TOL - 25th Nov, 2020

Earnings rebound driving recovery in this unloved sector

Earlier in the year we wrote about our attraction to the mining services industry given a favourable macro backdrop, earnings growth and cheap valuations.

While the macro side was very shaky for a few months through the COVID-19 pandemic, we believe it has actually become even more positive given Chinese stimulus and record low interest rates, leading to even higher gold and iron ore prices. Despite some COVID-19 hiccups on the operating side, most mining services companies have sailed through in reasonable shape with the median earnings revision this year for the group down 7%, considerably less than the ~20% fall seen by the broader small cap market.

.png)

Source: AMP Capital

Set up for earnings growth

The COVID-19 pandemic has demonstrated the role of the mining sector in the Australian economy, with mines running largely at full capacity over the past nine months. Miners continued critical maintenance work and expansion projects, with the taps recently turned back on for exploration. Iron ore majors are pushing ahead with growth projects and need to complete them in order to offset other mine closures from depleted resources. We are also seeing a number of developers complete feasibility studies and look to finance new projects – particularly in the gold space.

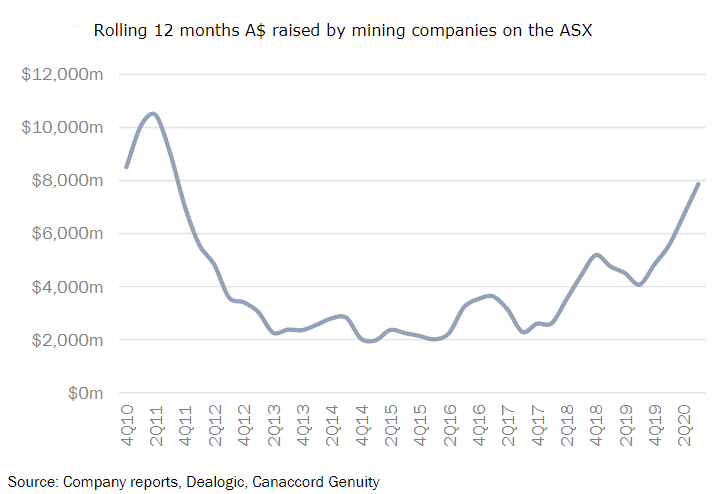

The boom in capital raisings seen over the past six months on the ASX has extended to the junior mining space, with the chart below showing fresh equity raised is up almost 4x from the bottom of the cycle in 2015, and approaching the top of the market in early 2011. We believe this is a good sign for future exploration programs, and coupled with a high gold price (gold typically makes up around 50% of global exploration spend), should set up a good period for companies providing services to the exploration industry, including drillers, tool providers and assay labs.

In our view, medium-term earnings for the sector should be well supported provided commodity prices hold up. An increase in exploration spend should flow through to new deposits being discovered, which is expected to lead to new mines being developed in coming years. Development projects which were parked a few years ago due to low prices are now being restarted, which benefits earthmovers, construction companies, equipment providers and contract miners. Financing projects is becoming easier given lower interest rates and supportive equity markets, while the risks lie in potential cost inflation and labour constraints given border closures.

Coal worries

The coal market has been the main overhang on the sector, with factors such as lower power demand due to the COVID-19 outbreak and Chinese import restrictions leading to low prices across the coal complex. Longer term, the potential for an acceleration of the move away from coal and towards renewable fuel sources through ‘green stimulus’ programs could cause further structural change within the industry. This provides a challenging backdrop for service providers in the coal market. However, we believe that existing contracts will be honoured and provide enough time for providers to shift their business further towards other industries and commodities. Service providers exposed to production are also better positioned as ‘take or pay’ obligations with rail and port providers means it is often more economic for mine owners to operate at a small loss rather than mothball production and pay rail and port fees. Capital markets are also open to provide additional liquidity to operators, with Coronado Coal recently conducting a $250 million equity raising.

Valuation support

Despite the positivity of high commodity prices, increasing capex programs from miners, and earnings which have far exceeded the market average, this bucket of stocks has underperformed the index since the start of the COVID-19 pandemic by 16%, and is trading on an average P/E multiple of just 10x for FY21, compared to 20x for the index. We are under no illusions that this is a cyclical sector that goes through boom and bust periods and deserves to trade at a discount to the market due to this volatility and the capital-intensive nature of the business models. However, we believe the current discount is excessive, especially considering the growth outlook and positive free cashflow being generated by the sector. In our opinion, the market is ignoring the sector in favour of re-open trades, tech stocks and the miners themselves. Nonetheless, we believe that earnings drives share prices and continued delivery on this front will see investors take notice of the sector and see it outperform the market.

We are invested across the sector, and we believe that Seven Group and Macmahon are extremely well-run businesses with a good level of earnings predictability, NRW should benefit from public infrastructure and iron ore work while trading on a free cashflow yield of over 10%, and IMDEX offers leverage to the coming exploration boom in gold.

Not already a Livewire member?

Sign up today to get free access to investment ideas and strategies from Australia’s leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Matt is Co-Portfolio Manager for the Maple-Brown Abbott Australian Small Companies Fund. He has 14 years investment experience in the Australian small and micro cap space, previously working for AMP Capital, IFM Investors and Macquarie Group.

........

While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) (AMP Capital) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided and must not be provided to any other person or entity without the express written consent of AMP Capital.

This article is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives and does not constitute a recommendation, offer, solicitation or invitation to invest.

1 topic

8 stocks mentioned

Matt is Co-Portfolio Manager for the Maple-Brown Abbott Australian Small Companies Fund. He has 14 years investment experience in the Australian small and micro cap space, previously working for AMP Capital, IFM Investors and Macquarie Group.

Expertise

Matt is Co-Portfolio Manager for the Maple-Brown Abbott Australian Small Companies Fund. He has 14 years investment experience in the Australian small and micro cap space, previously working for AMP Capital, IFM Investors and Macquarie Group.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Why ex-20 is the prime hunting ground for ASX returns

Livewire Markets