Time to buy... or time to sell?

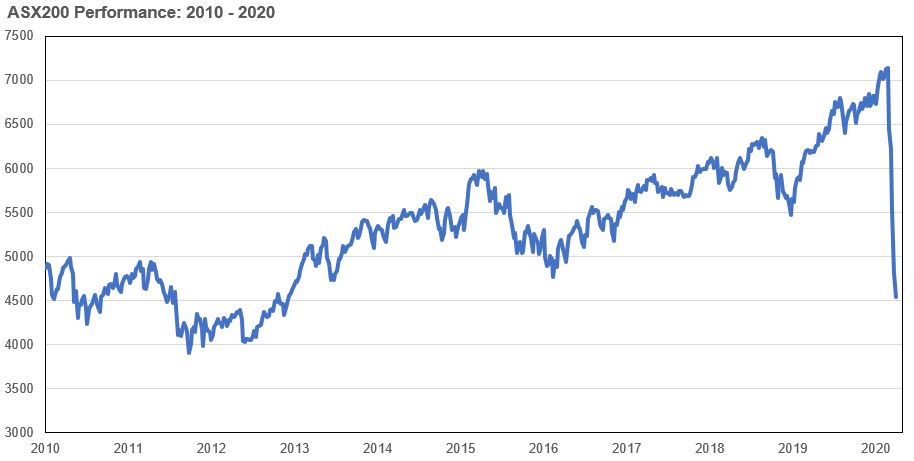

Fear and panic have gripped markets. In the four weeks since the 21st of February the ASX200 has declined from 7197 to a low of 4402 on the 23rd of March. And there is no telling whether and by how much it might continue to fall. The 38.8% decline has been extraordinary in its ferocity and speed, only surpassed in modern Australian stockmarket history by the 1987 crash.

The magnitude of the moves at the stock levels are even more dramatic. The resilience of some big index weights, including Woolworths, Coles and CSL, masks the destruction in valuations elsewhere in the index. Many stocks are down well over 50% in just four weeks. There has been very little time to modify investment exposures to respond to new information.

The positive outlook for the domestic economy, highlighted by the better than expected fourth quarter 2019 GDP data released on the 4th of March, has been made irrelevant by the probability that growth will be significantly negative in the coming months as countries shut down to reduce the loss of life stemming from the coronavirus COVID-19 (Coronavirus). So the question from here is what to do now? Is it a time to be selling or buying?

In relation to whether now is the time to sell, the critical factor is whether the value of the companies that an investor owns has changed in the last four weeks by the degree to which the share prices have moved. At a high level, the economic impact of the coronavirus on most companies will last the duration of the period in which it is not under control. During this period the hit to GDP, company revenues and earnings will be potentially enormous.

We do not wish to add to the sensationalism of every current headline, but clearly the travel, tourism, services, education, media, consumer discretionary and banking sectors are likely to be heavily impacted. In this regard the government is taking a proactive approach. If income is lost due to policies aimed at implementing social distancing and, for those potentially or actually infected, self-isolation, then the government needs to provide these individuals and small businesses with cash to be able to carry on through this period. This is exactly what the Australian federal and state governments are undertaking to do.

Similarly, there is likely to be a rise in unemployment, potentially substantial. However, these jobs are unlikely to be lost forever. It could be reasonably expected that the same number of waiters, hairdressers, event planners and tour guides will be needed post Coronavirus. There may be a sharp “recession”, but it seems likely that there will be a significant rebound in activity thereafter, absent the crisis cascading into something else altogether.

With more of the world’s medical resources devoted to working on both a vaccine and antiviral medication for the Coronavirus than, we suspect, any other virus in history, we believe it is right to be optimistic about the likelihood of medical success over the next 6 to 12 months. Australia is also acting quickly to try to stem the spread of the disease. Testing is an important part of this process, to let infected people know they are infected so that they can self-isolate to reduce the risk of infecting others. Testing rates per capita in Australia are among the highest in the world.

So how do we think about the valuation of companies to incorporate the impact from the Coronavirus? The businesses we own are conservatively geared, generally best of breed operators that are well placed to weather a difficult period. Each business will be impacted in different ways, and it is important that we assess this. Almost every company will experience a decline in earnings in the near term. Generally the market responds aggressively to earnings downgrades because the current year’s earnings are typically the most reliable baseline for assessing future years’ earnings. So typically a 30% earnings deterioration this year might justify a 30% deterioration in the valuation of the company, as analysts reassess and lower expectations for all future years of earnings.

