TOL - 18th Apr, 2024

How the #1 picks for 2024 are tracking (and the stock up 67%)

It's been a positive quarter for both the All Ordinaries Index and our fundie picks.

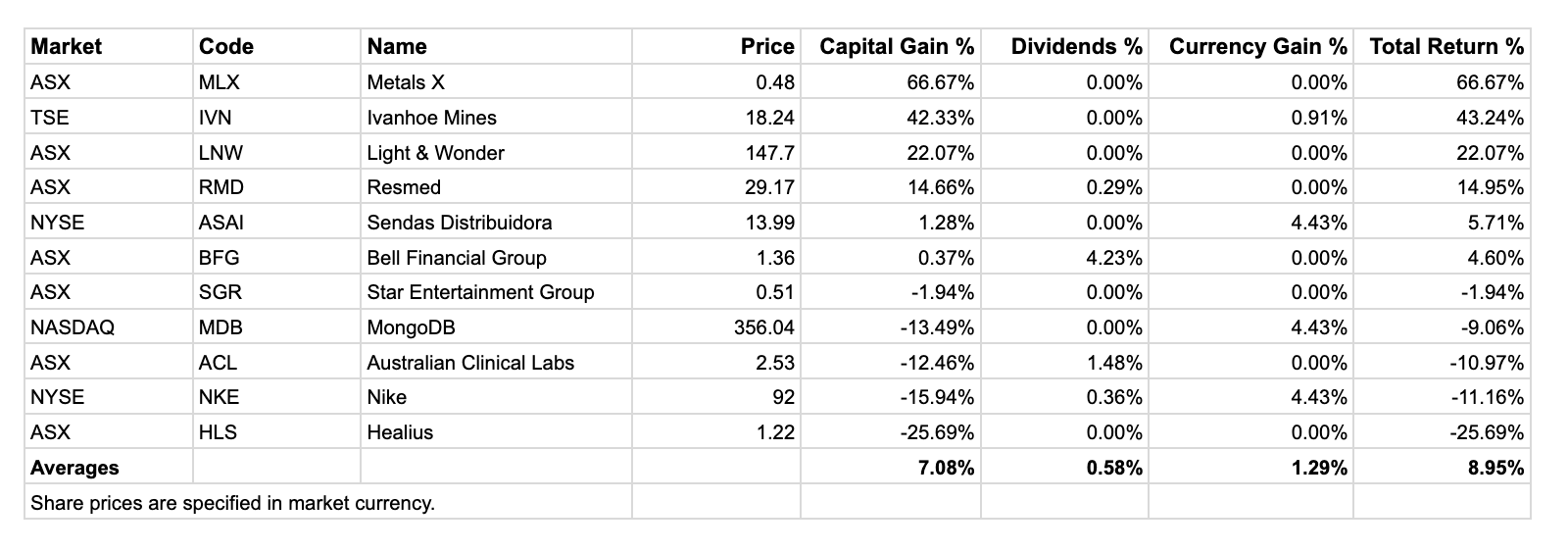

Since the beginning of the year, the #1 stock picks for 2024 have outperformed the All Ordinaries Index, with the portfolio of 11 stocks delivering an average return of 8.95%. The All Ords, in comparison, has lifted 2.32%.

It's a pretty solid return, but one that hasn't beaten the surge in US markets - with the S&P 500 up 9.62% year to date.

Six out of the 11 stocks have delivered positive returns so far in 2024, while five are in the red. Four stocks have delivered double-digit returns - with the clear winner, so far, lifting a whopping 67%.

Advertisement

There's a clear theme among the winning stocks, with the list's two strongest performers being the only two resources stocks of the bunch. Interestingly, among the three poorest-performing stocks are two pathology players.

In this wire, I'll summarise how the #1 stock picks for 2024 are tracking so far, with commentary from some of the fundies who participated in the series.

Please note: The information in this wire is not, nor is it intended to be, a set of recommendations. Please do your own research and seek advice from a professional. While quarterly performance data might make for interesting reading, for many of these products, performance should be considered over longer periods. Past performance is not a reliable indicator of future return.

The performance of the #1 stock picks from 2 January to 12 April 2024.

#1. Metals X (ASX: MLX)

- YTD Total Return: 66.67%

- Fund manager: Joel Fleming

- Firm: Yarra Capital Management

As Fleming explains, the investment case for tin producer Metals X centres on two key factors: optimism regarding the outlook for tin prices and the company's low valuation metrics, which offer substantial leverage to this rising commodity price.

"The performance year-to-date has validated the thesis, with the spot tin price up 22.6% YTD in USD (and even more in AUD terms), coupled with the commencement of capital management through an on-market buyback," he told Livewire.

