Even in unprecedented times, the price you pay still matters

The unprecedented impact of COVID-19 across business and society is invoking a fiscal response last used by wartime governments 75 years ago, according to Schroders.

Andrew Fleming and Martin Conlon of the Schroders Australia Australian Equities team explained how developed economies are deploying World War 2 levels of fiscal stimulus. They also discuss portfolio positioning for current conditions and why it’s the price you pay that matters most in the end.

Waging war on a financial virus

When Rishi Sunak, UK Chancellor of the Exchequer, unveiled Britain’s enormous 350-billion-pound stimulus package, he asserted: “We have never in peacetime faced an economic fight like this one.”

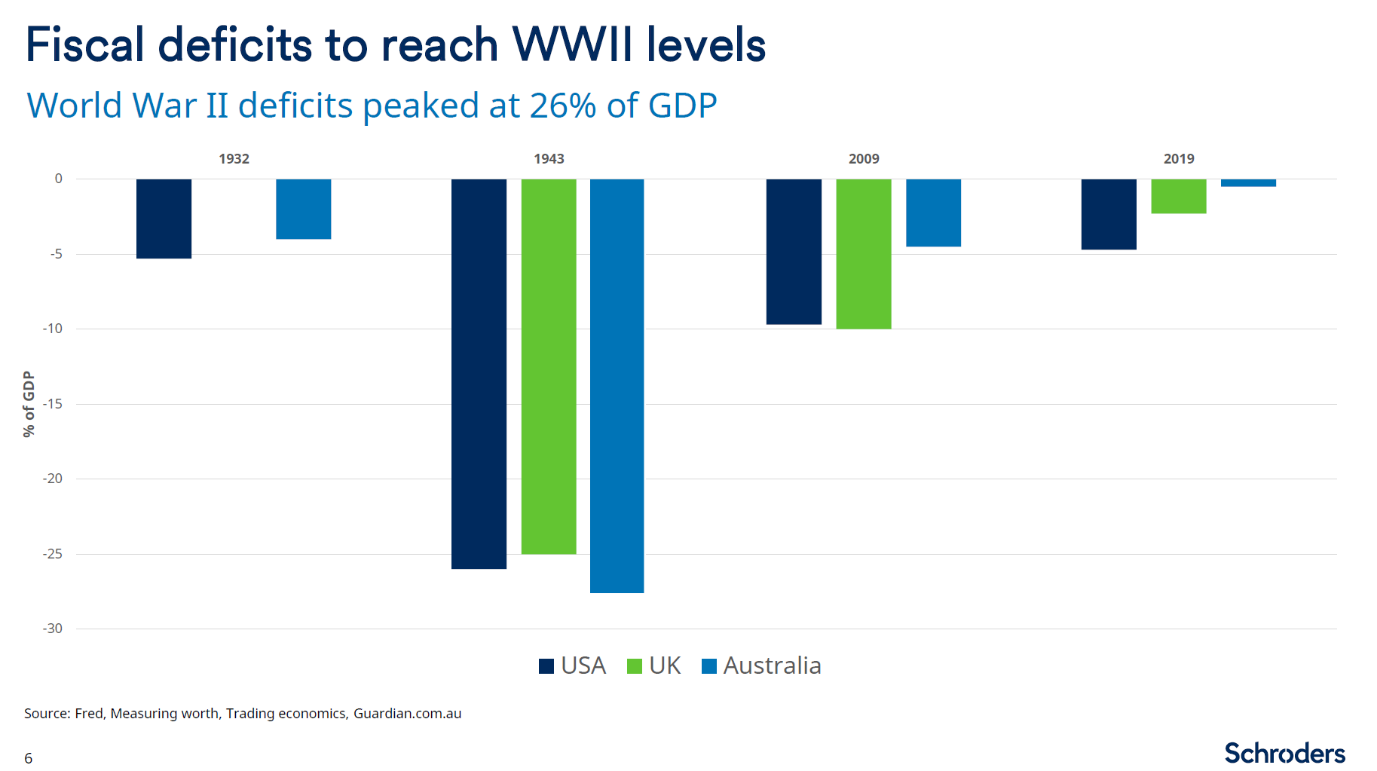

Fleming captured that sentiment perfectly the chart below, which shows that governments are positioning themselves to unleash wartime responses at the fiscal level in response to COVID-19.

