Demand for property to continue to outstrip supply

The CoreLogic Home Value Index report and the National Housing Finance and Investment Corporation’s (NHFIC), State of the Nation’s Housing report both suggest that demand for housing is likely to continue to outstrip supply.

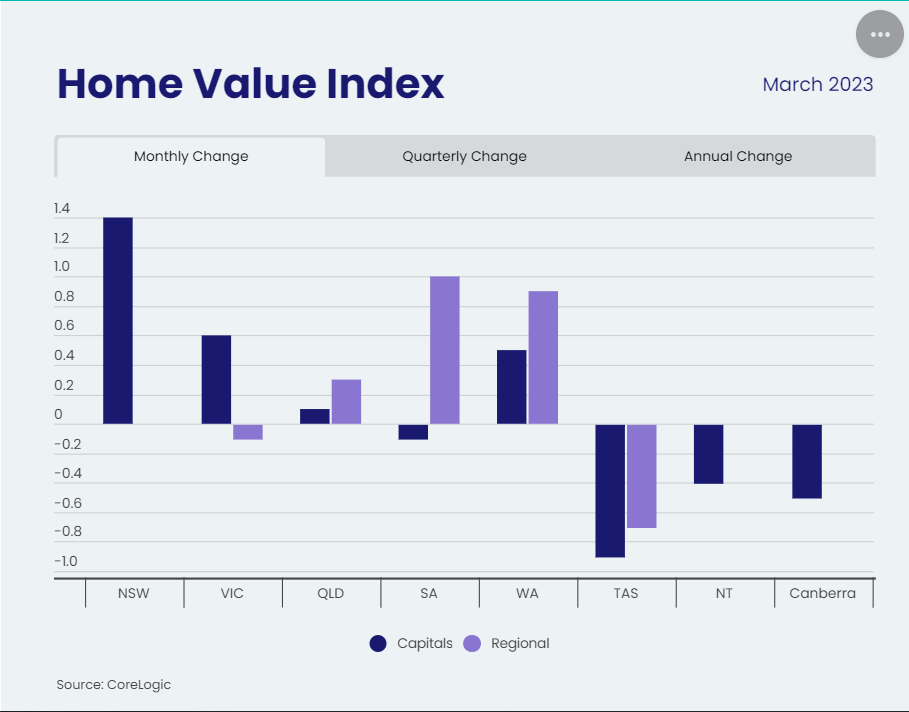

According to the CoreLogic report, dwelling values have seen their first month-on-month rise of 0.6% in March, the first time since April 2022. Suggesting the market is starting to recover from the impacts of the COVID-19 pandemic, and that demand for housing remains robust.

The report shows that Sydney and Melbourne experienced the strongest price growth in capital cities in the past month, with dwelling values rising by 1.4% and 0.6%, respectively. However, this lift is not consistent across the capital cities, with Hobart, Canberra, Darwin and Adelaide, all recording a decline.

Never miss an update

Get the latest insights from me in your inbox when they’re published.

Advertisement

Image source: (VIEW LINK)

Mirroring these findings, the NHFIC report shows demand for housing continues to be strong, particularly in major capital cities such as Sydney and Melbourne where housing supply has struggled to keep pace with demand.

The NHFIC report highlights that demand for housing has been driven by a range of factors including population growth, low-interest rates, and government policies such as the First Home Loan Deposit Scheme.

The reopening of borders has led to a stronger than anticipated recovery, with the Centre for Population predicting net overseas migration will increase by 268,000 between 2022 and 2024 and could be considerably higher. As more people move into cities and other urban areas, the demand for housing is likely to rise. This will place continued pressure on the supply pipeline of affordable housing and in turn, lead to increased competition and property prices.

As seen in both reports, Australia’s housing demand is strong; however supply is undoubtedly struggling to keep pace. In 2022, the construction industry felt the brunt of supply chain issues, with approximately 28,000 dwellings delayed. The industry continues to recover from the severe weather events of recent years and continues to feel the impacts of labour and material shortages. It comes as no surprise that the NHFIC report estimated a shortfall of more than 100,000 dwellings over the next 5 years, to 2027.

These structural characteristics of the Australian property market have far reaching implications. For those saving to enter the market currently, it will certainly be more challenging than any time in recent memory. For investors, the outlook is more positive, with supportive tailwinds on potential price appreciation for prospective property owners; and for those investors in the debt stack of these property transactions, the risk-adjusted return on offer can appear equally, if not more, compelling.

https://www.nhfic.gov.au/media/nhfic-releases-flagship-state-nations-housing-2022-23-research-report

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

As co-founder and Managing Director of Trilogy, Philip is responsible for leading a cohesive and high-performing team across Trilogy’s three offices, overseeing business compliance, and developing product offerings. He sits on the Compliance, Property Investment, Lending and Treasury Committees. He also acts as General Counsel for Trilogy.

Philip has over 30 years of experience in the financial services industry, across financial planning and funds management. He was previously a partner in a Brisbane law firm, having been a solicitor admitted to the Supreme Court of Queensland and High Court of Australia for over 35 years. He is a Fellow of Finsia, with qualifications at a post graduate level in mortgage lending and financial services.

Philip leveraged his Legal and Financial Services qualifications as a founding director in 1998 of the funds management entity which evolved into Trilogy. He is a key instigator of Trilogy’s products, including the Trilogy Monthly Income Trust, as well as the Trilogy Enhanced Income Fund, the Wholesale Income Fund and various property trusts. Philip is passionate about creating financial products within the mortgage and property sectors that generate attractive income returns, as well as assisting younger generations to achieve their financial goals.

........

This article is issued by Trilogy Funds Management Limited ABN 59 080 383 679 AFSL 261425 (Trilogy Funds) as responsible entity for the management investment schemes mentioned in this article. Application for investment can only be made on the application form accompanying the relevant Product Disclosure Statement (PDS) and by considering the Target Market Determination (TMD) available at www.trilogyfunds.com.au. The PDS contain full details of the terms and conditions of investment and should be read in full, particularly the risk section prior to lodging any application or making a further investment, together with the TMD. All investments, including those with Trilogy Funds, involve risk which can lead to no or lower than expected returns, or a loss of part or all of your capital. Trilogy Funds is licensed to provide only general financial product advice about its products and therefore recommends you seek personal advice on the suitability of this investment to your objectives, financial situation and needs from a licensed financial adviser. Investments with Trilogy are not bank deposits and are not government guaranteed. Past performance is not a reliable indicator of future performance.

1 topic

As co-founder and Managing Director of Trilogy, Philip is responsible for leading a cohesive and high-performing team across Trilogy’s three offices, overseeing business compliance, and developing product offerings. He sits on the Compliance,...

Expertise

As co-founder and Managing Director of Trilogy, Philip is responsible for leading a cohesive and high-performing team across Trilogy’s three offices, overseeing business compliance, and developing product offerings. He sits on the Compliance,...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Investing for the biggest market shift since the GFC

Livewire Markets

Equities

Why ex-20 is the prime hunting ground for ASX returns

Livewire Markets