And there's more where that came from, with Fleming arguing that there is still "significant" potential for growth given the tin market's supply and demand conditions.

"The business is expected to generate strong cash flow and has additional growth opportunities, particularly with further drilling prospects at Ringrose. The increased market capitalisation also provides access to a wider audience of potential investors," he added.

#2. Ivanhoe Mines (TSE: IVN)

- YTD Total Return: 43.24%

- Fund manager: Daniel Sullivan

- Firm: Janus Henderson

Similarly, Copper prices have strengthened recently, moving from a $3.60-$4.00/lb range in the past year to $4.28/lb.

"Ivanhoe Mines have successfully built and operated their key copper project at Kamoa-Kakula, and continue to develop their zinc, platinum and exploration projects," Sullivan said.

"Investment thesis intact, more growth is expected later this year with the Phase 3 copper concentrator project coming online."

#3. Light & Wonder (ASX: LNW)

- YTD Total Return: 22.07%

- Fund manager: Chris Stott

- Firm: 1851 Capital

Light & Wonder has also had a fantastic start to the year, with Stott arguing the stock's share price has been driven by the outperformance within its gaming operations division - notably, by its new game "Dragon Train".

"This game is taking significant market share in Australia and is showing very good early signs in the USA market," Stott said.

"We believe the share price can continue to trade higher driven by further new game releases and continued increases in market share."

#4. ResMed (ASX: RMD)

- YTD Total Return: 14.95%

- Fund manager: Emma Fisher

- Firm: Airlie Funds Management

ResMed continues to rebound from its lows, with the stock up nearly 15% in 2024 so far, and up more than 38% since hitting lows late last year on negative news surrounding the popularity of Novo Nordisk's Ozempic and other weight-loss/diabetes drugs.

In January, ResMed beat analyst estimates on both revenues and operating income. Non-GAAP gross margins also surprised to the upside, increasing by 90 basis points (bps) quarter on quarter to 56.9%.

#5. Sendas Distribuidora (NYSE: ASAI)

- YTD Total Return: 5.71%

- Fund manager: Vihari Ross

- Firm: Antipodes

Sendas Distribuidora is in the black but has underperformed the US market in 2024. The stock is scheduled to report its first-quarter results on April 25. In March, management reported its Q4 2023 results, beating analyst estimates on earnings per share but missing revenue estimates by 6.6%.

#6. Bell Financial Group (ASX: BFG)

- YTD Total Return: 4.60%

- Fund manager: Matthew Kidman

- Firm: Centennial Asset Management

Bell Financial Group, the parent company of Bell Potter Securities, Bell FX, Bell Potter Capital, Bell Direct, Desktop Broker, Bell Potter Online and Bell Direct Advantage, is also in the black in 2024 and has outperformed the All Ordinaries Index. It has underperformed the Small Ordinaries, though, which has lifted 6.53% year to date.

In February, Bell Financial Group's FY NPAT came in under analyst expectations, while its revenues beat estimates by 26.4%.

#7. Star Entertainment Group (ASX: SGR)

- YTD Total Return: -1.94%

- Fund manager: Matthew Haupt

- Firm: Wilson Asset Management

It's been a volatile ride for Star Entertainment shareholders in 2024, with the stock's share price diving nearly 26% in February on the announcement that the New South Wales casino regulator would undertake a second investigation into its Sydney casino operations.

Over the past 12 months, Star Entertainment's share price has fallen nearly 60%.

#8. MongoDB (NASDAQ: MDB)

- YTD Total Return: -9.06%

- Fund manager: Francyne Mu

- Firm: Franklin Templeton

Database management software provider MongoDB has had a volatile start to 2024, with the stock initially one of the best performers on the list before being sold off in February. That may be because MongoDB insiders have been selling off millions of dollars worth of shares in the company all year.

That said, the majority of the analysts who cover the stock still rate it as a buy. The stock has an average price target of US$449.20, which could indicate a 26.17% rise from here.

#9. Australian Clinical Labs (ASX: ACL)

- YTD Total Return: -10.97%

- Fund manager: Marc Whittaker

- Firm: IML

ACL, which is one of three national pathology operators in Australia, has sunk into the red in 2024, after already performing poorly in 2023.

While Whittaker notes that ACL's February reporting update was less positive than the team would have liked, the reasons why they backed the stock for the Outlook Series remain intact.

"Australia’s ageing population ensures ongoing growth in testing volumes, as older people are more likely to have health issues requiring regular monitoring. The number of conditions able to be assessed by pathology testing continues to grow, also underpinning growth in volumes," he said.

"These factors have seen industry testing volumes grow 5% p.a. over the past three decades. However, recent “business as usual” volumes have been slower to recover to trend than expected due to doctor shortages and cost of living pressures."

