TOL - 19th Jan, 2021

Dodging the darlings and loving the lonely

Our lack of exposure to the high-growth technology sector and the stable earnings streams from the healthcare and consumer staples sectors may seem extreme. But so are the prices one pays for companies in those sectors today.

Consider a hypothetical market darling, whose growth runway extends many years into the future due to its highly sought-after product or service and significant barriers to competition.

Even if it's clearly attractive, there is a price that is simply too high and exceeds the value of the likely trajectory of future earnings. No company is worth an infinite amount.

At the other end of the spectrum is a cyclical company with a bleak growth outlook. But a bleak outlook does not necessarily mean the company’s shares are worth zero. Navigating the grey area between these extremes requires a focus on underlying fundamentals.

Knowing when a market darling’s price is too high is no less important than knowing when an underperforming company’s share price is low enough.

Avoiding the former and building a portfolio of the latter will generate outsized investment returns in the long term, but it’s not easy to do consistently.

We have recently accumulated a stake in South32 Limited, an out-of-favour company that we think is attractively priced. At the other end of the spectrum, an expensive market darling we don’t own, is Afterpay. Sudhir Kissun discusses South32 below, followed by my analysis of Afterpay.

About South32 Limited

In 2015, BHP demerged a diverse portfolio of assets that it considered non-core, creating a new separately listed entity named South32 Limited. The main commodity exposures and assets of South32 are as follows:

- Alumina and aluminium: The Boddington bauxite mine and Worsley alumina refinery in Western Australia, the MRN bauxite mine and Alumar alumina refinery in Brazil, and two aluminium smelters in South Africa and Mozambique that source their alumina requirements from South32’s alumina refineries.

-

Manganese: The GEMCO manganese mine in the Northern Territory, two manganese mines in South Africa, and a manganese alloy smelter in South Africa.

-

Coal: Metallurgical coal mines at Illawarra in New South Wales, and thermal coal mines in South Africa (the South African operation is in the process of being divested).

-

Nickel: The Cerro Matoso nickel mine in Colombia.

-

Silver, lead and zinc: The Cannington mine in Queensland.

-

Other: An investment in the Hermosa zinc, lead, silver and manganese asset in Arizona in the USA, which is currently in the development phase, and various other exploration and development ventures.

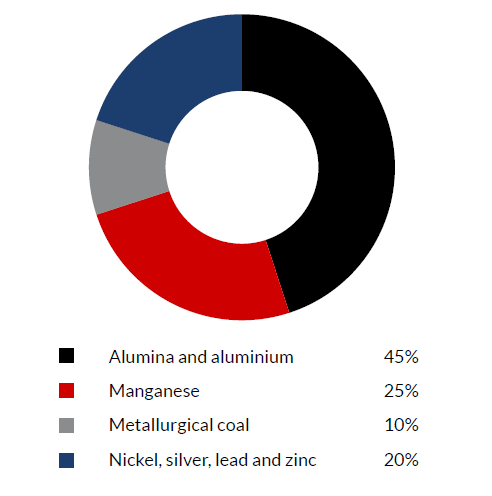

The earnings contributions of each of these assets will vary from year to year depending mainly on commodity price movements, but also on production volumes, operating costs and expenditures on sustaining capital. Through the cycle, we estimate the contributions to earnings before interest and taxes (EBIT) to be as per Graph 1.

Graph 1 - Estimated contributions to EBIT by commodity group

Source: Company financials, Allan Gray.

It is important to point out that the reserve lives of the individual assets differ. The Boddington bauxite mine has many decades of low-cost, high-quality reserves and resources available, whereas for most of South32’s other assets the reserve lives range between 9 and 18 years. Therefore, while alumina (which is produced from bauxite) is a large earnings contributor, it is an even larger component of the company’s overall value.

It is also worth noting that the key end-markets for South32’s commodities are aluminium and steel (with manganese, metallurgical coal and nickel being key inputs into the steelmaking process). Our view is that both these end-markets should exhibit sustainable demand growth over the long term as they have over the last few decades. Steel demand will be dependent on emerging countries continuing to industrialise and develop new infrastructure, while developed countries replace ageing infrastructure. Aluminium uptake will be supported by consumer demand for housing, automobiles, and packaged goods, to name a few.