“We’re getting very close to those World War 2 levels. If 25% is that magic number, you can see that the UK has already announce measures there are ~17% of GDP plus a few percent from their deficit to start with. With the contraction of GDP that you could expect given what we’re going through, we’re starting to get to numbers in the 20-25% range over the next month or two.”

The question is whether even this level of stimulus would be enough to support the sheer number of workers, businesses and other entities thrown in turmoil due to the global pandemic. The key to that of course is how long it takes governments to bring COVID-19 under control, with cases continuing to skyrocket around the world and the U.S. disturbingly surpassing China overnight as the country with the most infections.

“There are some economists forecasting U.S. GDP to contract 25-30% this quarter. That’s a rate of decline that we’ve never seen before and we’re not expecting a V-shaped recovery. There’ll be quite a lot of dislocations in investment markets because of the shock we’re going through.”

It’s the price you pay that matters

In discussing the recent equity market carnage, Fleming pointed out a key lesson for investors: pay a high price, expect a lower future return. It’s probably the most important lesson investors can take away from a bear market that’s brought a swathe of high PE stocks to their knees.

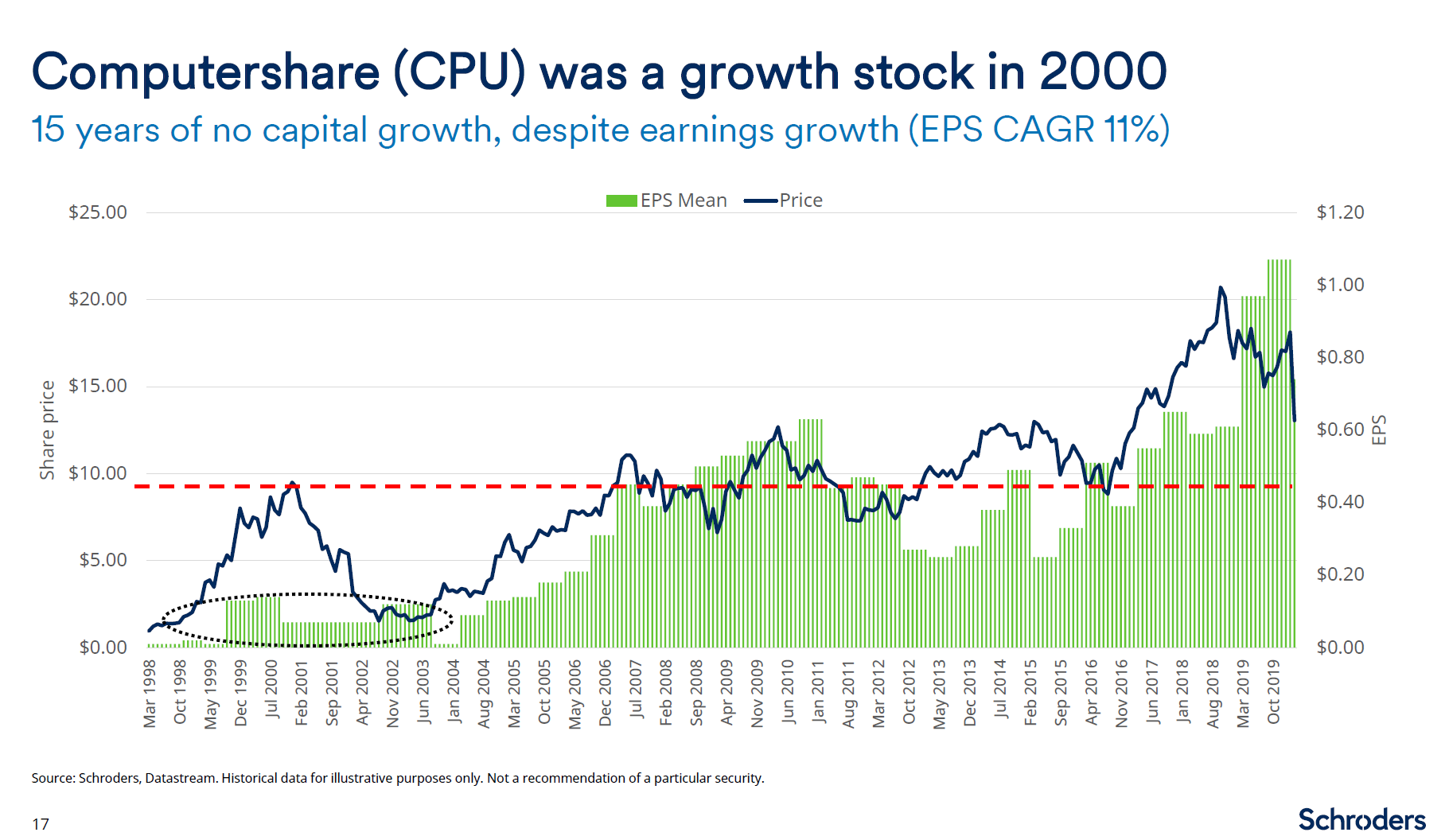

Fleming said the 40-70% share price falls across hyped up IT-stocks over the past month casts his mind back to when Computershare (ASX:CPU) was Australia’s posterchild of the early 2000s tech bubble. Even though Computershare was growing earnings, its stock price flew past business fundamentals and then crashed back down to earth.

Consequently, as the chart below shows, for those investors who bought at the top, the convergence between earnings reality and valuations meant 15 years of no capital growth.

“Even with earnings per share growing at 11% CAGR, this example shows you the only thing that matters as an investor is the starting multiple. It’s a note of caution that we now add for investors paying greater than 30-40 times P/E. It’s very difficult for investors to generate superior returns in the long-run when they pay high prices.”

