Electro Optic Systems – One to put in your sights

Electro Optic Systems (EOS) has been one of the most tipped stocks on Livewire Markets this year.

It supplies laser optic sights to the US, NATO and Australian military and counter-drone technology and has recently made an acquisition, Audacy, that will see it enter space. The company has cutting edge laser guidance systems allowing remote access targeting. It also has communication systems and now space capabilities. It is Australia’s largest defense exporter (according to EOS) although I suspect Austal (ASB) may have something to say on that.

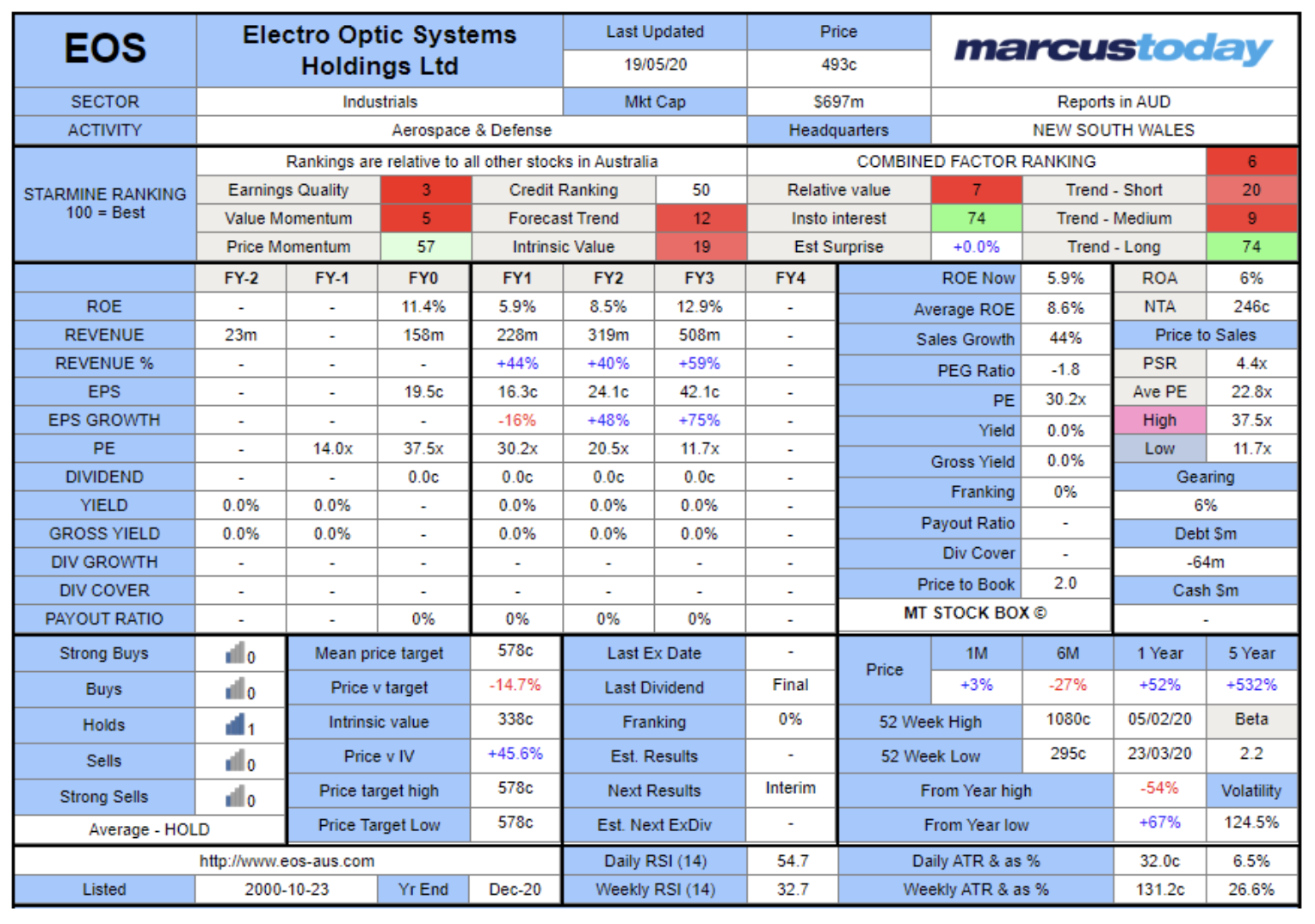

It has recently raised funds and the balance sheet looks better given cashflow issues. The company has done a placement at 475c to raise $134m and an SPP at 440c. Importantly, it has a US production site coming on stream in Mid-2020. The market cap is around $770m.