However, it is most likely that the Coronavirus will not have an ongoing effect. The impact is more likely to be a genuine one-off occurrence. Even if all of the businesses we own collectively make no money for the next 6 months, some will even lose money, the earnings thereafter should return to a level similar to what they were prior to the Coronavirus. (In fact for many, pent up demand could result in a short spike above previous levels post resolution of the crisis.) Put another way, owning stocks now is akin to owning them in 6 or 12 months time, or however long a resolution takes, when earnings will be back to normal at extremely attractive valuations while accepting that there might not have been any earnings to speak of in the interim, and there may even be some one off costs or losses to factor in.

This said, the market may continue to fall. However, most people that sell now assume they will know when to get back in. This is virtually impossible. There is no bell that chimes when the stockmarket low has been set. The pain may continue for some time, but as previous dislocations have demonstrated, often the market starts to climb the wall of worry while the news is still bad. By the time the recovery comes stocks have often rebounded considerably.

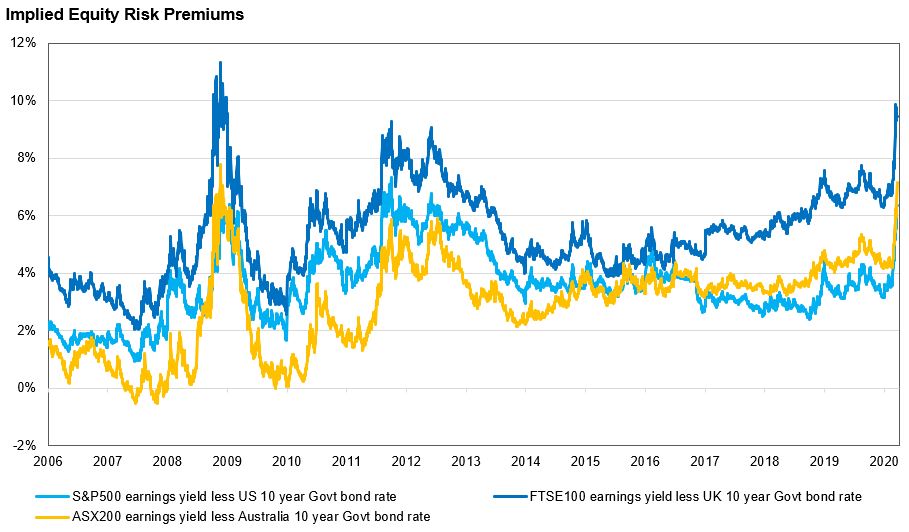

So when is the time to buy? This is a difficult question to answer. Implied equity risk premiums are extremely wide, as shown below. However, as a frame of reference, they are not yet at the same level as the peak of the Global Financial Crisis.

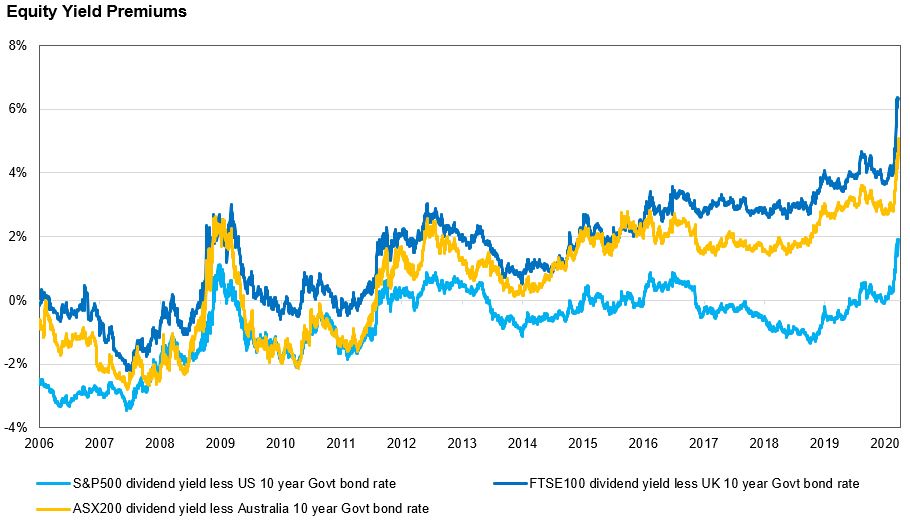

Equity yield premiums, or the additional yield you are likely to receive for holding shares over Australian Government bonds, have never been higher.

