How much, and when the RBA will cut interest rates in 2025

Yesterday’s RBA meeting showed a marked dovish tilt in language, causing markets to reel in expectations for the first interest rate cut.

The Reserve Bank of Australia (“RBA”) concluded its December 2024 meeting by maintaining its official cash rate (“OCR”) at 4.35%, marking the ninth consecutive meeting and the thirteenth consecutive month at this level. This was not the headline, however – this is exactly what the market expected.

Despite the seemingly benign outcome, there were some massive moves in markets post-meeting, and equally large changes in the expectations surrounding the timing and magnitude of RBA interest rate cuts in 2025. A picture tells a thousand words, so let’s check out some of the moves the decision triggered across markets in charts:

Exhibit 1: Massive plunge in key risk-free market yield benchmarks

The benchmark for short term Australian government bond yields, the 2-Year bond, fell by 12 basis points to 3.77%. Markets effectively delivered half a typical interest rate cut (i.e., 0.25%) immediately following the December Board meeting.

Exhibit 2: Big drop in the Australian dollar

The Australian dollar fell 1%, reaching approximately 63.75 US cents, its lowest level in over a year. Currency values are all about relative risk-free returns across countries. If markets anticipate they will earn a lesser yield in Australia (because of increased official interest rate cuts) compared to the USA, they will sell down the Australian dollar in favour of the higher yielding US dollar.

