Hiding in plain sight

As a fund manager in global equities, we are often asked about stock selection, especially at times like now when there has been a frenzy of investors that have piled into relatively few stocks such as Amazon, Apple and Tesla.

I’ve written about the risks of buying these stocks at the top of the market, so here I’d like to share what we feel are some of the many other opportunities out there with a much greater chance of a return on investment over the medium to long term.

One is Loews – a diversified US based holding company operating in energy, hospitality, insurance and packaging, essentially a mini-Berkshire Hathaway.

Key holdings include:

· 89.6% interest in CNA (a large NYSE listed commercial and casualty insurance company)

· 100% interest Boardwalk Pipeline Partners (transportation and storage of natural gas)

· 100% interest in Loews Hotels (luxury hotel operations)

· 99% interest in Altium (rigid plastics packaging manufacturer)

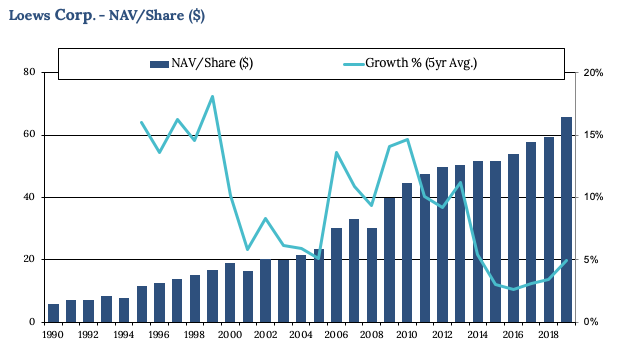

Given its holding company structure, one of the key metrics we look at to determine the success of management’s ability in generating shareholder returns is the growth in the Net Asset Value/share (NAV/share).

In the case of Loews, NAV/Share has been growing steadily over the long term and is now ~$60/share

Source: Bloomberg

Even if we use the market value of listed securities, rather than the book value, (which themselves are trading at a discount to NAV) Loews consolidated NAV is $50/share. Furthermore, within Loews we are buying a business alongside a very aligned family with a transparent strategy and strong track record.

Our process of using put options to enter stock positions means we are looking to buy Loews at $35/share, a level we believe has little downside from that position. So that leaves the upside. While the Hotels business won’t be delivering in the short term, the diversified nature of the business means other parts continue to perform and even increase their profitability. So a share price outcome in the mid/low $50 over the next few years is a realistic upside based on an expectation that Loews can continue growing Net Asset Value of ~7% p.a. while still applying a ~20% ‘holding company’ discount.

In short, we are buying a series of good quality assets at very attractive prices.

