East coast exposure at Perth prices

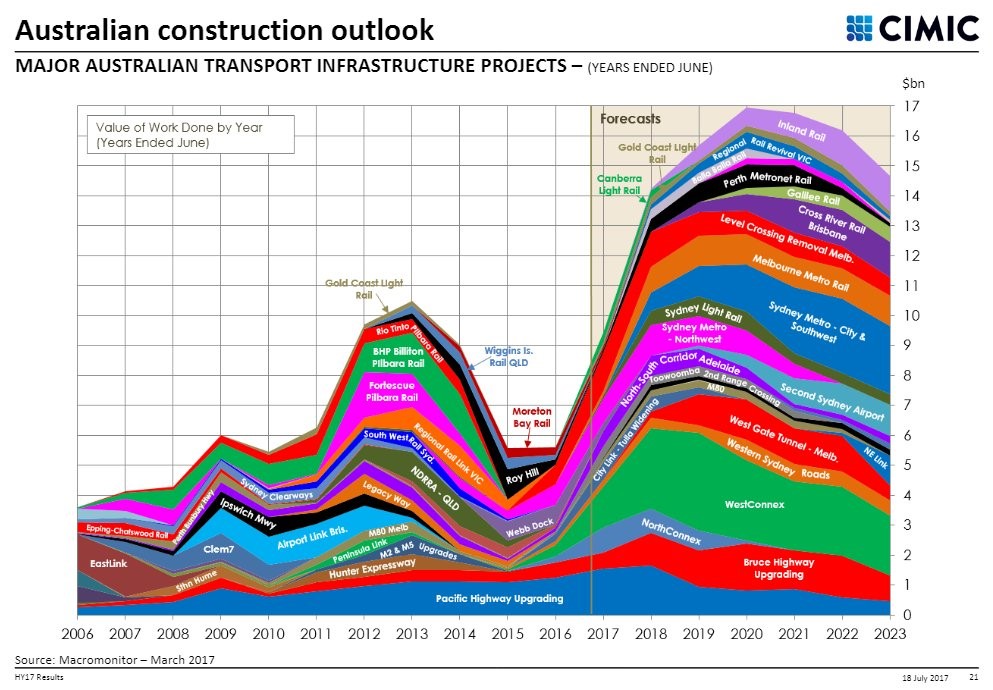

Tighter travel budgets for brokers in recent times have reduced the frequency of visits through WA, with those that do take place generally focusing on the miners and larger mining services companies. This leads to smaller WA industrial stocks being ignored, which can create opportunities. One such opportunity is Veris (VRS) a surveying roll-up offering exposure to the east coast infrastructure boom which is set to accelerate as shown below.

Source: Macromonitor, Cimic

VRS has gone through a period of transition over the last four years. In 2013 the Board took the decision to diversify away from mining in favour of the highly fragmented surveying and professional services industry. VRS announced its ninth surveying services acquisition last month. The acquired company, LANDdata, is based in Canberra and offers exposure to western Sydney infrastructure projects such as the Badgerys Creek airport and the Melbourne – Brisbane rail project.

As with many roll ups, the integration of new businesses has not been without incident. Delays in integration, margin squeeze due to increasing surveyor wages prior to cost pass through, and sharp declines in the infrastructure business led to a weak 1H17 result and share price weakness. Since then, founding director Adam Lamond (holds 14% of VRS) has resumed the role of Managing Director and the focus on integration of acquired businesses has intensified. Surveying rates on the east coast have started to tick up as the market for infrastructure facing professional services tightens, providing a tail wind for company earnings.

We are confident of an improved 2H17 result and positive outlook for the company. We consider director buying announced on the 4th and 11th of May as being supportive of our view. Further, we note the limited amount of organic growth in consensus forecasts, which appears conservative versus the infrastructure expenditure pipeline above and anecdotes of increasing rates in the industry.

Trading on FY18 Enterprise Value/ Earnings Before Interest Taxes, Depreciation and Amortization of 3.0 times, with net cash on the balance sheet, we view this risk / reward proposition as compelling.

VRS is a core holding in the Perennial Value Microcap Opportunities Trust.

Disclaimer: Please note that these are the views of the writer and not necessarily the views of Perennial Value.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Sam is an Equities Analyst in the Perennial Value Smaller Companies Team, responsible for the research coverage of small cap resources stocks.Sam joined Perennial Value Management in April 2012, from the Royal Bank of Scotland in Sydney where he held the role of Metals and Mining Analyst. During that time he won Starmine's 2011 top Australian Metals and Mining Analyst Award. Prior to transitioning to the investment industry in 2008, he commenced his career in the mining industry gaining open pit mining and exploration experience across key commodities including gold, nickel, iron and uranium. During his six years in the mining sector, Sam held roles with industry leaders such as Equigold and Jindalee Resources in Australia and West Africa. Sam holds a Bachelor of Science Degree (majoring in Geology and Chemistry) and a Postgraduate Honours Degree in Geochemistry from the University of Western Australia. He also holds a Graduate Diploma in Applied Finance and Investment.

Sam is an Equities Analyst in the Perennial Value Smaller Companies Team, responsible for the research coverage of small cap resources stocks.Sam joined Perennial Value Management in April 2012, from the Royal Bank of Scotland in Sydney where he...

Expertise

Sam is an Equities Analyst in the Perennial Value Smaller Companies Team, responsible for the research coverage of small cap resources stocks.Sam joined Perennial Value Management in April 2012, from the Royal Bank of Scotland in Sydney where he...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Investing for the biggest market shift since the GFC

Livewire Markets

Equities

Why ex-20 is the prime hunting ground for ASX returns

Livewire Markets