Deglobalisation and decoupling are upon us with consequences for portfolio construction...

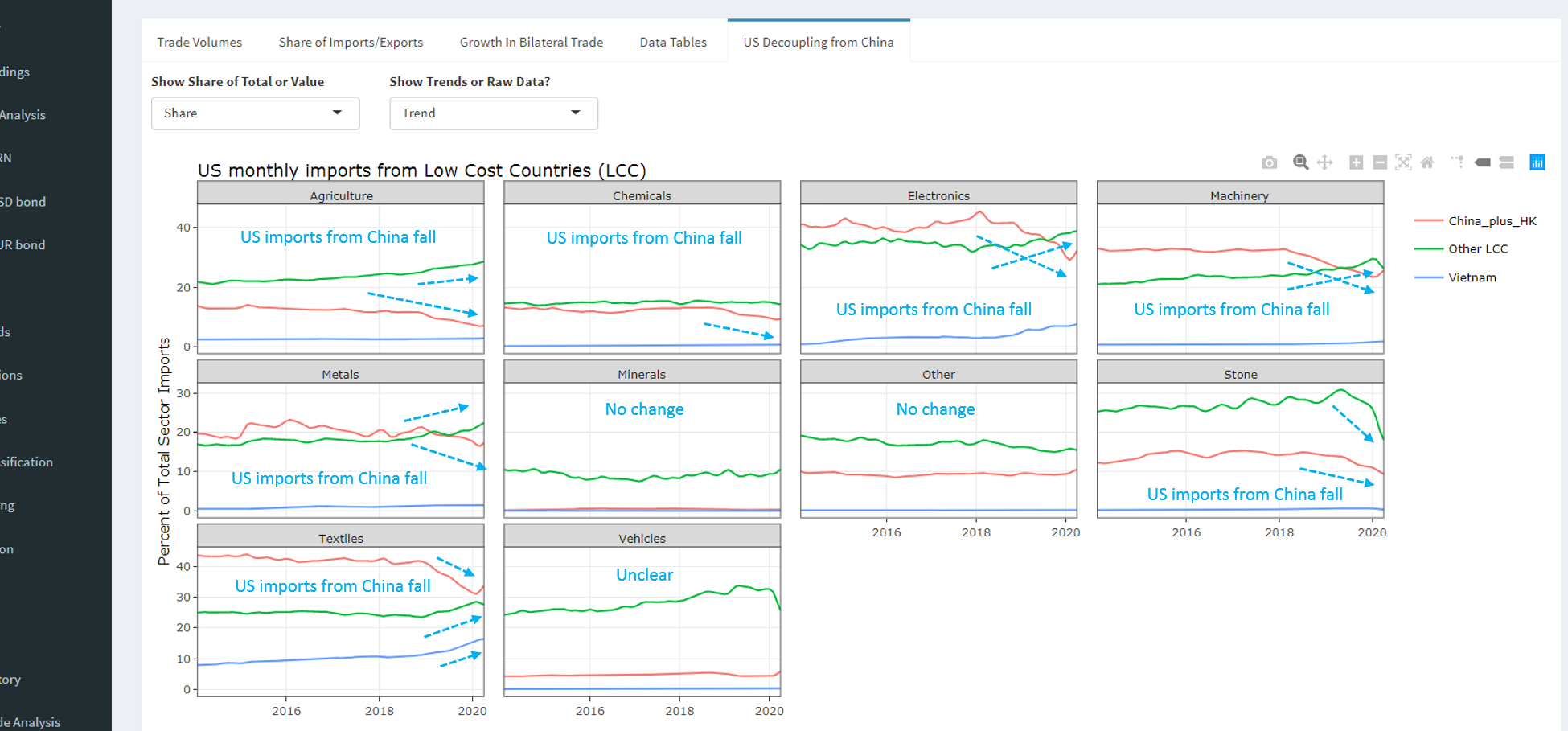

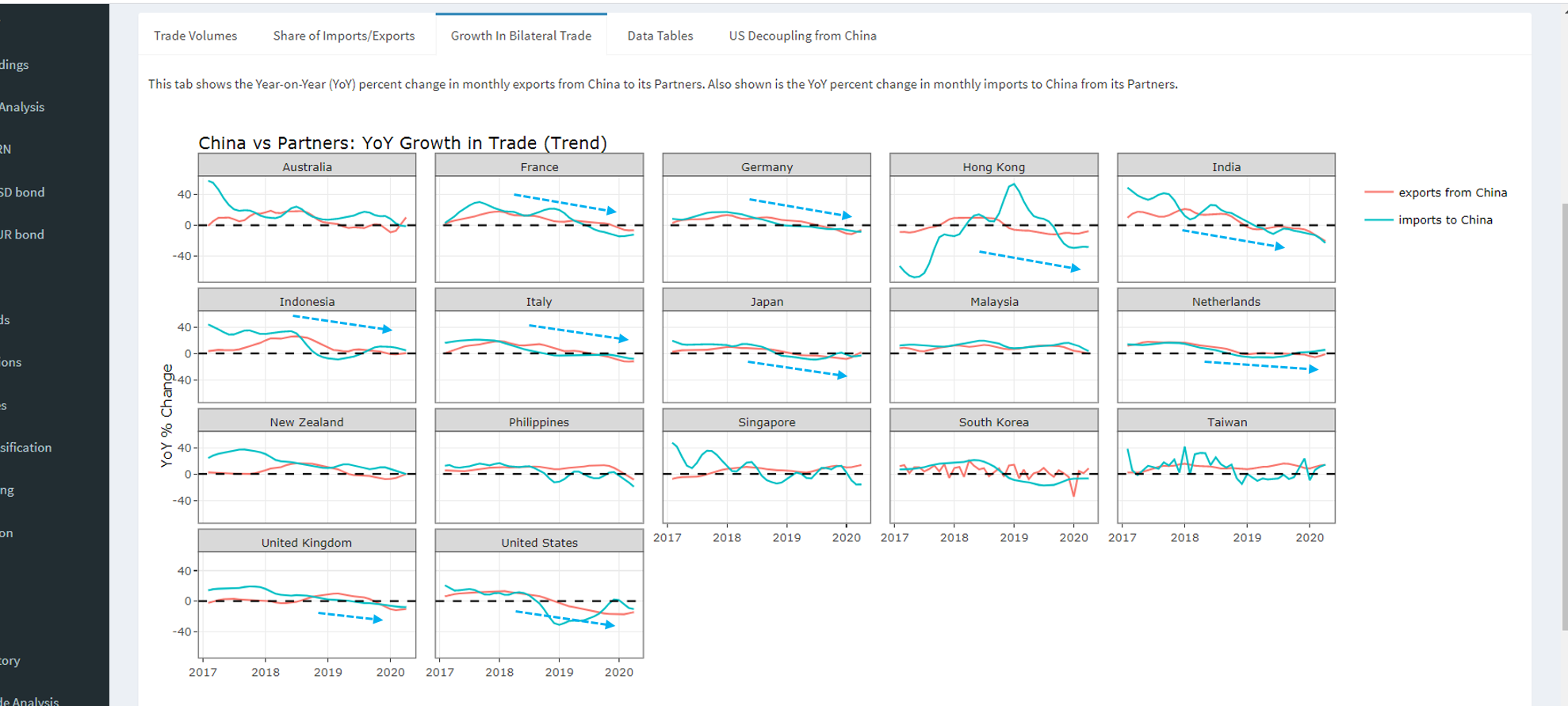

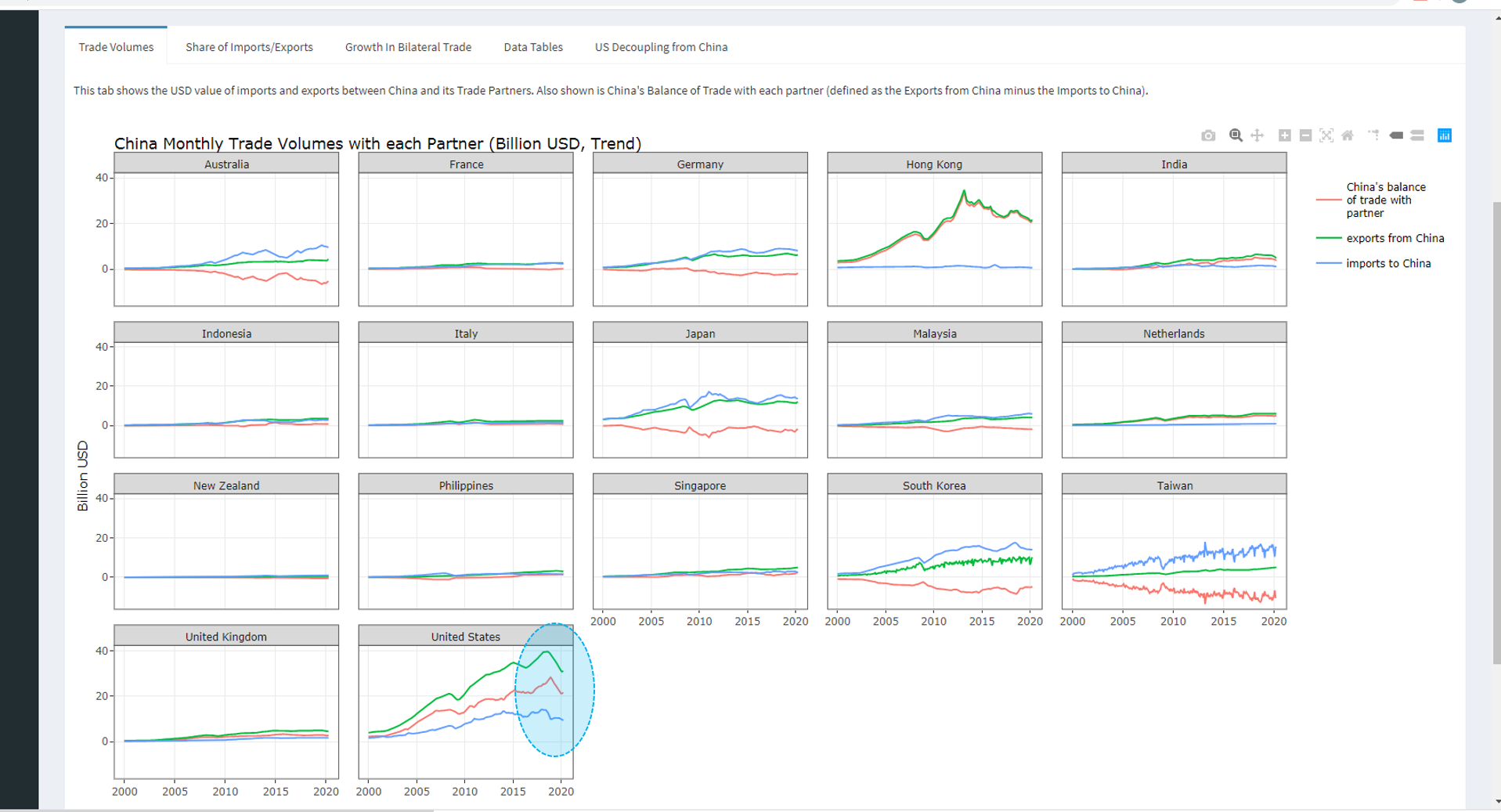

One of the things our team is very focussed on right now is relations between China and the West, and what this portends about the future. There is little doubt that we stand astride a historical inflexion point in geo-political relations that needs to be carefully parsed if one is to make thoughtful assessments about the distribution of future states of nature. In the same way that our quants built real-time COVID-19 infection/fatality tracking and forecasting systems, some time ago I asked them to construct tracking systems for trade linkages between China and the rest of the world to enable us to monitor decoupling in real-time. In this context, there are a few core hypotheses that we are exploring:

- First, we expect to see outright decoupling between the US and China precipitated by the US desire to disconnect given the growing conviction regarding the indivisibility between security, prosperity and liberty. This should motivate a shift in US trade towards other low cost markets (eg, Vietnam, Cambodia, India etc), more proximate regions (eg, Canada and Mexico), and, perhaps most interestingly, internally as the US fosters investment in domestic supply chains, which is a really big deal.