As contrarian investors, we aim to adopt a countercyclical approach

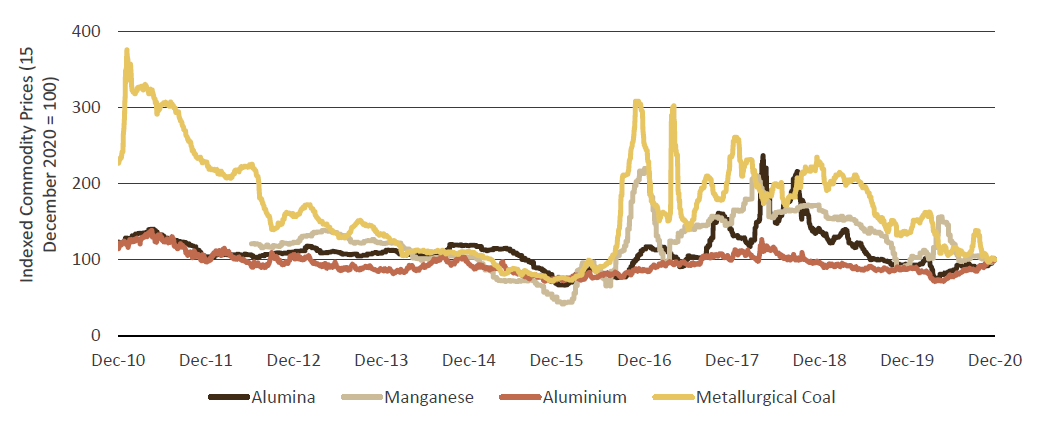

Our interest in South32 was piqued after a period of significant weakness in the prices of the commodities that make the largest contributions to its earnings (notably alumina, aluminium, manganese and metallurgical coal, as depicted in Graph 2).

The price weakness began in mid-to-late 2018 and was exacerbated by the demand destruction caused by COVID-19. We now have a situation where South32’s commodity prices, and therefore earnings, are low relative to history. As shown in Graph 2, with the exception of aluminium, the prices of South32’s other key commodities have been higher than today’s levels for most of the past 10 years.

Graph 2: Historical prices of South32’s key commodities

Source: Platts, Bloomberg, Metal Bulletin, UBS

Commodity share prices indirectly reflect market expectations of future underlying commodity prices. As contrarian investors, we prefer to adopt a ‘countercyclical’ approach: we buy companies when prices are depressed and the share price of the company reflects an expectation that earnings will remain low for the long term. Our view is that it is overly pessimistic to extrapolate today’s low commodity prices too far into the future, given the supply-demand imbalance that this will likely create. We believe South32’s share price today incorporates a lot of pessimism, creating an attractive buying opportunity for patient long-term investors.

South32 has two other attributes that we find attractive. Firstly, it is a low-cost producer, with most of its operations positioned in the first quartile of the cost curve. It can therefore withstand deep price troughs while mostly still generating positive free cash flow. Secondly, it has a strong balance sheet with a cash balance that exceeds its borrowings, so during periods of weak commodity prices (and therefore weak cash flow) it is not under pressure to service an onerous debt burden. Its strong balance sheet also means it is potentially well-positioned to take advantage of any cheap acquisition opportunities that may arise.

What do we pay for South32?

While it’s impossible to predict which of South32’s operations will outperform or underperform in any given year, we estimate that its portfolio of operations in aggregate should be able to generate pre-tax earnings of US$1.3 billion to US$1.5 billion per annum through the cycle. We estimate that this represents a high single-digit return on the capital that would be required to replicate South32’s portfolio of operating assets today. This does not seem excessive to us. With an enterprise value (EV) of just under US$11 billion, inclusive of the future cost of closing and rehabilitating its mine sites, the company is currently valued by the market at seven to eight times these earnings.

We can compare the earnings multiple to South32’s weighted-average reserve life, which is approximately 16 years. With a market capitalisation of a little over US$9 billion and our estimate of post-tax earnings of US$900 million to $1 billion, South32 is trading at 9 to 10 times post-tax earnings. We are therefore expecting to receive 16 years’ worth of earnings, but only paying for 9 to 10 years of those earnings. This strikes us as a good deal.

In addition to the attractive earnings multiple, we have identified three additional sources of upside that may or may not materialise.