Technically it has been trending sideways under some pressure mainly due to the capital raising. It is making tentative signs of breaking higher with a PT of around 700c possible if the contracts and cash payment timings fall into place.

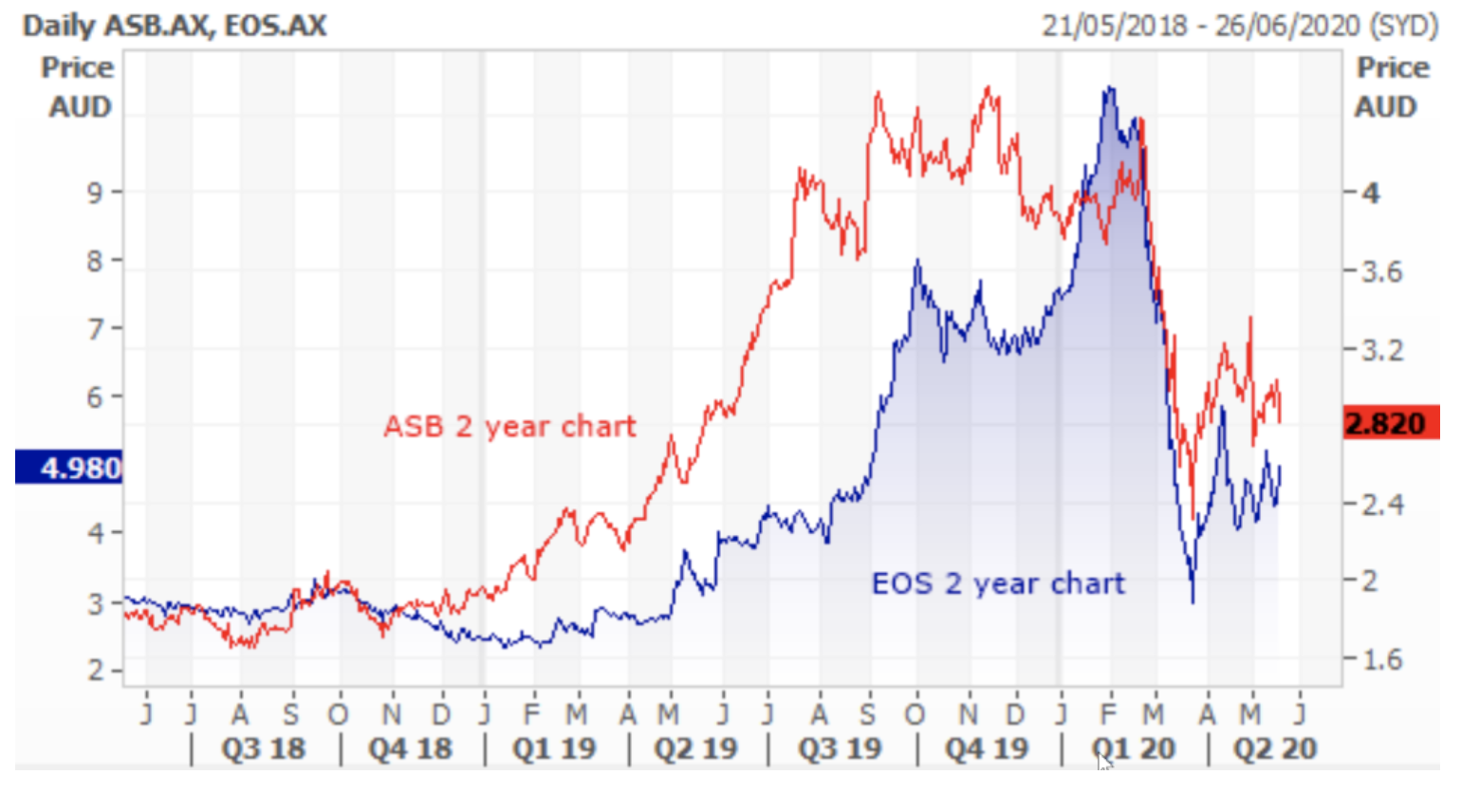

Its nearest comparison could be Austal (ASB) which like EOS is a large US military contractor. It also has US production capabilities together with local operations. Margins are not in the same league as EOS, but the orders are significantly bigger in monetary terms.

You can see how both have been slow grind stories for some time before a rerating as contracts, revenue and hoped for profit started rolling in.

