Home Cooking and Value Investing - Why Careful Ingredient Selection and Patience Pays Off

Adrian Warner

Avenir Capital

Many would agree that the execution of a patiently prepared home-cooked meal with carefully selected ingredients is a rewarding endeavor. Pre-packaged takeaway is convenient, but is undesirable for many reasons, beyond any immediate satisfaction.

Trends in investing are similar. Indices are essentially investment shopping lists prepared by someone else that help save passive investors time and effort in deciding what to buy or give benchmark-aware fund managers a starting point to help decide what to put in their trolleys.

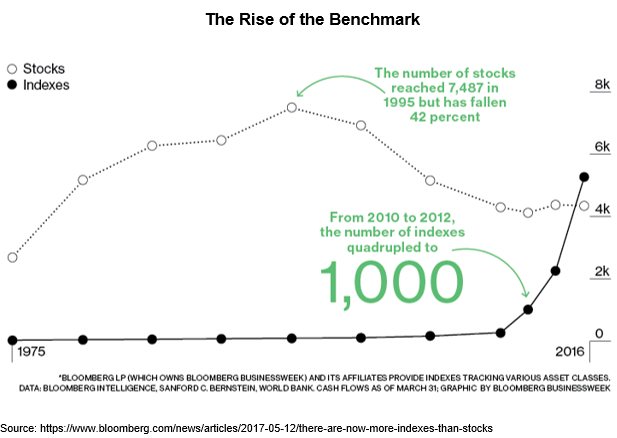

Changes in Investing Habits

Yet in 2017, the number of stock market indices exceeded the number of stocks in the US, expanding the proverbial supermarket of investment ‘takeaway’ offerings.

What does it say about our investment eating habits when the number of shopping lists starts to exceed the number of actual ingredients to buy? In our rush to embrace convenience, are we losing sight of selecting quality underlying ingredients and carefully preparing healthy, well balanced portfolios?

Many products in the new financial supermarket are built on the assumptions and ‘theories’ of markets - that humans make rational economic decisions and that price should always reflect the intrinsic value of the investment.

Yet humans, and therefore markets, are not perfectly rational, particularly in the short term.

The 2017 Nobel Prize for Economics, awarded to Richard Thaler, recognised this as much, acknowledging his research which demonstrated “…that, unlike members of homo economicus, members of the species homo sapiens make predictable mistakes because of their use of heuristics, fallacies, and because of the way they are influenced by their social interactions.” (1)

Thaler demonstrates that humans, particularly investors:

- rely too heavily on one trait or piece of information (anchoring),

- predict the frequency of an event based on how easily an example can be recalled (availability),

- judge probability of a theory by considering how much the theory resembles available data (representativeness),

- continue courses of action simply because that is how it has always been done (status quo), and

- are heavily influenced by the actions of others (herd mentality).

Holding Period Returns

Value investing, like cooking, should be an exercise in careful selection, patience and conscious avoidance of biases.

To this end, compelling research released last year from well-regarded active management academics Martijn Kremers and Ankur Pareek (2) looked at the relationship between holding period (duration), degree of ‘activeness’ and returns for US fund managers (3).

Kremers co-invented the concept of active share in 2009, which is now one of the pre-eminent ways of establishing whether an investment manager is a benchmark-hugger or takes high-conviction bets.

A great deal of prior literature has shown that the long-term net performance of active managers is roughly similar to, or worse than, that of benchmark returns - on average.

However, the authors find that Active Share, or the degree of difference between a fund’s holdings and its benchmark’s holdings, and the average holding periods of stocks in their portfolios, are key factors in determining the outperformance of both mutual funds and institutional portfolios.

Unfortunately, such managers are the exception, not the rule.

Among high Active Share mutual funds, those with patient investment strategies (average holding periods of more than two years) appear to generate average alpha of 2.05% per year in the study.

At the other end of the spectrum, irrespective of how dissimilar their portfolios are relative to their benchmarks, highly traded mutual funds with short stock holding periods underperform, with average annual net alpha of negative 1.44%.

What lesson should we take from this study? Active investors must have conviction and be patient. What is good for us takes time to prepare and is best savored, not devoured!

It thus comes as no surprise then, that the key to the success of high conviction, patient value investors is, funnily enough… valuation.

