Cooking with gas – global energy opportunities

Electricity generation in Europe is undergoing a major transformation. Many investors think that the “new world” (i.e. renewables, batteries and smart grids) is going to wipe out the “old world” (i.e. centralised baseload generated from nuclear and fossil fuels). Whilst we do accept that there will be a transition we are cognisant that there are serious financial, political and practical factors that will keep low cost “old world” assets in demand for the foreseeable future. For the lights to stay on, supply and demand must be actively balanced 24/7, and renewables simply can’t do that yet. Therefore, until affordable storage of TWhs of energy is feasible, electricity will remain a mission critical service, not a commodity.

The workings of electricity markets in Europe are complex and poorly understood, largely due to an interplay of national and European level policies. However, what is abundantly clear is that the German policy of subsidising renewables has been somewhat environmentally unfriendly, knocking clean burning natural gas out of the supply stack in favour of cheaper hard coal (power is dispatched according to short run marginal cost of fuel). As high cost gas plants were removed from their price setting position and increasingly sat idle, vital “peak pricing” gradually disappeared. Depressed gas prices over the past 12 months has further cut into peak price volatility. Thanks to E.U. led market coupling, this power price malaise spread to France and other parts of the continent.

Without the earnings that flow from “peak pricing” both hard coal and gas generators in Germany have failed to recover their all-in costs for a number of years. As a consequence, 15% of hard coal and 23% of gas/oil plants have already declared decommissioning plans. When combined with the forced shutdown of nuclear and lignite plants we estimate that 30% of the total required capacity is set to leave the market by 2023. Whilst renewables will fill some of this gap, gas fired generation will play a much greater role leading to a large pick-up in gas demand as well as a significant increase in power prices. As the U.K. market has recently shown, a properly functioning carbon market would significantly accelerate that shift.

Although not immediately obvious, there are a number of linkages between global gas prices and European electricity prices, with much of the analysis we have done on the North American and global liquefied natural gas (LNG) market helping to inform our views on the European generation market.

The current consensus view is that the wave of new LNG projects from the U.S. and Australia will result in a global oversupply of LNG. Given Europe’s deep spot market liquidity, well connected infrastructure and price sensitive power generation demand, it will become the dumping ground for this “excess” LNG, putting downward pressure on European gas prices and by extension, European electricity prices for a number of years.

We tend to disagree for two major reasons. Firstly, the market is too focused on the supply side of the LNG equation, missing the significant growth in demand from new gas markets such as China. Secondly, we question whether there will actually be sufficient gas production in Australia and the U.S. to meet the future volume commitments of these LNG plants. Whilst talk of gas shortages is now mainstream media in Australia, such an outcome is seen as impossible in North America even though production growth has stagnated in the last 3 years.