- The Hermosa asset in which South32 has invested US$1.6 billion to date. We have not accounted for any EBIT contribution from this asset in our earlier estimate of US$1.3 billion to US$1.5 billion. Even a sub-par return on the investment in Hermosa would represent attractive upside.

- South32 is in the very early stages of exploring a low-cost option to extend the life of the GEMCO manganese mine. If this extension is successful, it has the potential to meaningfully increase the value of the company.

- If South32 manages to complete the sale of their South African thermal coal business, US$700 million of rehabilitation liabilities will be released from the balance sheet.

Our investment thesis is not dependent on any of these three events coming to pass, but if they do, the upside in South32 could be compelling.

As with any investment, a lot could go wrong from here. Structural, political, regulatory or other factors could conspire to negatively impact South32’s commodity prices, sales volumes or production costs. While it is difficult to quantify these uncertainties, our view is that the low earnings multiple that investors pay today, alongside the company’s assets (which are low on the cost curve), and a strong balance sheet provide a reasonable margin of safety against adverse future outcomes.

About Afterpay Limited

Afterpay is a buy-now-pay-later facilitator that allows its users to split the cost of retail purchases into four equal two-weekly instalments over six weeks (with the first instalment paid at the time of purchase). It does not charge its users interest and generates its revenue by charging retailers a percentage of the merchant sales it facilitates as well as by charging its users late fees.

Afterpay’s business is best understood with reference to its unit economics. Table 1 shows its 2020 annual results with reference to its underlying merchant sales.

For the year ended 30 June 2020, retailers were charged 4.1% of merchant sales on average. The company made a further 0.6% of merchant sales in late fees and incurred non-scalable processing costs totalling 1.2% of merchant sales. It incurred bad debts of 0.9% with the net of all these amounts, its net transaction margin (NTM) being 2.6% of merchant sales. It targets an NTM of greater than 2%. Below this NTM are almost $300 million in scalable costs dedicated to customer acquisition, business development, head office costs, IT development and so on.

How successful might Afterpay be?

In order to determine what a mature and successful Afterpay might look like, we first need to determine how big its addressable market is. In Australia, retail sales excluding food retailing, cafés, restaurants and takeaway food services amounted to $104billion for the 12 months to September 2020. This represents approximately 5% of Australia’s gross domestic product.

We can use Australia’s addressable market to infer Afterpay’s total addressable market from the geographies in which it is seeking to grow. The combined GDP of the United States, Australia, the United Kingdom, Canada, Spain, France, Italy and Portugal (Afterpay’s chosen target markets) was US$33.7 trillion in 2019 (and likely lower in 2020). Assuming the same 5% addressable market share as in Australia, Afterpay’s addressable market would be US$1.7 trillion or about A$2.3 trillion in merchant sales.

Table 1: Afterpay’s unit economics

Source: Afterpay Annual Report 2020.

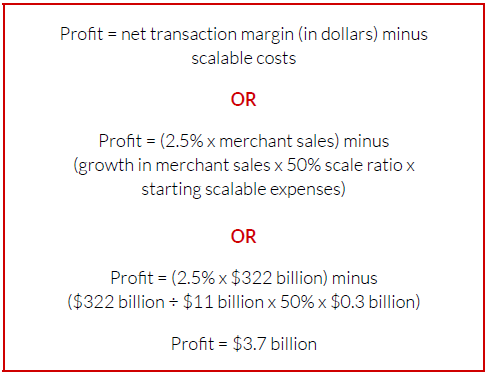

Mastercard’s share of global consumer-to-business purchases is 14%. Let’s assume the successful and mature Afterpay has a market share that matches that of Mastercard’s. This would imply merchant sales of $322 billion (14% of $2.3 trillion).

How profitable might a successful Afterpay be?

Using this level of merchant sales and the unit economics detailed above, it is possible to calculate how much profit Afterpay will generate. First we need to make two important assumptions:

- The current NTM of approximately 2.5% is sustainable.

- Afterpay’s scalable cost base will only grow by half of the dollar transaction margin growth.

Using the above, we can calculate that Afterpay’s earnings before interest and taxes would be $3.7 billion.

How much does an investor pay for Afterpay?

