House prices: as bad as they get?

The newly appointed deputy chair of the Australian Prudential Regulation Authority (APRA) talking at a FINSIA conference last month said that APRA’s “stability measures” - in other words their restrictions on bank lending introduced last year - have helped prepare the Australian economy for “an unseasonable cold snap”. Really?

APRA are perhaps ignoring the fact that rather than prepare Australia for a "cold snap" they may in fact have caused it.

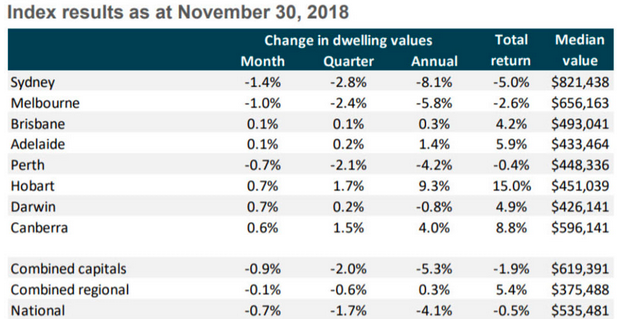

Here is a table of house prices from CoreLogic as at the end of November. Sydney house prices have been down 8.1% in the last year, Melbourne House price is 5.8%. Melbourne and Sydney between them account for 55% of the value of Australia’s houses. The national annual fall in house prices in capital cities is down 5.3% in the last year.

The fall in the housing market in Sydney of 8.1% is the steepest since May 1983. Since the peak month in July last year the Sydney housing market is down 9.5%. The “peak to trough” decline at 9.5% is about as bad as it gets, the record was 9.6% between 1989 and 1991. The peak to trough fall in Melbourne house prices has been 5.8%.

The house price fall which has led to a marked drop in clearance rates could possibly be blamed on an increase in housing supply, slowing demand and a reduction in foreign buying activity, but the most significant factor leading to the house price decline has clearly been the tightening in finance lending regulation imposed by APRA.

The target of that regulation was clearly the frothy end of the investment market, but the result has been an almost record destruction of the core of the housing market risking or causing the “unseasonable cold snap” that APRA rather laughably suggests they were helping prepare for. Surely APRA caused it.

There has been some commentary in the last couple of weeks about how the Australian economy, tied as it is to the housing market, now risks recession because of the housing market. But that is the cart before the horse. It should be the other way around as it was in 1989 to 1991 when we saw similar levels of house price depreciation. The recession caused the record house price decline - now the suggestion is that the record house price decline will cause a recession.

But the Australian economy is cracking along - the RBA said in their recent minutes “GDP growth is expected to be around 3½ per cent on average over 2018 and 2019…growth would be supported by accommodative monetary policy, above-trend growth in Australia's major trading partners and a stronger profile for the terms of trade. Year-ended GDP growth was expected to ease to around 3 per cent towards the end of 2020 because LNG exports were expected to reach capacity production levels by the end of 2019.”

In the eyes of the RBA it seems, we have to worry about LNG exports rather than the housing market.

The result is that our economic concerns are overdone.

Prompted by the US "slowing growth" theme everybody has been feeding the recession narrative in the last week, which is of little value - I do hate the way commentators seeking clicks slot in behind the most clicked theme in the very short term and promote it mercilessly while ignoring the fact that they failed to predict it.

The more optimistic interpretation is that if you look at the “peak to trough” decline in house prices, particularly in Melbourne and Sydney, then this is not only about as bad as it gets, but it has also overshot considering we are not in recession and are unlikely to drop into recession as we were the last time house prices fell this much. As I say, shouldn’t the recession come first?

The bottom line is that the regulator has prematurely killed the housing market.

Combined with the Royal Commission they have paralysed the bank sector, slowed down lending rates and damaged the housing market. If they were looking to blow the froth of the investment market and off the international interest in the Australian market, they have gone too far.

The RBA (who are not APRA) acknowledged the damage in their recent minutes saying “Conditions in the Sydney and Melbourne housing markets had continued to ease, following significant growth over preceding years. Credit conditions were tighter than they had been for some time, partly because lending standards had been tightened following the introduction of supervisory measures to help contain the build-up of risk in household balance sheets.”

The economy meanwhile, rather than heading into recession, is fine, and with the economy in fine fettle, it won’t take much to rescue the housing market and fend off an “unseasonable cold snap” as described/caused by APRA. All it will take is for the RBA to pass the message to APRA to pass the message to the banks to “get on with it” again, to loosen lending requirements, get loan applications down from 6 to 8 weeks back to 2 to 3 weeks, and this housing market will rapidly recover, as it always has from this level of depreciation.

My advice is not to go making any big decisions about the housing market or the Australian economy. Rather than the housing market dropping into a hole and the economy dropping into recession, the chances are that this is the bottom of the house price decline - that house price growth is as bad as it gets. With house price growth as bad as it’s ever been since the last recession, without a recession, this is not the beginning of the end, it is an opportunity.

Predictions for 2019 are a popular theme this month, let me give you three:

- House prices bottom.

- The Australian economy doesn’t come close to negative growth for one quarter let alone two.

- The RBA will not need to cut rates.

Did you enjoy that?

Marcus Padley is the author of the Marcus Today stock market newsletter. To sign up for a 14-day free trial please click here.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Marcus Padley founded Marcus Today in 1998 and leads the team of analysts and market commentators that publishes a daily stock market newsletter, presents four podcasts and runs an $80m Australian equity fund. He is passionate about educating and informing private investors with insightful, honest, straight-up independent stock market research and ideas. Marcus likes to call it as it is without agenda, puts subscribers first, and this has paid off for real people with real money.

1 topic

Marcus Padley founded Marcus Today in 1998 and leads the team of analysts and market commentators that publishes a daily stock market newsletter, presents four podcasts and runs an $80m Australian equity fund. He is passionate about educating and...

Expertise

Marcus Padley founded Marcus Today in 1998 and leads the team of analysts and market commentators that publishes a daily stock market newsletter, presents four podcasts and runs an $80m Australian equity fund. He is passionate about educating and...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Funds

The 5 best-performing super funds of the year

Livewire Markets

Equities

Buy Hold Sell: 5 ASX stayers built to go the distance

Livewire Markets