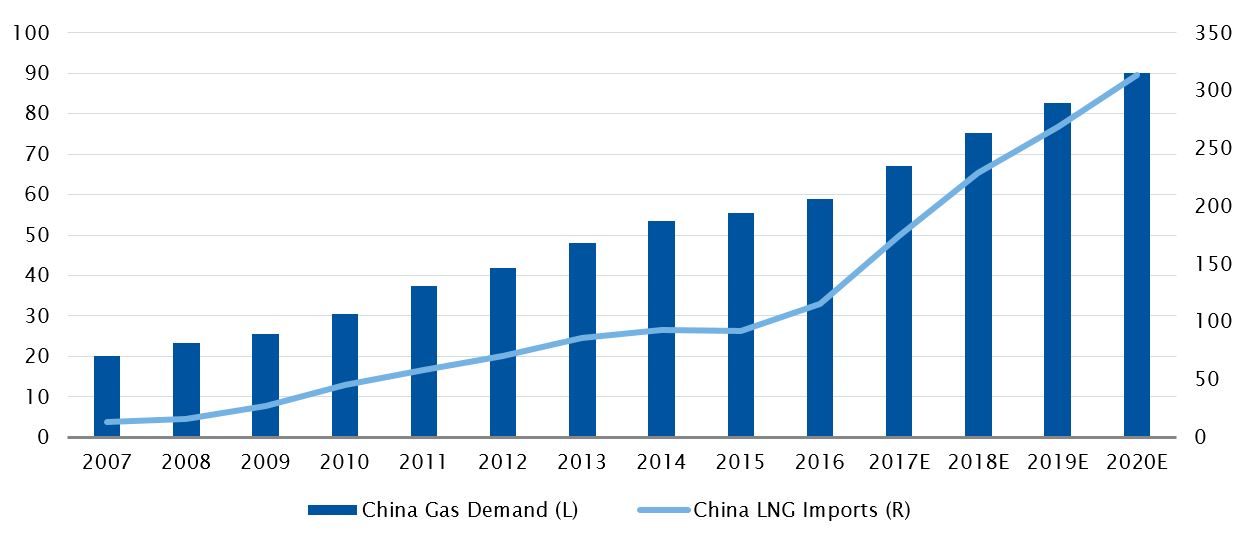

Chinese gas demand and LNG imports (billion cubic metres, 2007 – 2020E)

Source: Source: BP, Antipodes Partners

Over the next three years, annual global LNG capacity is set to increase by around 100 billion cubic metres (bcm). Set against current LNG demand of 350 bcm, this growth in output is considerable. However in the context of global gas consumption of 3,600 bcm it does appear somewhat insignificant, especially when one considers Chinese demand potential.

Over the last 10 years, Chinese gas demand has grown at 13% p.a., with consumption this year set to come in at 235 bcm, up +15% year on year. Despite this growth, gas still accounts for less than 7% of the energy mix, well short of the Government’s 10% target set for 2020 as part of its clean energy policy.

With domestic production growth estimates largely dependent on unproven shale reservoirs, LNG is likely to supply the bulk of this additional demand. So far this is proving to be the case with Chinese LNG imports surging 50% this year. When combined with robust demand from new market such as Pakistan, Jordan and Thailand as well as increased gas fired power generation demand in Europe, we question whether there will be any LNG surplus at all. With LNG spot prices currently trading at premium to long term oil linked contracts, we feel somewhat vindicated in our view.