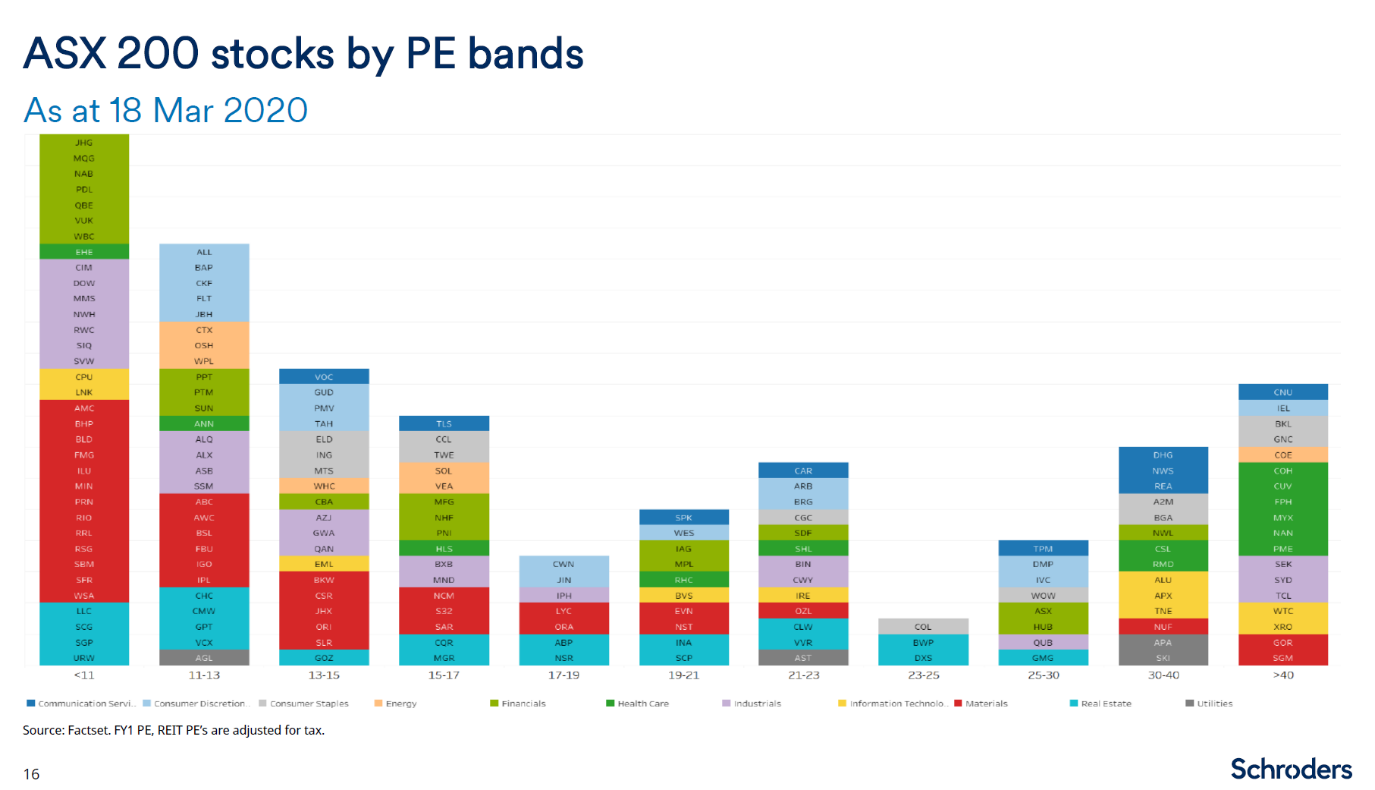

And he warns that could be a portent of things to come for some of the expensive shown below.

Where are ASX 300 valuations now?