The impact of COVID-19

The company has suffered some timing issues surrounding CV19, although it has had no contract cancellations or diminution. It has an unchanged pipeline of potential contract awards. The company has been suffering from late payment and deferrals, hence the need for a capital raise to ensure it has flexibility and strength to see it through the temporary disruptions. Some $70m of export revenue has been deferred and $9m EBIT on contract disruptions.

90% of the company revenue is from exports and as such is reliant on logistics and the supply chain which has been challenging given the closure of international air transport hubs.

Deliveries have been delayed and cash receipts have been materially impacted as they are delivery based.

Output at its Australian operations has suffered after production was split into two shifts, but adjustments are underway to restore output.

The Outlook for 2020

The company has guided to revised revenue of $230m and $27m EBIT which is around 25% growth prior to FX gains. This assumes no contract cancellations.

USA production is on schedule to begin production from mid-2020 and will ramp up to $400m in annual capacity over the next two years.

One catalyst for a rerating is the opening of production in the US and a return to full production in its home base of Hume.

The company has a resilient pipeline of government programs. Some revenue has now been pushed out to FY21.

The recent Audacy acquisition was unfortunately timed as CV19 hit. However, it looks like a good strategic fit and cost around $10m in cash. Audacy was granted a space station spectrum license by the FCC which gives it the ability to establish wideband capabilities for satellites and other space vehicles with real-time data transfer. The company will be required to launch a satellite constellation by June 2024, so there are some Capex requirements further out.

Key metrics

Sales are the driver of EOS. The market will need to see the rebound from CV19, and the deliveries timetable re-established. If sales can rise to $508m as forecast the share price will do very well in a couple of years.

The Balance Sheet

The balance sheet has been shored up with a recent capital raise through an institutional placement at 475c and a SPP at a slightly better price of 440c.

EOS has production of around $60m of deliverable product which has been disrupted so payment has been delayed.

It had a cash balance of $43m which has now been boosted by the capital raise.

The money raised will ensure production continues but cash receipts for the products will be delayed until Q4 FY20.

Following the placement, the company should have sufficient cash to generate $27m EBIT and produce billable goods of around $140m within FY20, for which cash payment is expected.

The balance sheet should be able to handle timing differences of production versus payment.

Following the capital raise, it will have $171m of Pro-forma cash together with a $15m line of credit from EFIC. The money raised will be used to fund production runs and secure government contracts together with the completion of the Audacy acquisition for EOS Space.

Broker consensus

The company has very little broker coverage. One broker has a hold.

In terms of fund managers, Monash with Simon Shields is very bullish on the outlook.

Summary

The stock has fallen hard and there are risks that countries try to use local providers for defense works. We have already seen Austal (ASB) lose a contract in the US to a competitor and it is not out of the question that EOS could see some erosion of its markets given nationalistic constraints. However, at current prices, it has fallen a long way from its pre-CV highs, and with only timing seemingly an issue, it now represents good value and leverage exposure to the US defense market.

The acquisition opens a channel in space for EOS to support market demand, leveraging the EOS advantages in the space communications domain to protect satellites from space debris and the satellite platform means that customers will be able to access more bandwidth for optical technologies. Think 5G for weapons guidance systems. As space debris grows, EOS will be at the final frontier helping to clean it up.

It is not expensive looking out beyond the current disruptions. Good technology and US-based manufacturing coming on stream mid-year and exposed to a sector that is relatively immune from spending cuts although UAE and other Middle East contracts may see issues as oil prices remain at subdued levels.

Speculative Buy for recovery with the defense sector delivery and payments. The US manufacturing operation could be a catalyst for a rerating. The balance sheet has been improved, now just a question of timing. Potentially some short-term indigestion from recent capital raise.

Find out more

We offer our investors and newsletter Members complete transparency on our investment decisions. You can follow what we do in our portfolios on a daily basis via our daily podcasts and in the newsletter. For our daily Strategy advice you can join Marcus Today - click here to SUBSCRIBE or to sign up for a FREE TRIAL

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Henry started in financial markets in London in the 80s as an option trader before coming to Sydney and spending 7 years at Macquarie Bank including a stint running equity derivatives and cash trading.

2 stocks mentioned

Henry started in financial markets in London in the 80s as an option trader before coming to Sydney and spending 7 years at Macquarie Bank including a stint running equity derivatives and cash trading.

Expertise

Henry started in financial markets in London in the 80s as an option trader before coming to Sydney and spending 7 years at Macquarie Bank including a stint running equity derivatives and cash trading.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Investing for the biggest market shift since the GFC

Livewire Markets

Equities

Why ex-20 is the prime hunting ground for ASX returns

Livewire Markets