CSL and no growth but at any price

Our portfolios have been underweight the market's favourites over the last few years and recent 12 months in particular. These can be summarized as bond proxies, growth stocks, and gold. All have been beneficiaries of ultra low-interest rates and the more intense than ever focus on earnings certainty and incremental upgrades. As an aside, not only have very low-interest rates encouraged asset bubbles including the categories above, they have also funded unsustainable (and irrational in the longer term) entrants into industries ranging from energy to insurance. This is another harmful consequence of this interest policy. That is the destruction of industry returns by speculative participants, which will impact the ability to invest in capital and labour.

UBS Asset Management

UBS Asset Management

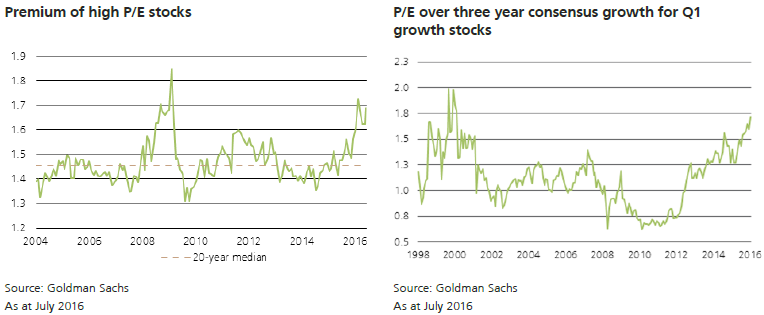

This valuation ignorant obsession with earnings growth has pushed multiples to all-time highs. Investors who have picked the willingness of the market to pay much more for less earnings may argue lower discount rates have encouraged this re-rating. However, the increase in the premium of high P/E stocks over low P/E peers to near GFC levels of 70%, shows this has only been applied to a select section of the market. The same participants may suggest this premium is supported by their delivery of scare growth. However when the P/E of top quartile growth stocks is divided by consensus three-year growth forecasts, the ratio of 1.8 times is almost 30% higher than the same ratio before the GFC, and almost as high as the tech boom.

At the stock level, CSL is a prime example of this willingness to pay massive premiums for traditional growth stocks, whether they deliver the growth or not. At the full-year result this week, CSL achieved their guidance of about $1,470m and just 5% growth by excluding the losses from their flu business. This number also includes a foreign exchange gain of about $115m. The normalized number is over 25% lower than where expectations were one year ago. This performance is clearly not the kind of quality growth expected from a company trading on over 30 times. The company then guided to 11% growth for 2017. However, the starting point for this growth includes the flu loss and excludes the foreign exchange gains for a base of just $1,152m and a 2017 earnings target of $1,278m. Therefore to report a number showing some growth, various one-offs were included, but to ensure growth for the following year these same one-offs were removed from the base. That is the company is asking the market to accept $1,470m as the measure of the performance in 2016, and $1,278m (-13% lower) as the target in 2017, and arguing this still represents growth. In fact, earnings have grown by less than 2% p.a. since 2010. It would be understandable for the market to have hammered the stock over this period. Instead, CSL has been consistently re-rated from an average in the high teens before 2013 to about 30 times now. CSL is one example of many of this trend.

The willingness of the market to ignore valuation risk for stocks traditionally believed to deliver earnings certainty (even if they actually don't), highlights a massive market dislocation. The funding for these trades appears to be the disproportionate and indiscriminate selling of businesses that display any earnings volatility, particularly relative to historically unreliable sell-side expectations. We will explore this in future weeks.

Article written by Jakov Maleš, Head of Equities at UBS Australia, and contributed by UBS Australia: (VIEW LINK)

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

UBS Asset Management offers investment capabilities and investment styles across all major traditional and alternative asset classes. These include equity, fixed income, currency, hedge fund, real estate, infrastructure and private equity investment capabilities that can also be combined into multi-asset strategies.

2 topics

1 stock mentioned

UBS Asset Management

UBS Asset Management

UBS Asset Management offers investment capabilities and investment styles across all major traditional and alternative asset classes. These include equity, fixed income, currency, hedge fund, real estate, infrastructure and private equity...

Expertise

No areas of expertise

UBS Asset Management

UBS Asset Management

UBS Asset Management offers investment capabilities and investment styles across all major traditional and alternative asset classes. These include equity, fixed income, currency, hedge fund, real estate, infrastructure and private equity...

Expertise

No areas of expertise

Comments

Comments

Sign In or Join Free to comment