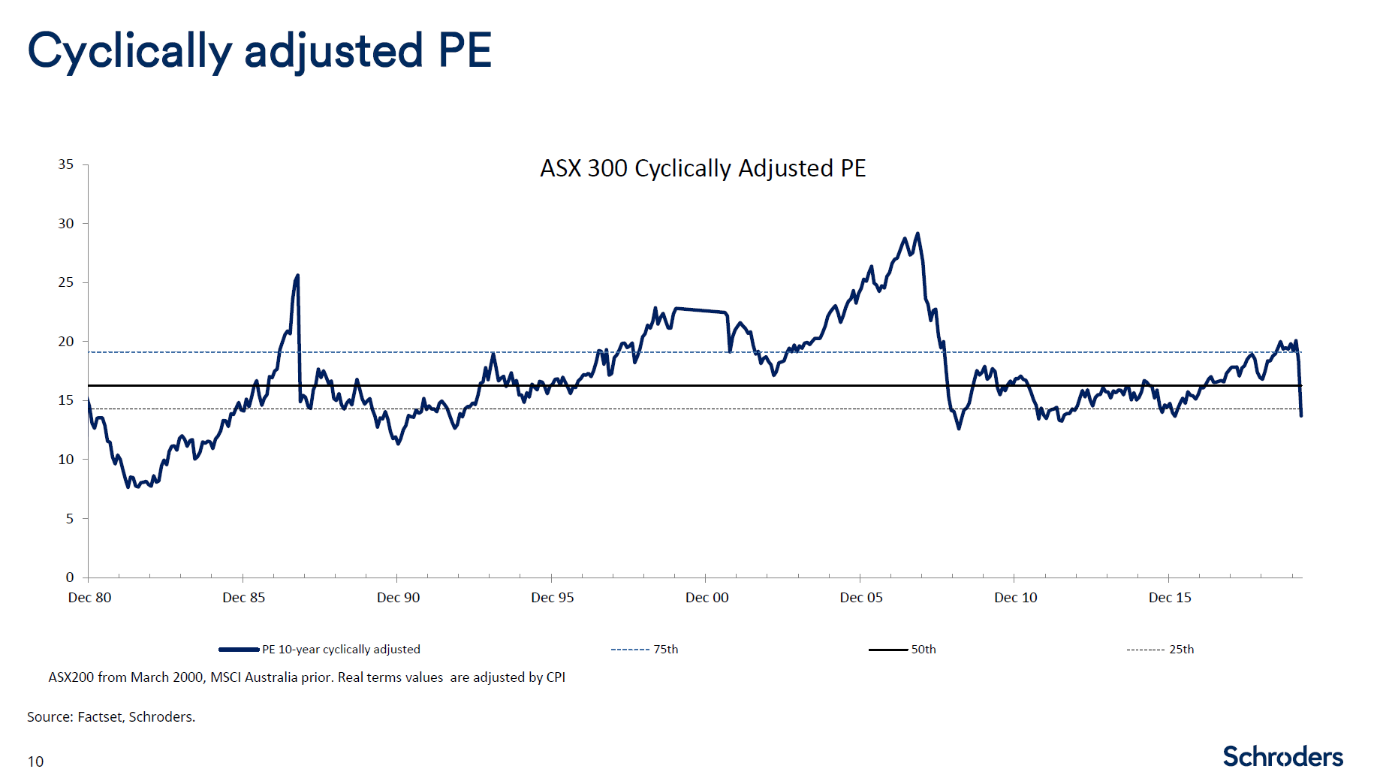

Taking a step back to consider the broader market, Fleming says cyclically adjusted P/Es are approaching levels last seen during the global financial crisis (see chart below).

While you’d think that this would whet buyers’ appetites, Fleming offers those in search of value a big caveat: significant downside risk remains.

“There’s a lot priced in already albeit earnings haven’t rebased yet, so even on a 10-year average there will be a material upwards revision to multiples. Obviously significant earnings declines will come through in August FY 20 earnings, but the knock on into FY 21 could be material as well depending on the extent of the dislocation in the labour force and how that will knock on through into consumption and activity.”

Portfolio positioning

Conlon says the key to investing in the current environment is to consider where valuations are, and where earnings will be through the cycle. While there have been sharp market falls across almost all sectors, this could present opportunities to buy businesses at more attractive prices.

Here, he shares some examples of how Schroders are positioning their equity portfolios:

- Favouring resource stocks, and industrial and consumer staple stocks with defensive revenue and earnings streams that are well-placed to weather the volatility.

“The majority of resources businesses have exceptionally strong balance sheets and proven capability in dealing with fluctuating price cycles and volatile revenue streams. To date, the effect on iron ore pricing has been mild. While prices for some commodities, such as alumina, aluminium and copper are more depressed, nearly all are still in relatively strong financial positions. We believe most resource stocks are now attractively priced and offer strong long-term return prospects.”

- Selectively adding risk in businesses where valuations have become more attractive and can be expected to rebound strongly post short-term challenges.

“Unsurprisingly, airline, tourism, casino and gaming stocks have been amongst the hardest hit by COVID-19. Given capacity reductions, high fixed costs and minimal short-term revenue, solvency issues will be significant for these industries. At the other end of the spectrum, supermarkets are experiencing an increase in earnings – however we feel this is transitory and should not materially impact valuation.”

- Cautious on bank positioning given the likelihood of increasing bad debts and the limited ability of monetary policy to provide support.

