February Review: Small Losses and an Ugly Outlook

February was generally negative for risk assets, but it was by no means uniform. Equities fell in the US (-0.4%), China (-2.3%), Australia (-2.5%), Europe (-3.3%) and Japan (-8.5%). Credits spreads mostly pushed wider, but the divergence in US high yield bonds continues to grow with BB’s rising a little and CCC’s continuing their fall. The Bloomberg Commodity Index fell a little (-1.6%), but gold (10.7%) and iron ore (17.8%) had big gains whilst US natural gas (-25.7%) plummeted. Gold is finally catching an updraft after falling for 3 years. Whilst gold doesn’t deliver any yield to its owners, in a negative interest world that becomes a positive rather than a negative.

For those with a bearish tendency, their appetite for bad economic news was satisfied in February. It’s not just Zerohedge pumping out the bad news, there’s plenty of it on Bloomberg as well. Those arguing that’s it is just a commodity and manufacturing downturn in the US will be hoping that a service sector PMI printing below 50 is just an aberration. US lay-offs spiked in January, factory orders are falling whilst inventories are rising and tax collections from employee pay packets are falling. Two of biggest generators of jobs in recent years have been retail and restaurants. Store closings and a sharp decline in the Restaurant Performance Index aren’t good signs.

The chasm between real earnings and the version that companies are selling is the worst since 2008. If you take the management view combined earnings of S&P 500 companies grew by 0.4% in 2015. If you take the accountant’s view combined earnings fell by 12.7% last year, with only a tiny gain since 2010. That’s a pretty good reason for stocks to be down as much as they have been. Yes, falling energy prices and the higher US dollar have played a part and there’s an argument for taking into account those impacts. However, I don’t remember anyone wanting to exclude those factors when their impact was positive so it’s a stretch to say they should be excluded now.

In US consumer credit subprime auto arrears and defaults are starting to ramp-up. 3% down loans (97% LVR/LTV) are making a comeback via Bank of America and Freddie Mac. Something like US$1 trillion of 2005-2008 era home equity line of credit loans (HELOCs) are now converting from interest only to 15-year principal and interest repayments. These HELOC borrowers can expect to see their monthly payments jump by 100-200% when their reset arrives. HELOCs are typically second ranking, mostly held on bank balance sheets and arrears and defaults have been jumping after the resets occur so it is something to watch closely.

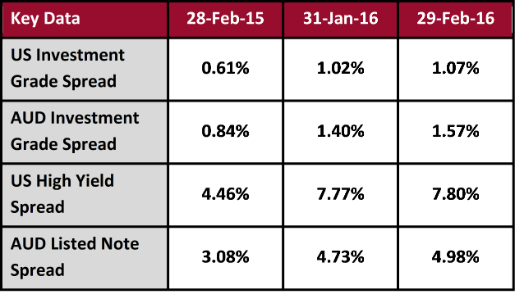

The US high yield debt markets have largely ground to a halt for the lowest quality borrowers, those rated B- and below. The poor performance of CLO equity and sub-investment grade tranches is making CLO issuance much harder, which is horrible news for borrowers as 61% of leveraged loans were bought by CLOs last year. High yield bond issuance is also off to a very slow start at about a quarter of the year to date pace of the last two years. There’s been more than a few failed deals.

The travails of Solera Holdings is an interesting case in point as the B1 rated, first ranking loans were oversubscribed and syndicated at reasonable pricing. Conversely, the Caa1 rated second ranking bond offering was pulled after only half the desired demand could be found even with an 11% yield. The fact that over 30% of US high yield bonds and over 10% of leveraged loans are trading at distressed levels also makes it hard to sell new deals – investors are nursing heavy losses and are distracted with the workouts on what they already own.

Many investment funds have had a rocky start to the year. One Bridgewater fund was reported to be down 10% in two weeks and Citadel is shuttering another hedge fund. A good portion of sovereign wealth funds have been built on the back of oil revenues, with lower prices expected to see these funds become net sellers of equities to the tune of US$70-400 billion in 2016. A defined benefit pension fund in the US with 400,000 members has flagged 40-61% reductions in payouts to members as its assets simply aren’t enough to meet its future liabilities.

US oil in storage is at the highest levels in 86 years with reports that some areas are refusing requests for storage forcing producers to sell at distressed prices. One statistic that highlights the carnage is a Bloomberg calculation that the net debt to EBITDA for listed commodity companies is 8.3 times. This means that on average commodity companies have way too much debt and almost no equity value. The early stage of a wave of bankruptcies predicted for this year is starting to impact banks with recent quarterly reports having banks disclosing their oil and gas exposures and increasing their provisions. It’s not as bad as some would guess as commodity companies have mostly borrowed through bonds rather than loans. Based on what’s been disclosed some large banks could lose a fair portion of a year’s profits in oil and gas losses, but spread over a three to four-year period.