CORRELATION CLUSTER

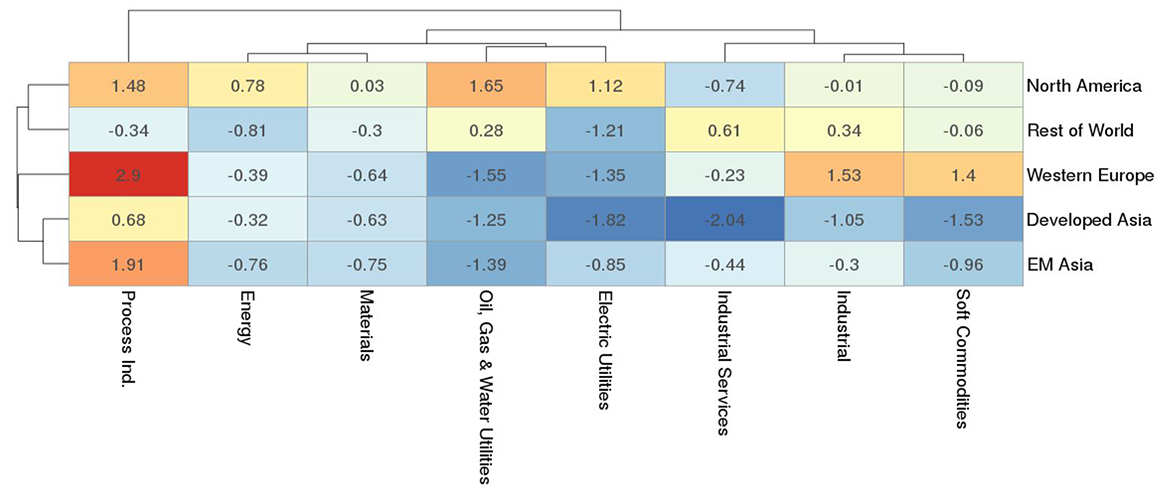

The Antipodes Partners Industrials, Commodities and Utilities Valuation Heat-map provides a more granular illustration of valuation clustering across sectors and regions. Cell colouring indicates the degree to which a sectors’ enterprise value to sales multiple relative to the world is above or below its 21 year trend (expressed as a Z-Score, the number of standard deviations from the mean). The warmer the colour, the greater the relative multiple versus history; vice versa for the cooler blues, with extremes highlighted by the boldest of colours.

Figure 1: Antipodes Partners Industrials, Commodities and Utilities valuation heat-map

Source: Source: Antipodes Partners

Our holdings in EDF and Inpex are well positioned to benefit from this forecast rise in gas and electricity prices and across portfolios we have up to approximately 10% exposure to stocks offering a similar opportunity. Whilst these stocks are correlated, they are also broadly differentiated by activity and regional end-market including resource owners, energy services, European electricity generators and Chinese town gas distributors. Also, as is evident in Figure 1, whilst the global Energy and Electric/Gas Utility sectors appear cheap in most regions of the world, in the current environment of high valuation dispersion, there are also cheap ways to hedge some of the commodity price exposure via shorts. In particular, the North American “shale patch”, where the market is still extrapolating growth with very little focus on returns, still appears significantly over-valued, as do the North American utilities that have been broadly re-rated as bond proxies.

ELECTRICITE DE FRANCE (EDF)

EDF is the owner of the largest nuclear fleet in Europe, supplying 80% of French electricity demand. We think it has been unduly punished by the European regulators and investors alike, who have failed to recognise the systematic importance of this asset.

