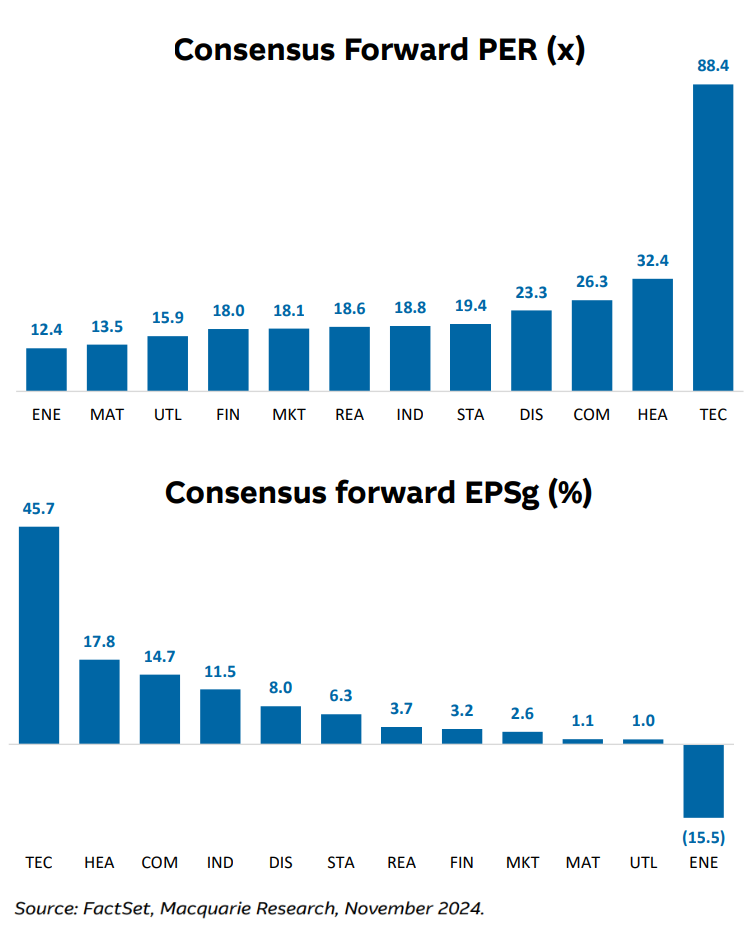

Technology was one of the harder hit sectors in October, with a 4.0% decline in total return. EPS Change was a positive 2.1%, however, allowing the sector’s PER (x) to pare back to 88.4 from 93.7 in September. With a P/E Ratio this high, you’d want to have a very high EPSg to justify it. Perhaps then it's no surprise Technology is sporting a market leading +45.7% in this metric.

,%20Figure%205%20-%20Consensus%20forward%20EPSg%20(bottom)%20Source%20FactSet,%20Macquarie%20Research,%20November%202024..png)

Q: Cheap versus Expensive?

View: Technology is typically a high P/E Ratio sector, reflecting the just-as-typically-rapid earnings growth experienced in the sector since the late-90's. Still, a “high 80s-90s” P/E Ratio is eye-wateringly high even for this sector, but I suggest investors are more likely considering P/E Ratios in 2-3 years here – and not only those in 12 months. 3 years of 45% compound annual earnings growth is going to cut an 88 P/E Ratio to just 15 (coincidence!?🤔). Horses for courses, and investing in Tech stocks is for those who understand the nature of this style of investing.

Health: healthy returns

Health managed a slightly positive total return of 0.7%, backed by a robust 5.8% EPS change. This resulted in the sector’s PER (x) dipping to 32.4x from 33.9x in September. EPSg is a very healthy 17.8%.

Q: Cheap versus Expensive?

View: A commendable performance by Health in October, but its P/E Ratio is still high compared to long-term norms of around the mid-20s.

Staples: hardest hit

Staples was the second hardest hit sector in October as sector leader Woolworths (ASX: WOW) tumbled on fears relating to the recently announced ACCC supermarkets case in the Federal Court and a disappointing first quarter trading update. Prices often track earnings expectations, and it was the case with 1.8% shaved off the sector’s forecast earnings for next 12 months. Still, the imbalance between price and forecast earnings declines helped improve value within the sector – its PER (x) dipped to 19.4x from 20.3x in September. EPSg is a decent 6.3% here.