It’s not just fossil fuel energy production that is under pressure, renewables are also suffering. PE firms are raising capital and targeting renewable projects as governments are looking to cut renewable subsidies in order to help balance their budgets. Spain’s largest renewable company Abengoa has filed for bankruptcy protection in the US noting US$10 billion in liabilities. Environmentalists jumping for joy at the struggles of fossil fuel producers obviously missed Economics 101. Cheap coal, gas and oil makes renewable electricity relatively more expensive. It means wind farms and solar farms will be harder to fund as some of their predecessors have not hit their target returns. Development of battery storage will eventually lead to far more cars being battery powered but in the short term it makes buying a new Tesla more a cool factor decision than a cost saving decision.

China’s debt levels grew at almost 50% of GDP last year (see graph below) and set a new record for a single month in January growing at roughly 5% of the size of the economy. Debt growth in February is thought to be about the same. The global increase in total debt to GDP has averaged 2.6% per year since 2007, so China increasing debt by 5% in a single month is completely off the charts. Foreign exchange outflows in January were almost another record at US$99 billion, but some see the data as fudged as crucial parts were removed whilst others think it is just a misunderstanding. Hedge fund manager Kyle Bass called China a “ticking time bomb” with the currency overvalued and the banks insolvent. The communist party newspaper and one of their investment banks think Kyle is dead wrong.

[China_debt__2_.jpg.jpeg]

With the Chinese government now openly asking the media to stick to the party line it is hard not to be suspect of anything the government or the Chinese media is saying about all being well and problems being contained. The securities regulator has been sacked following the share market falling by 47% from the peak and the disastrous implementation of circuit breakers in January. A fascinating article highlighted how this sort of external pressure pushes Chinese bankers to lend even when the loan quality is awful. One of the last non-official surveys remaining, the Minxin monthly private company survey, has companies seeing conditions well into contraction territory.

The collapse of the Ezuabo Ponzi scam is thought to have ensnared up to 900,000 Chinese “investors”. Estimates are that US$7.6 billion has been lost after staff spent up on a lavish lifestyle. This won’t be the end of it though, as 25% of Chinese peer to peer platforms are thought to be fraudulent. As an outsider it’s difficult not to see the Chinese investment markets as a place where anything goes. A report that more than 50% of listed Chinese companies have pledged their own stock in order to secure loans is just another reason to be sceptical of investing in Chinese shares. Investigations continue on two companies (amongst many) with one having lost ¥500 million from its bank accounts and another having (apparently) completely lost four years of financial records when a truck was stolen.

For those wondering how a Bernie Sanders style experiment would work for America, Venezuela might be a handy guide. Plane loads of new cash are being flow in as the 720% inflation rate means that citizens need a lot more physical cash to purchase everyday items. Even when the cash is in hand it doesn’t guarantee a successful shopping trip as supermarkets have been running out of the basics with episodes of looting and social breakdown being predicted. The lack of foreign currency reserves, now almost exhausted from repayments on foreign currency debts, means imports are increasingly difficult to source. The country has had to resort to sending its gold overseas in order to secure new foreign currency loans as lenders understandably don’t trust the government to be good for it. Credit default swaps are pointing to a default within months, not years. Such is the good life within the “socialist paradise”.

Neighbouring Puerto Rico is also considering a default on its debts within months, but unlike Venezuela it is a territory of the US and not an independent country. US politicians are trying to figure out a way to support it with a restructuring of its debt as states and territories (unlike municipalities) aren’t supposed to be able to default on their debts. Universities in the states of Louisiana and Illinois are being threatened with shutdown within a year as state funding is at risk. Schools in Detroit, Michigan might also face drastic cuts in the near term as the school system is issuing debt at very expensive interest rates in order to keep spending more than its revenues. Nigeria has denied asking for a $3.5 billion bailout, but with inflation above 60% and a soaring CDS there’s clearly problems.

A key theme in February was the argument that central banks have failed. Some say this is not because they haven’t done enough but because they simply don’t have available the tools necessary to get economic growth going again. Helicopter drops of money are being suggested by some “serious” academics as the way to fix things. Those who remember former Australian Prime Minister Kevin Rudd’s version of this will recall that a decent chunk ended up in poker machines. It was good for the profits of the casinos and gambling dens but the country has been paying interest on the debt incurred to fund the one-off payments ever since. If we had built the national broadband network or a high speed rail link we’d at least having something other than debt to show for it now.

The other side of the argument is that we need to let inflated debt levels deflate or bust. Ireland and Iceland have both done this and have started growing again. Ireland chose to nationalise the bank debts and will be paying for it for decades whilst Iceland left its bank creditors to fend for themselves. Either of those is a better outcome than Greece where the six-year train wreck continues and another round of bailout funding is being sought.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Narrow Road Capital is a credit manager with a track record of higher returns and lower fees on Australian credit investments. Clients include institutions, not for profits and family offices.

1 topic

Narrow Road Capital is a credit manager with a track record of higher returns and lower fees on Australian credit investments. Clients include institutions, not for profits and family offices.

Expertise

Narrow Road Capital is a credit manager with a track record of higher returns and lower fees on Australian credit investments. Clients include institutions, not for profits and family offices.

Expertise

Comments

Comments

Sign In or Join Free to comment