Irrational Extrapolation

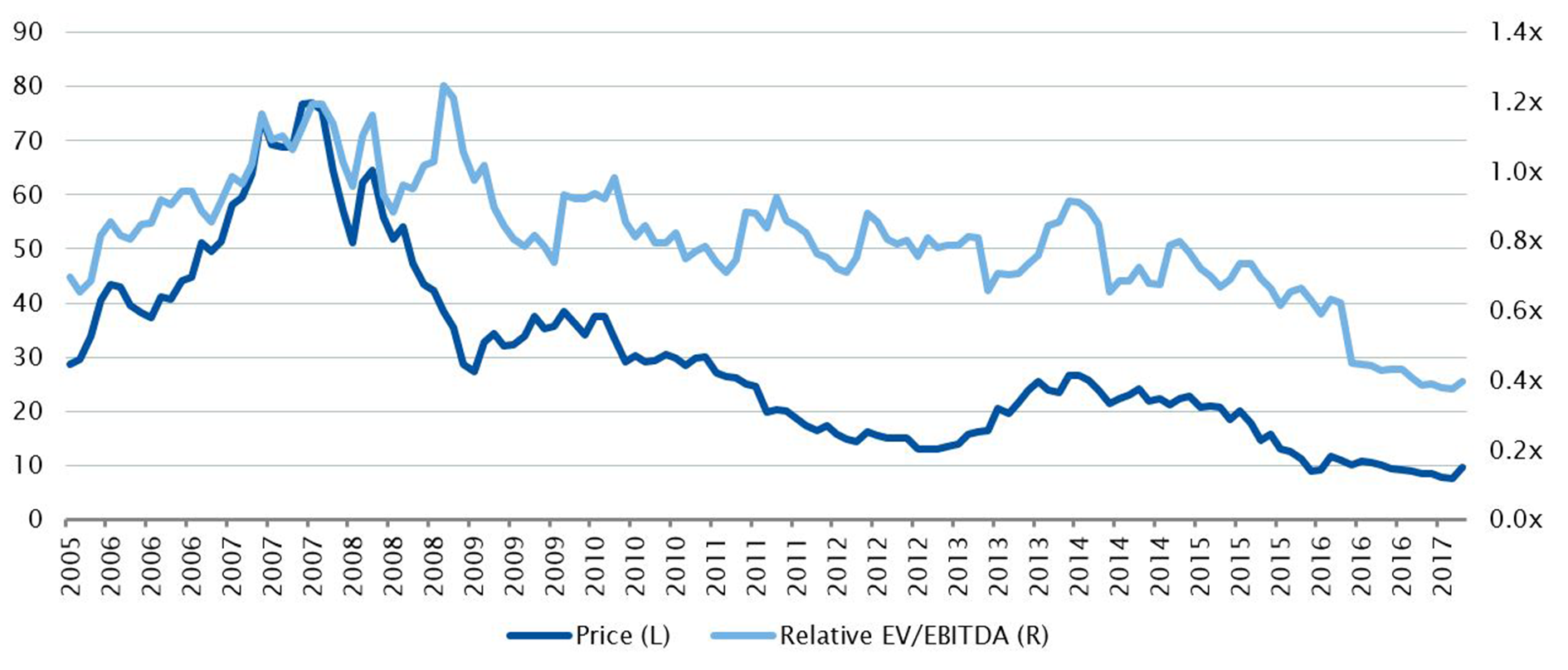

The power price malaise that spread from Germany to France has depressed French prices to levels EDF’s regulators had never envisioned. Investors are extrapolating these conditions into perpetuity, not recognising the inevitable transition to a more sustainable state of affairs.

Chart 2: EDF relative EV/EBITDA to world (2005 – 2017)

Source: Factset

Multiple Ways of Winning

As the largest producer of carbon-free energy in Europe, EDF is system critical not only to France, but to the entire continent. All-in cash cost on EDF’s fleet, even in the middle of a very heavy maintenance cycle, is still cheaper than a comparable cost measure for gas or hard coal (at currently depressed carbon and gas prices).

Energy demand is bound to increase with the economic recovery, at the same time capacity is being withdrawn at a record pace. Electric vehicles (EVs) have potential to further increase energy demand by around 0.7% for every 5% of EV adoption rate.