These remain issues in the short term, Whittaker adds, but growth rates are likely to return to trend over time.

"ACL has a strong balance sheet with minimal debt, providing scope for further bolt-on acquisitions in an industry that will see further consolidation over time," he said.

"The synergies from any potential acquisition could be significant, making any future transaction very attractive. Trading on only 12.2 times FY25 earnings and a yield of over 6%, ACL remains very attractively priced and we have continued to add to our position."

#10. Nike (NYSE: NKE)

- YTD Total Return: -11.16%

- Fund manager: Mary Manning and Bob Desmond

- Firm: Alphinity Investment Management and Claremont Global

Nike recently released its third-quarter 2024 earnings result, with revenues and earnings per share beating analyst estimates. Bank of America lifted its price target on the stock to $113 from $110 and upgraded it to a Buy from Neutral, arguing estimates for earnings were bottoming and that the Olympics could be a catalyst.

"Nike is taking bold steps to transform, and the stock sits at a 10-year trough relative P/E... Consensus estimates for FY25 dropped 35% over the past two years and the multiple is 10 points below its five-year average," analysts at Bank of America said.

The majority of analysts rate the stock a buy, with an average price target of US$111.70, indicating a 21.45% upside from here.

#11. Healius (ASX: HLS)

- YTD Total Return: -25.69%

- Fund manager: Dr Philipp Hofflin

- Firm: Lazard Asset Management

Healius is Australia's second-largest private pathology company, with a "large market share in a defensive, consolidated and usually profitable industry," Hofflin said.

The company's 75% fall in share price since 2022 "enabled us to buy a business in a good industry at a depressed price, but it has not yet delivered the turnaround we expected in 2024," he added.

Hofflin believes there are four catalysts that could see the stock's fortunes turn around in 2024, including:

- Self-help, as new management lowers costs in pathology that rose too far during COVID.

- Government regulations, with significantly increased GP reimbursement rates to restore bulk billing rates. More bulk billing leads to more GP visits and testing.

- The government is being urged to re-introduce pathology reimbursement indexing in the May budget, to keep pathology bulk billed. Any adjustment would be very positive for profitability.

- The company is considering various corporate M&A options.

Hofflin believes the stock remains attractively priced and revealed that Lazard had been a net buyer in 2024.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Welcome to Livewire, Australia’s most trusted source of investment insights and analysis.

To continue reading this wire and get unlimited access to Livewire, join for free now and become a more informed and confident investor.

Already have an account? Sign in here

Advertisement

This article is for members only

Join Free to unlock all exclusive content

To continue reading and gain unlimited access to all Livewire content, join free to become a more informed, confident investor.

Already have an account? Sign in

This is an archived profile. Ally Selby was with Livewire Markets from 2020 to December 2024.

........

Livewire gives readers access to information and educational content provided by financial services professionals and companies (“Livewire Contributors”). Livewire does not operate under an Australian financial services licence and relies on the exemption available under section 911A(2)(eb) of the Corporations Act 2001 (Cth) in respect of any advice given. Any advice on this site is general in nature and does not take into consideration your objectives, financial situation or needs. Before making a decision please consider these and any relevant Product Disclosure Statement. Livewire has commercial relationships with some Livewire Contributors.

Heavy Hitters, Big Calls, Bold Predictions, Top Stocks

Switch to CommSec. Get up to 100 trades brokerage-free

Get up to 100 trades brokerage-free when you switch to CommSec and transfer a min. $10,000 in shares from another broker. Limited time offer.

Disclaimer: Min. investment amount, T&Cs, other fees and charges and eligibility criteria apply. New customers only.

DOWNLOAD THE FREE EBOOK FROM

The Ultimate Investing Guide for 2025

Livewire has handpicked a selection of investment experts for their outlook for the year ahead.

DOWNLOAD THE FREE EBOOK FROM

The Ultimate Investing Guide for 2025

Livewire has handpicked a selection of investment experts for their outlook for the year ahead.

2 topics

10 stocks mentioned

12 contributors mentioned

This is an archived profile. Ally Selby was with Livewire Markets from 2020 to December 2024.

Expertise

This is an archived profile. Ally Selby was with Livewire Markets from 2020 to December 2024.

Expertise

Comments

Comments

Sign In or Join Free to comment

D

David Hannell

Ten stocks over four exchanges for a 8.9% return. Compare with the VanEck ETF "QUAL".. One stock, one exchange for 14.5% return ytd. I know which one is easiest to manage.

most popular

Equities

Investing for the biggest market shift since the GFC

Livewire Markets

Equities

Why ex-20 is the prime hunting ground for ASX returns

Livewire Markets