- Second, we think that this domestication of supply-chains in the US will be further fuelled by automation, artificial intelligence and robotics, which will reduce the importance of labour input costs and hence the legacy competitive supply-chain advantage of developing countries with relatively low per capita incomes.

- Third, we believe that this decoupling will extend way beyond the US to most Western states, which is a process that has been catalysed by COVID-19. Striking recent examples of this shift include Japan paying its companies to bring supply chains home and the sudden decision of the UK and Canada to re-evaluate their relationship with certain Asian telecommunications companies vis-a-vis 5G infrastructure.

- Fourth, it is reasonable to assume that China will respond by trying to both actively resist the decoupling dynamic through various legitimate means while at the same time expanding her trade linkages with other developing markets involved in Xi's signature Belt & Road Initiative, including Eastern Europe, Asia, and Africa.

- Fifth, we fear that this could result in a fracturing of much of the global trading system as we understand it today into a bi-polar world cleaved by the Western and Sino ideological and business models, much as we observed during the last Cold War between the world's leading democratic and communist states; and

- Finally, we posit that deglobalisation and decoupling will not be limited to just national security sensitive industries as is currently assumed, but will gradually over a period of years extend to encompass any economically important sector.

While our research is still very embryonic, I am happy to share screen-shots from some of our systems below that show that this process of deglobalisation and decoupling is underway, especially if one focuses on trade between the world's two largest economies. In the medium-term, this will have profound consequences for portfolio construction that all investors should try to understand. That is certainly our mission right now...

Get investment ideas from industry insiders

Liked this wire? Hit the follow button below to get notified every time I post a wire. Not a Livewire Member? Sign up for free today to get inside access to investment ideas and strategies from Australia’s leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha Managers” based on his risk-adjusted performance throughout his career across. He previously worked for Goldman Sachs in London and Sydney, the Reserve Bank of Australia, and founded the award‐winning research/investment group, Rismark. He has regularly advised governments, developing unique policy proposals. Chris graduated with the University Medal (Economics & Finance) from Sydney University. He studied in the PhD program at Cambridge University in 2002/03, leaving to set up his funds business.

........

General Disclaimer:

Past performance does not assure future returns. All investments carry risks, including that the value of investments may vary, future returns may differ from past returns, and that your capital is not guaranteed. This information has been prepared by Coolabah Capital Investments Pty Ltd (ACN 153 327 872). It is general information only and is not intended to provide you with financial advice. You should not rely on any information herein in making any investment decisions. To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this information. The Product Disclosure Statement (PDS) for the funds should be considered before deciding whether to acquire or hold units in it. A PDS for these products can be obtained by visiting www.coolabahcapital.com. Neither Coolabah Capital Investments Pty Ltd, EQT Responsible Entity Services Ltd (ACN 101 103 011), Equity Trustees Ltd (ACN 004 031 298) nor their respective shareholders, directors and associated businesses assume any liability to investors in connection with any investment in the funds, or guarantees the performance of any obligations to investors, the performance of the funds or any particular rate of return. The repayment of capital is not guaranteed. Investments in the funds are not deposits or liabilities of any of the above-mentioned parties, nor of any Authorised Deposit-taking Institution. The funds are subject to investment risks, which could include delays in repayment and/or loss of income and capital invested. Past performance is not an indicator of nor assures any future returns or risks. Coolabah Capital Institutional Investments Pty Ltd holds Australian Financial Services Licence No. 482238 and is an authorised representative #001277030 of EQT Responsible Entity Services Ltd that holds Australian Financial Services Licence No. 223271. Equity Trustees Ltd that holds Australian Financial Services Licence No. 240975.

Forward-Looking Disclaimer:

This information may contain some forward-looking statements. These statements are not guarantees of future performance and undue reliance should not be placed on them. Such forward-looking statements necessarily involve known and unknown risks and uncertainties, which may cause actual performance and financial results in future periods to differ materially from any projections of future performance or result expressed or implied by such forward-looking statements. Coolabah Capital Investments Pty Ltd undertakes no obligation to update forward-looking statements if circumstances or management’s estimates or opinions should change except as required by applicable securities laws. The reader is cautioned not to rely on forward-looking statements.

2 topics

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha...

Expertise

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management