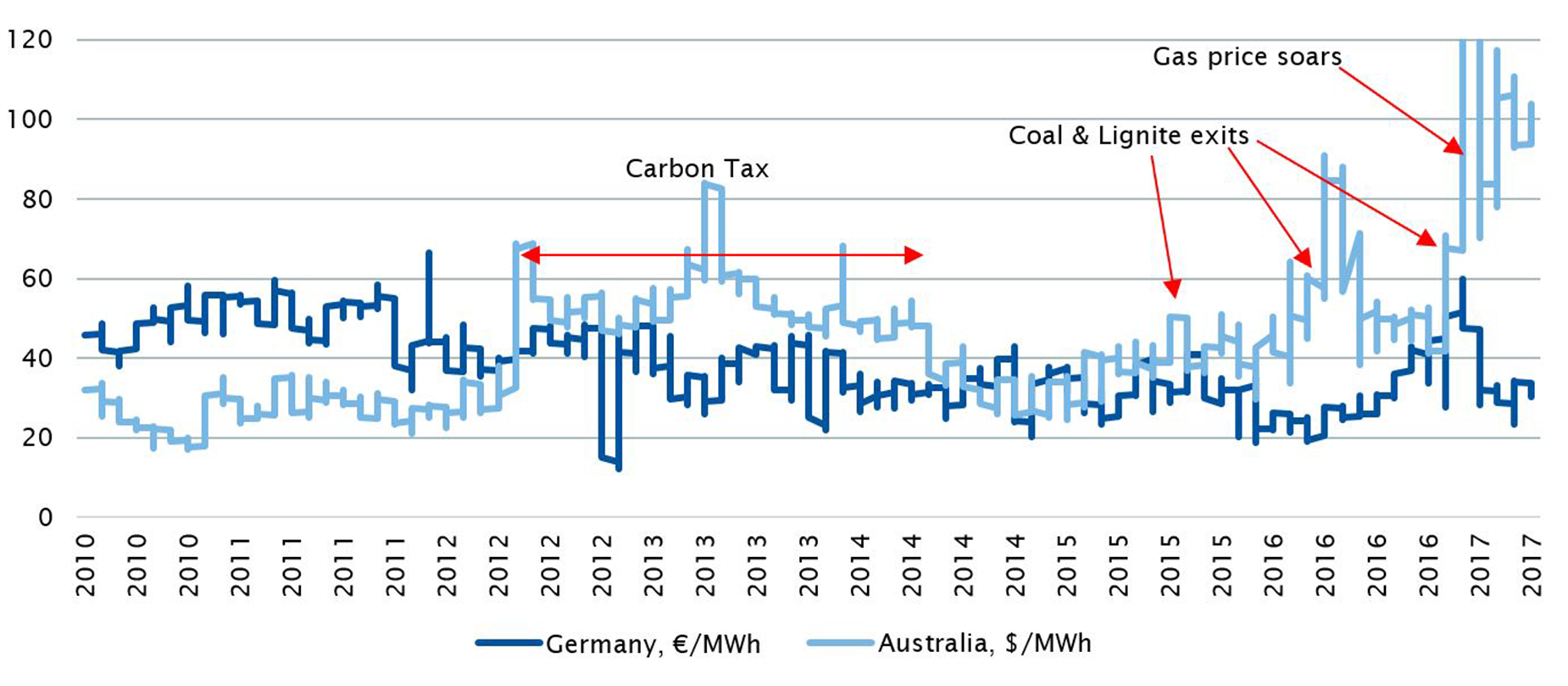

As marginal fuel shifts from coal to gas, Europe may find itself in a “power price” super-cycle similar to Australia (Chart 3). Poor economics and tighter environmental policies will eventually drive hard coal out of the market and gas burn will increase substantially, pushing gas and electricity prices even higher.

Chart 3: Australian electricity price case study (2010 – 2017)

Source: Bloomberg

Margin of Safety

Despite the 40% rally off the lows, the shares trade at a fraction of the replacement cost of the assets, reflecting a long streak of operational, governance and regulatory mishaps. The 63GW strong nuclear fleet – once an earnings powerhouse of the Group – will likely return a cash break-even result this year. We appraise that the market is valuing this at a negative €20bn equity value.

The French government owns 80% of the company and it has already implemented a number of important regulatory initiatives to bolster the earnings of the French fleet. After funding this year’s €3bn equity injection and multiple foregone dividends, the government is highly incentivised to make the company work again. An extra 10 €/MWh in power prices makes a significant difference to EDF’s earnings (+€1.8bn), but only represents +6% on the total French retail power bill and the country enjoys a power bill roughly 50% lower than the broader region.

INPEX

Inpex is effectively Japan’s national oil company and is best known in this country as the operator and 62% owner of the $38bn Ichthys LNG project. Ichthys is effectively three mega-projects rolled into one, involving some of the largest offshore facilities in the industry, a state-of-the-art onshore LNG processing facility and an 890km pipeline all with an operational life of at least 40 years.

Ichthys is set to begin producing by the end of the year and by the time it reaches plateau production in 2019 it will be generating 8.9 million tonnes of LNG, 1.6 million tonnes of LPG and 36 million barrels of condensate per annum.

For Inpex, this will translate into an additional output of 200,000 barrels of oil equivalent per day (boe/d), increasing its production base by almost 50%. Given the relatively low operating costs and favourable tax structure, the impact on the cashflow statement will be much greater. Yet despite this upcoming inflection, on most metrics Inpex still trades as the cheapest oil and gas producer globally; so what is the market missing?

