Hero or Zero: $500m Macquarie hybrid lists on Wednesday...

The $500 million Macquarie Bank Capital Notes 2 (ASX: MBLPB) hybrid begins trading on Wednesday, and it will be fascinating to see how it performs.

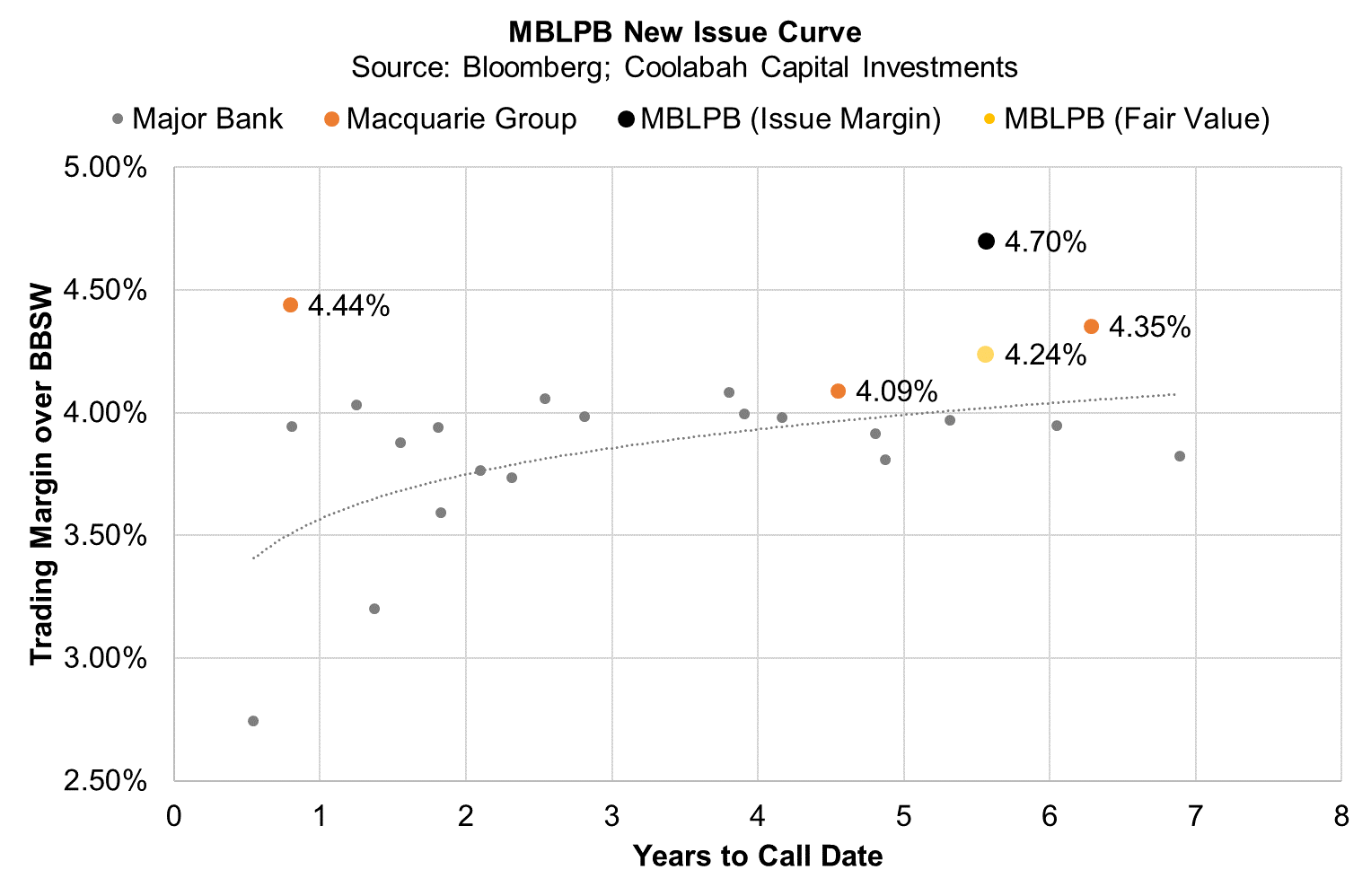

This new deal was issued on a margin of 4.7% (470 basis points) above the quarterly bank bill swap rate, implying an all-in grossed-up running yield of circa 4.8%. At the time, we thought it was attractive and subscribed for our portfolios.

Based on Friday's ASX pricing, it looks like the interpolated credit spread for MBLPB would be around 4.24% above the swap rate (given it sits between two other Macquarie Group hybrids---MQGPC and MQGPD---in terms of tenor), which suggests a clean price of about $102.11 (or a capital gain of more than 2% above its $100 face value) in lieu of the 46 basis points of prospective credit spread compression from the 4.7% issue margin.

Importantly, this doesn’t take into account the superior creditworthiness of a Macquarie Bank hybrid relative to the existing Macquarie Group hybrids. More precisely, the new MBLPB hybrid would be notionally rated BB+ by S&P compared to the lower BB ratings for MQGPC and MQGPD (this is because of the difference between a hybrid issued by the banking entity as opposed to the group where only the bank gets the benefit of things like government-guaranteed deposits and access to the RBA's emergency funding facilities).

While S&P does not officially rate ASX hybrids (it only rates their unlisted equivalents), MBLPBs theoretical BB+ rating puts it on the cusp of the investment-grade/high-yield threshold and one notch below the investment-grade BBB- ratings the major banks' hybrids attract from S&P when issued in the over-the-counter market.

If investors were to price in this superior creditworthiness (ie, the higher rating) by, say, reducing MBLPB’s trading margin 10 basis points tighter than its currently interpolated spread using the Macquarie Group hybrid curve (ie, down from 4.24% to 4.14%), this would increase the expected clean price $0.46 to $102.57.

I was recently interviewed by Pinnacle Investment Management's Gerald Willeston about the new Macquarie hybrid issue, which you can watch by clicking on the player below. The second video is another interview with Gerald where I discuss where I think hybrids should be classified in a multi-asset-class portfolio (either as high yield fixed-income or very low beta, defensive equities).

Never miss an update

Stay up to date with my content by hitting the 'follow' button below and you'll be notified every time I post a wire. Not already a Livewire member? Sign up today to get free access to investment ideas and strategies from Australia's leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha Managers” based on his risk-adjusted performance throughout his career across. He previously worked for Goldman Sachs in London and Sydney, the Reserve Bank of Australia, and founded the award‐winning research/investment group, Rismark. He has regularly advised governments, developing unique policy proposals. Chris graduated with the University Medal (Economics & Finance) from Sydney University. He studied in the PhD program at Cambridge University in 2002/03, leaving to set up his funds business.

........

Disclaimer: This information has been prepared by Smarter Money Investments Pty Ltd. It is general information only and is not intended to provide you with financial advice. You should not rely on any information herein in making any investment decisions. To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this information. Past performance is not an indicator of nor assures any future returns or risks. Smarter Money Investments Pty Limited (ACN 153 555 867) is authorised representative #000414337 of Coolabah Capital Institutional Investments Pty Ltd, which holds Australian Financial Services Licence No. 482238 and authorised representative #001277030 of EQT Responsible Entity Services Ltd that holds Australian Financial Services Licence No. 223271.

1 topic

1 stock mentioned

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha...

Expertise

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha...

Expertise

Comments

Comments

Sign In or Join Free to comment