While there is undoubtedly risk to near term dividends, lost dividends should be reinstated in most instances post the resolution of Coronavirus concerns. Again, analysing each company and assessing the risk to dividends is important. Interestingly, we closely follow buying and selling activity from those inside the company. Directors and management know far more about the businesses than an external investor will ever know. So they are in a more informed position to make a decision about the long term prospects of the business. During difficult periods, they are best placed to understand whether the company can weather the storm. If they are committing their own after-tax income to buy shares, it is normally a good indicator that there is value on offer. In the last 4 weeks we have had insider buying, typically from directors, in 13 of the 27 companies the Auscap Long Short Australian Equities Fund is presently invested in. This is the highest ratio we have ever seen in a short period of time.

What if you were already caught long, as we were, and do not therefore want to add to your overall exposure? At this stage portfolio optimisation appears to be the best approach to preparing for an eventual recovery in asset prices. Portfolio optimisation might involve selling some assets, even if they have fallen, to buy other assets at even more attractive prices. So far the virus has had quite a different effect on valuation depending on the company, throwing up opportunities. This is the time to improve the quality of and prospective returns from a portfolio. Reducing an investment, even in a stock that is undoubtedly cheap, to buy part of a better business at a more compelling price, is a logical exercise at this point and one we are endeavouring to undertake. The declines in many instances have been indiscriminate, but the recovery will not be. The best companies will outperform in the aftermath of a crisis.

We are experiencing the same raw emotion that all investors are currently going through. The market has been caught in a wave of fear about the unknown. Relentless selling has, temporarily, rendered normal fundamental valuation redundant. However, our role is to remain rational. Portfolio optimisation is a path to improving the quality of the portfolio before the eventual recovery. Until then stock market moves will most likely remain extreme, testing the resolve of every investor, both retail and professional. We encourage all investors to think long term about the companies and funds they are invested in. It is highly unlikely that the “value” of the businesses they part-own has changed to anywhere near the same degree as the recent price fluctuations as a result of the outbreak of the Coronavirus would suggest.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Tim founded Auscap Asset Management in 2012. He has 19 years’ experience in the financial services industry. From 2007 to 2011 he was an Executive Director at Goldman Sachs where he was responsible for managing an Australian equities long/short portfolio using Proprietary funds. Prior to 2007 he worked at Macquarie Bank within the Investment Banking Group. Tim is a CFA charterholder, a CMT charterholder, a Senior Associate of FINSIA, a Graduate of the Australian Institute of Company Directors (GAICD) and has a Bachelor of Laws (Hons) from the University of Sydney and a Bachelor of Commerce from the University of Sydney.

........

Tim Carleton is a Principal and Portfolio Manager at Auscap Asset Management (Auscap), a boutique equities long/short investment manager. This article contains information that is general in nature and does not constitute investment or any other form of advice. This article does not take into account the objectives, financial situation or needs of any particular person nor does it constitute a recommendation to be relied upon when making an investment or any other decision. You need to consider your financial needs before making any decision based on the information in this article and a person should obtain and consider the relevant disclosure document before deciding whether to invest in an Auscap fund. No part of this article is to be reproduced or disclosed without the prior written consent of Auscap. In relation to any MSCI data in this article, the MSCI data is comprised of a custom index calculated by MSCI for, and as requested by, Auscap. The MSCI information may only be used for your internal use, may not be reproduced or redisseminated in any form and may not be used as a basis for or component of any financial instruments or products or indices. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties (including, without limitation, any warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages. (www.msci.com)

3 stocks mentioned

Tim founded Auscap Asset Management in 2012. He has 19 years’ experience in the financial services industry. From 2007 to 2011 he was an Executive Director at Goldman Sachs where he was responsible for managing an Australian equities long/short...

Expertise

Tim founded Auscap Asset Management in 2012. He has 19 years’ experience in the financial services industry. From 2007 to 2011 he was an Executive Director at Goldman Sachs where he was responsible for managing an Australian equities long/short...

Expertise

Comments

Comments

Sign In or Join Free to comment