Irrational Extrapolation

Firstly, we believe the market is too focused on what has happened, extrapolating the operational and cost issues that also plagued other Australian LNG developments. Despite having scant tangible evidence to support their claims, the bearish sell-side analysts still forecast significant cost overruns. Whilst we acknowledge that there are residual risks, we take comfort in the fact that the offshore facilities have now been installed and the project is over 90% complete.

Admittedly Ichthys hasn’t been without issue, with the project forecast to come in around 10% over budget and 15 months behind schedule. However in the grand scheme of Australian LNG projects, that actually ranks as somewhat of a success. Yes, the full cycle economics of the project won’t be spectacular but that is largely irrelevant, we are buying the company today when the vast majority of the capital has already been spent and we are now in the position to harvest the cashflow that will be generated.

Secondly, Inpex is also a victim of where it is listed, with most Japanese investors unaccustomed to valuing resource based companies given the lack of local comparisons. Consequently, most tend to value Inpex on shorthand multiples of earnings which fails to capture the asset duration of the portfolio. In addition, by looking at earnings after depreciation we are over-emphasising the cash that has gone in, whilst largely ignoring the significant cash that is set to come out.

Multiple Ways of Winning

Whilst few would argue that the successful ramp-up of Ichthys is crucial to Inpex, we do believe the market is underestimating just how great the cash inflection will be. As stated earlier, the upfront investment of Ichthys has been massive, however the ongoing capex requirements will be no more than $2/boe. Combined with operating cost of $12/boe and minimal tax obligations the project will deliver almost $35/boe of cash flow assuming oil prices of $50. After considering interest and principal repayment, that should result a $2bn uplift in free cash flow for Inpex. When compared to an Enterprise Value of $16.5bn, the significance is stark.

Whilst Ichthys will always dominate the investment debate with Inpex, there is much more to this company than this one project. Indeed the market seems to underestimate just how significant a period of investment the company is now emerging from, with next year also seeing the benefit of the start of the Prelude floating LNG development. This comes on the heel of the successful ramp up of Kashagan with these two projects contributing a further $700m of FCF to Inpex.

Margin of Safety

One way to consider the valuation is simply to look at Enterprise Value to Proven Reserves. On this metric, Inpex trades on an Enterprise Value of $5/boe compared to the average global sector multiple of $11/boe. However, we are mindful that no barrel is created equal, with variations in realisations, operating costs and taxation rendering the metric somewhat flawed.

For a more objective assessment of valuation we can consider the net present value of its proven reserves, which at the current oil price we estimate to be worth $20bn compared with the Enterprise Value of $16.5bn. Bear in mind this is only proven reserves; no credit is given for possible reserves or future exploration success. Effectively we are buying the business today at a significant discount to the run-off value.

As a sense check, by the time Ichthys has fully ramped up in 2019, Inpex will be on an EV FCF yield of 15% assuming oil prices of $50/boe.

For further insights from Antipodes please visit our website

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Antipodes' pragmatic value approach to investing in global equities aims to provide clients a smoother long-term wealth creation journey. We manage global long-only and long-short unit trusts, along with the Antipodes Global Shares (Quoted Managed Fund) active-ETF (ASX: AGX1). Through these vehicles, investors can access portfolios of attractively priced global businesses with strong long-term growth prospects. Antipodes was established in 2015. The investment team operates from offices in Sydney and London.

5 topics

1 stock mentioned

Antipodes' pragmatic value approach to investing in global equities aims to provide clients a smoother long-term wealth creation journey. We manage global long-only and long-short unit trusts, along with the Antipodes Global Shares (Quoted Managed...

Expertise

Antipodes' pragmatic value approach to investing in global equities aims to provide clients a smoother long-term wealth creation journey. We manage global long-only and long-short unit trusts, along with the Antipodes Global Shares (Quoted Managed...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Funds

The 5 best-performing super funds of the year

Livewire Markets

Equities

Buy Hold Sell: 5 ASX stayers built to go the distance

Livewire Markets