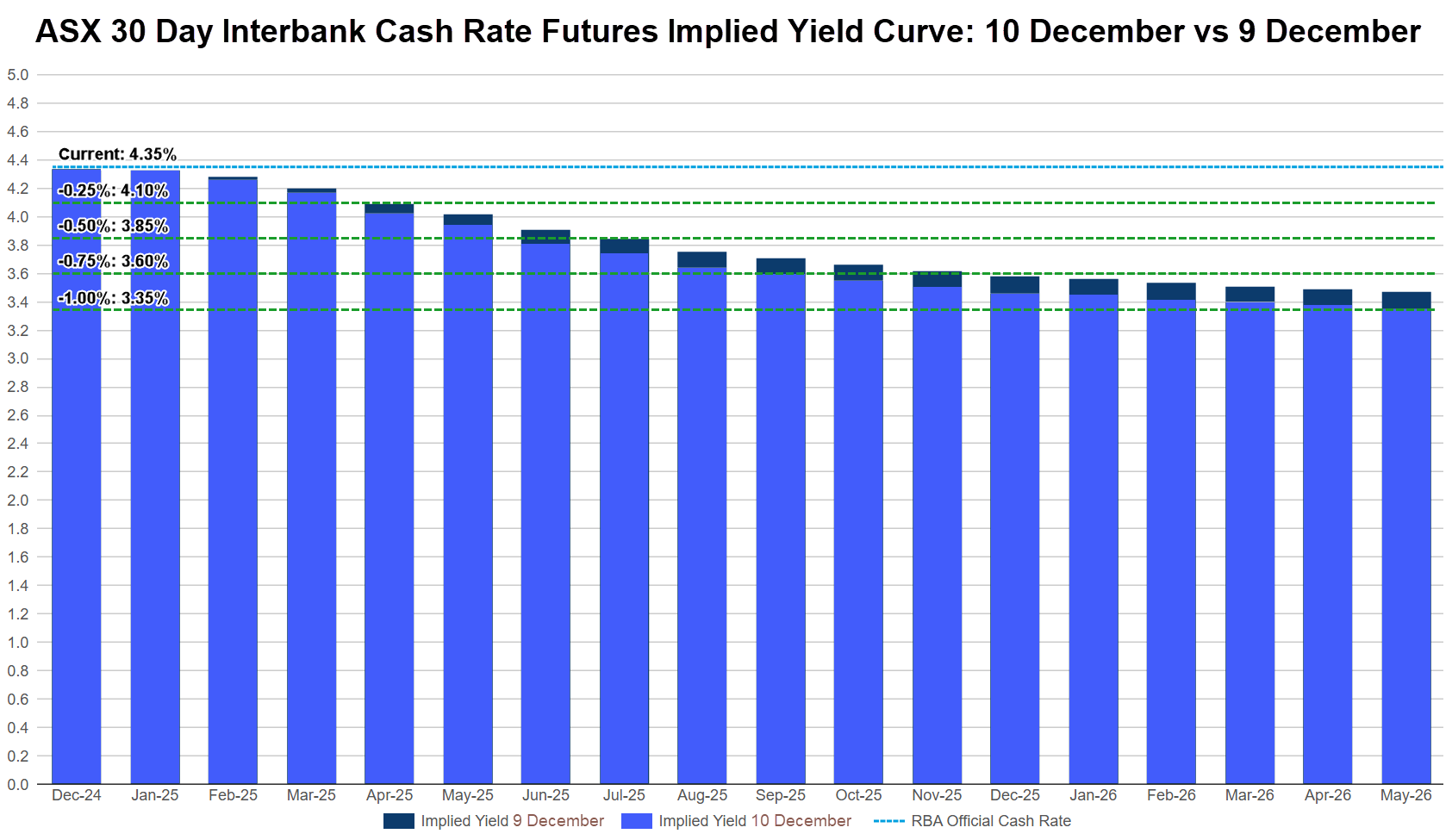

Exhibit 3: Dip and draw in the Implied Yield Curve

The ASX 30 Day Interbank Cash Rate Futures Implied Yield Curve is a market proxy for the RBA’s OCR. The Yield Curve provides investors with a graphical representation of where the market is predicting the OCR will be down the track.

I have overlaid the December 10 Yield curve (light blue bars) over the December 9 curve (dark blue bars) to illustrate the change in market expectations for the timing and magnitude of RBA interest rate cuts both before and after the December Board meeting. I’ve also drawn on the schedule levels equating to the next 1.0% of 0.25% cuts.

Generally, the market has lowered its expected level of the OCR through the 18 month look-forward period. Where the light blue bars touch an interest rate cut level tells you when the market has fully factored in the relevant cut.

In terms of first cut timing, the curve has experienced the following notable changes:

- The next RBA meeting is 5-6 February, the chance of an interest rate cut at this meeting has increased from 28% to 34%

- March meeting cut probabilities increased from 60% to 72%

- There is no meeting in April, but this is when the market is factoring the first rate cut (interpret this as hedging their bets between the March and May meetings!) The interesting item here is that the probability of a larger, 0.5% cut, increased from just 6% to 28%.

- The second 0.25% rate cut has moved in from July to June.

- The third 0.25% rate cut has moved in from December to September.

- There was no fourth 0.25% rate cut in the Yield Curve’s look forward period ending May 2026, but there’s now a 98% probability it will occur in that month

In summary, markets believe the first RBA interest rate cut is a lock by May next year, but the probability of a surprise March cut has increased. Mortgage holders are still likely to get three 0.25% cuts in 2025, but they are likely to occur three months earlier by September. There is now a fourth cut in the mix by May 2026.

Why did markets react so vigorously to the December RBA meeting?

Here are the key takeaways from the December meeting statement and post-meeting press conference by Governor Michelle Bullock that caused the market to pivot so substantially:

Statement

- Expressed "gaining some confidence that inflation is moving sustainably towards its target", this a departure from previous assertions about the necessity of maintaining restrictive policies.

- Omitted earlier references to being vigilant against upside risks to inflation and the commitment to keeping policy sufficiently restrictive until confident of inflation's trajectory.

- Added references to weakening Australian economic growth, "While underlying inflation is still high, other recent data on economic activity have been mixed, but on balance softer than expected in November", in particular citing the worse than expected September quarter GDP figures, noting it was "the slowest pace of growth since the early 1990s".

- Added the statement: "Wage pressures have eased more than expected in the November SMP." – again, arguably dovish.

- Replaced "But there are uncertainties" with "Some of the upside risks to inflation appear to have eased and while the level of aggregate demand still appears to be above the economy’s supply capacity, that gap continues to close."

Press conference

- “Some indicators softening in line with our forecasts, that said, on balance, some data is a little softer than expected. This has given the Board some confidence that inflationary pressures are declining, but risks remain.”

- Which data? “The national accounts data weren’t as strong as expected, the Wages Price Index came a little bit lower than what we thought it might be, inflation data were broadly in-line. It’s not only slowing as we’d like, it’s slowing a little-bit more and that’s positive for inflationary pressures…it’s giving us confidence we’re coming on our narrow forecast path.”

- “Some of those risks to upside inflation have eased. We have noticed [the weaker data] and we do need to take a bit of a signal from that, but upside risks remain.”

Conclusions

In summary, the RBA's December meeting maintained the current cash rate but signaled a marked shift towards a more accommodative stance. Markets are now anticipating potential rate cuts to occur sooner and to a greater magnitude in early 2025. The news is arguably positive for mortgage holders, and also likely, for stocks which also tend to benefit from lower official interest rates.

If there is a group of losers out of the developments of the last 24-hours, it's likely to be those with cash in the bank. It might be time to think about locking in those higher deposit rates while you still can!

This article first appeared on Market Index on Wednesday 11 December 2024.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl has a passion for technical analysis and has taught his unique brand of price-action trend following to thousands of Aussie investors.

........

Investing is risky. Inevitably you will endure losses. If you can't cope with losing, don't invest.

{kind=link}

{kind=link}

5 topics

7 stocks mentioned

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl...

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl...

Comments

Comments

Sign In or Join Free to comment