Q: Cheap versus Expensive?

View: Staples is one of the few sectors trading around its long term P/E Ratio average.

Materials: Materially undervalued?

Materials stocks couldn’t maintain their September resurgence, dipping a modest 4.9% compared to September’s 12.9% gain. Importantly though, and possibly due to an improved outlook in the wake of the Chinese economic stimulus measures, 12 month forecast earnings improved 3.9%. The combination of falling prices and increasing earnings resulted in a notable 5.1% reduction in the sector’s PER (x) to 13.5x from 14.4x in September. EPSg is hardly shooting the lights out at +1.1%, though.

Q: Cheap versus Expensive?

View: Aussie Materials stocks appear to be undervalued compared to many other sectors, and perhaps more importantly, the sector is also undervalued compared to its long term P/E Ratio average of 14x.

Energy: Australia’s cheapest sector?

Energy is the worst performing ASX sector over the last 12 months. October was more of the same, with a -4.8% total return (+0.1% in dividends versus -4.9% price change). Prices and earnings moved in the same direction, with 12 month forecast earnings for the sector sinking by 2.0%. The sector P/E Ratio was 12.4, roughly in line with September. EPSg tells the story here, a dismal -15.5% and the worst of any other major ASX sector.

Q: Cheap versus Expensive?

View: Professional analysts often warn mum and dad investors about the “P/E Ratio Trap”. This is where novice investors gravitate towards low-P/E Ratio sectors that professional investors have forecast to experience large declines in earnings.

Basically, a low-P/E is sometimes a red flag for a weak sector – rather than a sector that’s representing good value. Markets look forward, not backward, so investors must consider valuation within the context of earnings growth. A low-P/E Ratio accompanied by strong forecast earnings growth is more likely to equate to good value compared to a low-P/E Ratio accompanied by earnings contraction.

The last point above says it all – yes there’s a very low P/E Ratio relative to other major sectors here, but what’s going on with earnings has to be concerning. For what it’s worth, at 12.4x, Energy’s P/E Ratio is modestly below its 14.5x long term average

Utilities: down, but not out of contention

The Utilities sector was the hardest hit sector in October, posting a total return of -7.2%. Next 12 months earnings were also clipped by 1.1%, resulting in the sector’s PER (x) dipping 6.1% to 15.9x from 16.8x in September. EPSg is nothing to get excited about at +1.0%.

Q: Cheap versus Expensive?

View: Using the 10-15-20 P/E Ratio rule of thumb, Utilities appear to only be fair value. They are, however, trading at a tidy discount to their longer term average of closer to 20x.

Conclusions

At a very high level, it appears that higher earnings growth sectors like Discretionary, Communications, Technology, and Health are trading at lofty P/E Ratio levels compared to both the 10-15-20 rule and their respective long term averages.

On the other hand, sectors like Materials, Energy, Utilities that are presently sporting lower earnings growth forecasts, appear to be trading at more attractive valuations compared to the 10-15-20 rule, peers, and long term averages.

In between, there’s a group of sectors sporting modestly positive earnings growth including Financials, Real Estate, and Discretionary that are hardly cheap, but also aren’t nearly as expensive as some of their higher-earnings growth peers.

One theme that is consistent throughout this analysis is that investors appear to pay a premium in terms of valuation for stability and growth in earnings. This is therefore, potentially a good rule of thumb to consider when sizing up your next investment.

This article first appeared on Market Index on Monday 4 November 2024.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl has a passion for technical analysis and has taught his unique brand of price-action trend following to thousands of Aussie investors.

........

Investing is risky. Inevitably you will endure losses. If you can't cope with losing, don't invest.

{kind=link}

,%20Figure%205%20-%20Consensus%20forward%20EPSg%20(bottom)%20Source%20FactSet,%20Macquarie%20Research,%20November%202024..png){kind=link}

{kind=link}

5 topics

20 stocks mentioned

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl...

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl...

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

What a 40% year taught us: 4 lessons from the past 12 months (and 3 new stocks to buy)

Seneca Financial Solutions

Equities

Morgans’ top large-cap picks for October 2025

Morgans Financial