“The good news is that all Australian banks have materially boosted their capital levels since the GFC and are among the best capitalised banks in the world. Bank stocks with the exception of CBA are currently very cheap. However, for now we remain cautious on the sector due to its sensitivity to bad debts, high correlation to economic risks and high absolute weight in the equity market.”

Conlon is also adding smaller positions in energy stocks where valuations have been savaged, albeit cautiously. On the flip side, an area he’s continuing to avoid is healthcare where “already aggressive valuations have become even more aggressive relative to an overall equity market level which is materially lower.”

Never miss an update

Stay up to date with my content by hitting the 'follow' button below and you'll be notified every time I post a wire. Not already a Livewire member? Sign up today to get free access to investment ideas and strategies from Australia's leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Vishal has over 15 years' experience in financial journalism and has a particular interest in property, exchange-traded funds (ETFs), investing strategy and financial history.

........

This article is for informational purposes only and should not be considered financial advice. The article may contain the views or opinions of third party contributors to Livewire Markets. These contributors have not considered your objectives, financial situation, or needs. The information in this article should not be relied upon as a substitute for personal financial advice. Livewire Markets recommends that you seek independent advice before you apply for any financial product or service. Livewire Markets is exempt from requiring an AFSL under APRA Regulatory Guide 36, section 66.

4 topics

1 stock mentioned

2 contributors mentioned

Vishal has over 15 years' experience in financial journalism and has a particular interest in property, exchange-traded funds (ETFs), investing strategy and financial history.

Expertise

Vishal has over 15 years' experience in financial journalism and has a particular interest in property, exchange-traded funds (ETFs), investing strategy and financial history.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Investing for the biggest market shift since the GFC

Livewire Markets

Equities

Why ex-20 is the prime hunting ground for ASX returns

Livewire Markets