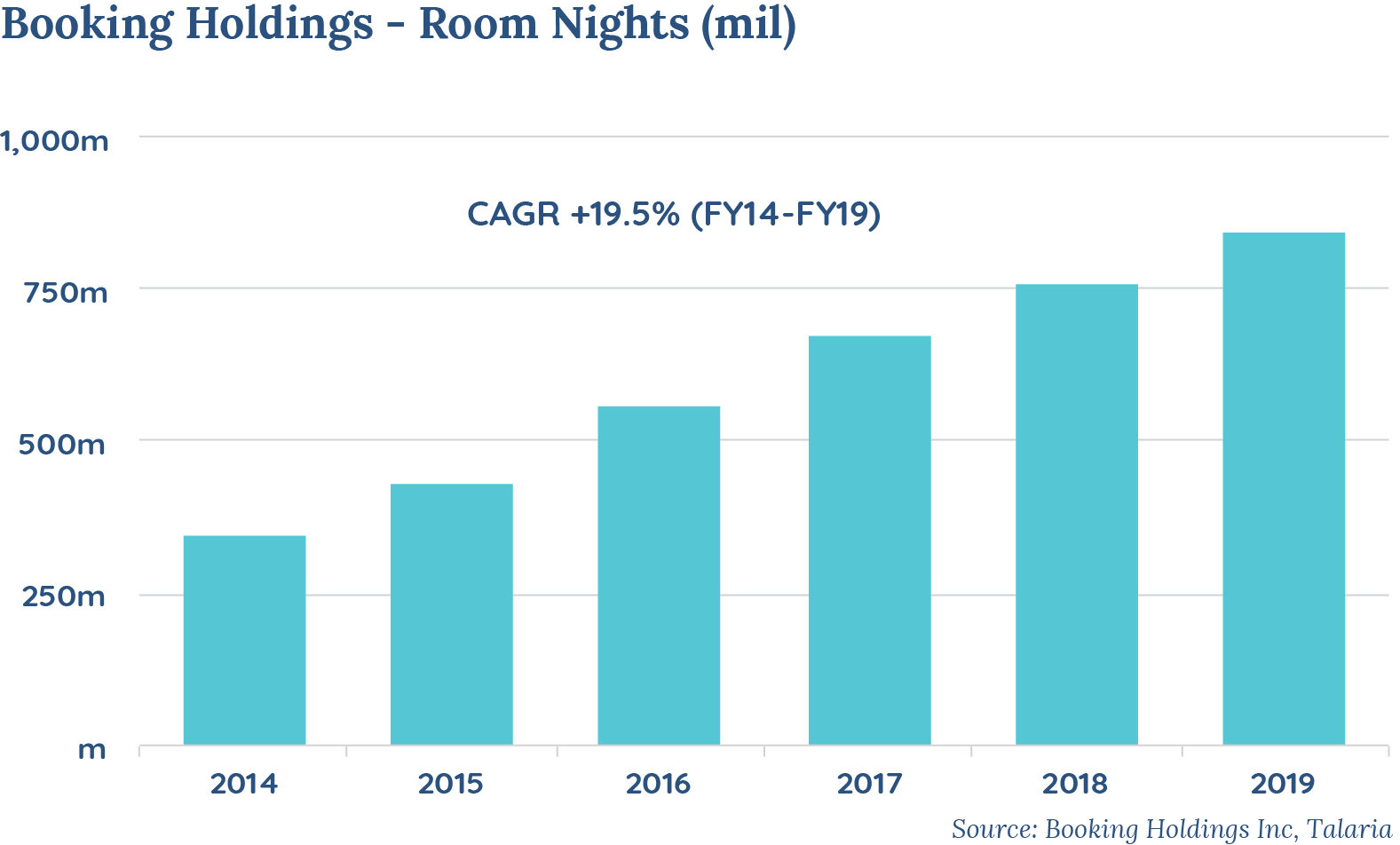

Another similar company is Booking Holdings. Booking has both driven and benefited from the move to online travel management. In 2019 they sold over 800 million room nights.

The business model is very profitable with Booking keeping approximately 15% of the room sale, a percentage that has been stable despite growing market share. This has allowed the company to earn operating margins of approximately 35%, which substantially flow through to cash given the very low capital requirements of the business.

The travel industry has been among the worst affected by COVID-19 and Booking has not been spared. Revenue this year will likely be down over 50% and profits closer to 80% lower. As expected, this has had a negative impact on the share price; with weakness providing an opportunity to get exposure to the stock at an attractive level.

In our assessment, the negative revenue impact will be transitory as the business model is very much viable. Furthermore, during the current challenging period, we expect weaker online and offline competitors to exit the industry, often through lack of scale and balance sheet weakness.

In terms of resilience, Booking has no net debt, and liquidity of US$14.5bn which compares to estimated ongoing costs of $6.9bn. This provides sufficient capital to operate for years, even if low activity were to persist. Approximately 60% of costs are variable and thus will fall in line with sales, and there is medium term flexibility on the remaining 40% of costs.

In June we placed options that agreed to buy Booking at approximately 15% below the then current price yet still generate around 20% annualised return. At our entry price we believe the shares offer up to 50% upside based on normalised earnings which we expect to be realised in the next three years.

With investing, as in life, it’s always nice to get something in return for the effort, so while Booking appreciated over 15% by the time our options matured, we still received the premium for taking it out.

These are just two examples of how we are paid for taking market risk.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Chad is the Co-Chief Investment Officer and co-founder of Talaria Asset Management. He has more than 21 years of experience in the financial services industry in the UK, South Africa and Australia. Talaria's investment strategy seeks to increase the certainty of global equity returns for investors through its:

> Unique and structurally lower-risk investment approach that combines capital growth and income generation to deliver a more consistent return profile (smoothing).

> Portfolio of up to 45 large, globally listed companies.

> Internationally experienced and personally invested leadership team.

www.talariacapital.com.au

........

The information in this article is general information only and is not based on the objectives, financial situation or needs of any particular investor. In deciding whether to acquire, hold or dispose of the product you should obtain a copy of the current Product Disclosure Statement (PDS) for the Fund and consider whether the product is appropriate for you.

Wholesale Units in the Talaria Global Equity Fund (the Fund) are issued by Australian Unity Funds Management Limited ABN 60 071 497 115, AFS Licence No. 234454. Talaria Asset Management Pty Ltd ABN 67 130 534 342, AFS Licence No, 333732 is the investment manager and distributor of the Fund. References to “we” means Talaria Asset Management Pty Ltd, the investment manager. A copy of the PDS is available at australianunity.com.au/wealth or by calling Australian Unity Wealth Investor Services team on 13 29 39. Investment decisions should not be made upon the basis of the Fund’s past performance or distribution rate, or any ratings given by a rating agency, since each of these can vary. In addition, ratings need to be understood in the context of the full report issued by the rating agency itself. The information provided in the document is current at the time of publication.

3 topics

Chad is the Co-Chief Investment Officer and co-founder of Talaria Asset Management. He has more than 21 years of experience in the financial services industry in the UK, South Africa and Australia. Talaria's investment strategy seeks to increase...

Expertise

Chad is the Co-Chief Investment Officer and co-founder of Talaria Asset Management. He has more than 21 years of experience in the financial services industry in the UK, South Africa and Australia. Talaria's investment strategy seeks to increase...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Why ex-20 is the prime hunting ground for ASX returns

Livewire Markets