Valuations at time of entry remain key

According to Bank of America Merrill Lynch analysis from 1971 to today - valuations at the time of purchase have explained 80-90% of returns from the S&P 500 over a 10-year horizon (4). The research, ironically, comes from a major investment bank, whom as an industry has prospered on encouraging short-term trading.

True value investors should focus on valuation, rather than trying to keep up with the benchmark on a short-term basis as it maximises the chance of outperforming the market on a long-term basis.

This of course, is hard to justify to investment oversight committees where peer comparison and a natural human bias to immediate action prevails. As such, it is understandable why so much of the retail and institutional funds management industry trends towards career-risk driven mediocrity and hugs the benchmark. However, good investing, like good cooking, doesn’t benefit from having too many chefs in the kitchen.

Patience ultimately wins over the long term, as too many investors trade too frequently, do not properly anchor assessments of value in fundamental long-term reasoning, or fire their fund managers too quickly.

In the same way that cooking at home is harder and harder as we become more time poor, yet increasingly satisfying for the same reason, we believe patience and high conviction as sources of excess return is likely to persist due to the unchanging nature of human psychology.

We are optimistic that growing investor short-termism and passive investing trends may, in fact, provide high conviction active investors with some of their best opportunities in a long time.

At Avenir Capital, we like to carefully and patiently prepare our own investment cooking and we encourage all investors to consider doing the same.

By Sam Morris, Investment Specialist at Fidante Partners and Adrian Warner, CEO/CIO, Avenir Capital

For further insights from Avenir Capital, please visit our website

(1) Thaler, Richard H.; Sunstein, Cass R. (2008). Nudge: Improving Decisions about Health, Wealth, and Happiness, Yale University Press, p.7 (VIEW LINK)

(2) Cremers, M. and Pareek, A. (Nov 2016). Patient Capital Outperformance: The Investment Skill of High Active Share Managers Who Trade Infrequently, Journal of Financial Economics, Vol. 122, No. 2, pp. 288-306

(VIEW LINK)

(3) Sample set included a large sample of all-equity US retail mutual funds from the largest database of returns, the Centre for Research in Security Prices (CRSP), and a sample of all aggregated institutional investor US equity portfolios as inferred from their quarterly 13F statements over a 24 year period from 1990 to 2013 (Retail) and 1984 – 2012 (institutional).

(4) Bank of America Merrill Lynch (March 2017). Strategy Snippet: The most contrarian theme: long-term fundamental investing

(VIEW LINK)

The information in this article has been prepared on the basis that the Client is a wholesale client within the meaning of the Corporations Act 2001 (Cth), is general in nature and is not intended to constitute advice or a securities recommendation. It should be regarded as general information only rather than advice. Because of that, the Client should, before acting on any such information, consider its appropriateness, having regard to the Client’s objectives, financial situation and needs. Any information provided or conclusions made in this article, whether express or implied, including the case studies, do not take into account the investment objectives, financial situation and particular needs of the Client. Past performance is not a guide to future performance. Neither Avenir Capital (“Avenir”) (ABN 40 150 790 355, AFSL 405469), Fidante Partners Limited (“FPL”) (ABN 94 002 835 592, AFSL 234668) nor any other person guarantees the repayment of capital or any particular rate of return of the Client portfolio. Except to the extent prohibited by statute, neither Avenir nor FPL nor any of their directors, officers, employees or agents accepts any liability (whether in negligence or otherwise) for any errors or omissions contained in this article.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Adrian Warner is the Managing Director and Chief Investment Officer of Avenir Capital and is responsible for the portfolio management of the Avenir Global Fund. Prior to founding Avenir Capital, Adrian worked in private equity investment in Australia, Asia and the United States with an investment record spanning over 20 years.

2 topics

Adrian Warner

Chief Investment Officer

Avenir Capital

Adrian Warner is the Managing Director and Chief Investment Officer of Avenir Capital and is responsible for the portfolio management of the Avenir Global Fund. Prior to founding Avenir Capital, Adrian worked in private equity investment in...

Expertise

Adrian Warner

Chief Investment Officer

Avenir Capital

Adrian Warner is the Managing Director and Chief Investment Officer of Avenir Capital and is responsible for the portfolio management of the Avenir Global Fund. Prior to founding Avenir Capital, Adrian worked in private equity investment in...

Expertise

Comments

Comments

Sign In or Join Free to comment