Afterpay currently has a market capitalisation of over $30 billion. It is largely debt free today, but would require a further $18 billion in capital were merchant sales to grow by over $300 billion. Its enterprise value then (assuming the share price doesn’t change between now and then) would be close to $50 billion. Investors are paying over 13 times those future preinterest and pre-tax earnings today.

This mature Afterpay should be as cyclical as any other shortterm money-lender. Its fortunes will rise and fall with the economic cycle that already sees retail spending (upon which it relies heavily) and bad and doubtful debts fluctuate. Banks, which are similarly exposed but have both a more secured loan book (Afterpay’s loan book is unsecured) and longer-dated lending profile (Afterpay’s loans are repaid over six weeks) trade at much lower multiples than this today.

There are a few obvious pitfalls in the analysis above. For example, Afterpay could expand beyond the chosen geographies in our analysis. The bigger Visa might be a better benchmark to judge success than its smaller rival Mastercard. Its customer database might have considerable value across a number of adjacencies that Afterpay is not currently targeting. Or its costs might scale far better than the 50% we have assumed (though doing so would place them among the very best technology companies). But there are also significant risks that we’ve not mentioned (e.g. regulatory risk and competition) that will go a long way towards offsetting any upside and an almost certain near-term future of no or very low profits (as distinct from an established lender like a bank).

At today’s price, the risks in owning Afterpay seem heavily skewed to the downside.

Avoiding the losers is as important as picking winners

The sharemarket today appears to be as polarised as the recent US presidential election, with cyclical stocks being as cheap as they have ever been, while technology and other ‘growth’ stocks are as expensive as they have ever been. Your Allan Gray Australia Equity portfolio is filled with companies like South32 that we think are in the unloved space, and has zero exposure to popular stocks like Afterpay. We think this is the best way to position the portfolio for strong future relative returns.

The above wire is an extract from Allan Gray Australia’s December 2020 Quarterly Commentary, which you can read in full here.

Want to learn more?

Contrarian investing is not for everyone, however there can be rewards for the patient investor who embraces Allan Gray’s approach. Visit the Allan Gray Australia Equity Fund profile to find out more.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Simon Mawhinney is the Managing Director and Chief Investment Officer of Allan Gray Australia, where he leads the company’s investment strategy and oversees the performance of its Australian equity and multi-asset portfolios. Simon joined Allan Gray in 2006 as an analyst, bringing with him a strong background in finance from previous roles at Alliance Bernstein, Macquarie Bank, and Deloitte & Touche. Simon holds a Bachelor of Business Science (First Class Honours) in Finance and Business Strategy, along with a Postgraduate Diploma in Accounting, from the University of Cape Town. He was a Chartered Accountant and is a CFA Charterholder. Known for his contrarian, long-term, value-driven investment philosophy, Simon speaks frequently at industry events and appears in media interviews, offering perspectives on specific securities, as well as portfolio positioning and the Allan Gray contrarian investment strategy.

........

Past performance is not a reliable indicator of future performance. There are risks involved with investing and the value of your investments, including in the Allan Gray Funds, may fall as well as rise. This article represents Allan Gray's view at a point in time and may provide reasoning or rationale on why we bought or sold a particular security for the Allan Gray Funds or our clients. We may take the opposite view/position from that stated, as our view may change. This article constitutes general advice or information only and not personal financial product, tax, legal, or investment advice. It does not take into account the specific investment objectives, financial situation or individual needs of any particular person and may not be appropriate for you. Before deciding to acquire an interest in any financial product or making any other investment decision, please read the relevant disclosure document. We have tried to ensure that the information in this article is accurate in all material respects, but cannot guarantee that it is.

2 topics

2 stocks mentioned

1 fund mentioned

1 contributor mentioned

Simon Mawhinney is the Managing Director and Chief Investment Officer of Allan Gray Australia, where he leads the company’s investment strategy and oversees the performance of its Australian equity and multi-asset portfolios. Simon joined Allan...

Expertise

Simon Mawhinney is the Managing Director and Chief Investment Officer of Allan Gray Australia, where he leads the company’s investment strategy and oversees the performance of its Australian equity and multi-asset portfolios. Simon joined Allan...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Property

The property market’s next big moment is already underway

Livewire Markets

Funds

The hunt for the "great change stories" in global equities

Livewire Markets