TOL - 9th Dec, 2020

How to earn higher income for lower risk

When it comes to liquidity, Australian investors think inconsistently across their portfolios, especially in relation to where they source income. While most are typically comfortable buying a residential investment property to generate a modest yield (accompanied by high transaction costs), they’re often hesitant to deploy their capital into a locked-up vehicle that targets yields and income up to 2-3 times more than the current rental yield.

With short-term interest rates remaining at 0.10%, or lower, in 2021 and well beyond, and term deposit rates not that much higher, we believe 2021 is the year to begin capturing the illiquidity premium offered within sub-sectors of the global credit markets.

Why should investors consider adding illiquid assets to their portfolios?

In order to earn a return above the risk-free rate (0.10%), by definition, investors must take risk. These risk premiums include: equity risk premium, term risk premium, credit risk premium and illiquidity premium. When constructing the core components of an actively-managed diversified portfolio, the first three risk premiums are typically accounted for, but the illiquidity premium is often overlooked.

The illiquidity premium is essentially the additional compensation to investors for limiting their ability to take advantage of future market dislocations should they arise as their capital is locked up for a specified period. As a result, illiquid investments should offer a premium in the form of higher yield expectations. These comparably higher yields can be a helpful income-generating component of a portfolio. (It could be argued that to some extent residential investment property represents this illiquid component in portfolios given that investors are making a multi-year capital commitment, but unfortunately the current low rental yield provides little compensation.)

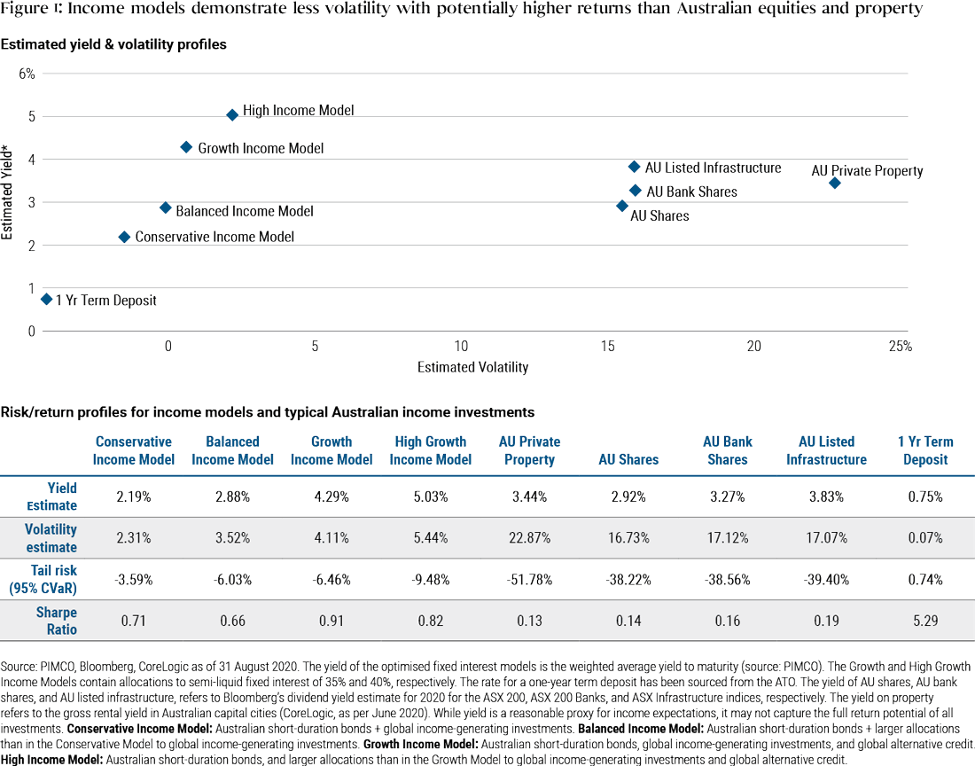

Combining both liquid and less-liquid income-generating alternatives in a portfolio, such as in the High Income Model we discussed in a recent article, is one way of capturing some of this illiquidity premium.

In this research, we analysed a number of potential income models that comprise a range of fixed income investments that cater to varying risk tolerances. Each was optimised and stress-tested using our proprietary risk analytics infrastructure. The High Income Model comprised Australian short-duration bonds, global income-generating investments, and modest allocations to global alternative credit in order to capture some illiquidity premium. In this case, alternative credit investments referred to financing provided to borrowers that either require non-standard, customized terms, or are private in nature because the issuer cannot access public credit markets, making these investments sit on the more illiquid end of the investing spectrum.

For investors prepared to have some of their portfolio allocated to less liquid assets, our analysis estimates that by investing in a high income portfolio, they could achieve expected total returns greater than 5% (see Figure 1). This is higher than our return estimate for Australian equities, yet demonstrates only a third of the volatility and a quarter of the left tail risk as Australian equities or property investments.

Why focus on the illiquidity premium in 2021?

Now more than ever, investors need to consider all of the available risk premiums when building an efficient portfolio for their future. This may mean a number of things, including boosting diversification and taking advantage of unique opportunities caused by the current dislocations in areas like alternative credit.

In our view, alternative credit currently looks extremely attractive on a relative basis. Central banks have been supporting the most liquid, traditional areas of capital markets. A lot of that liquidity hasn't found its way into the less liquid, alternative areas of credit markets such as private corporate debt or real estate opportunities.

Importantly, investing in alternative credit requires intense bottom-up research and expertise in areas such as commercial and residential real estate, direct lending and distressed investing. Fund manager selection is therefore key: Funds need to be appropriately sized and managers experienced and well-resourced to target these opportunities.

One thing investors can't ignore in 2021

The above wire is part of Livewire's exclusive series titled "The one thing investors can't ignore in 2021." The series will culminate in the release of a dedicated eBook that will be sent to readers on Monday 21 December. You can stay up to date with all of my latest insights by hitting the follow button below.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Robert co-oversees the portfolio management teams in Asia. Previously, he was a portfolio manager in Munich and head of the European investment grade corporate bond team. He has 35 years of investment experience.

........

Livewire gives readers access to information and educational content provided by financial services professionals and companies ("Livewire Contributors"). Livewire does not operate under an Australian financial services licence and relies on the exemption available under section 911A(2)(eb) of the Corporations Act 2001 (Cth) in respect of any advice given. Any advice on this site is general in nature and does not take into consideration your objectives, financial situation or needs. Before making a decision please consider these and any relevant Product Disclosure Statement. Livewire has commercial relationships with some Livewire Contributors.

Past performance is not a guarantee or a reliable indicator of future results.

All investments contain risk and may lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and low interest rate environments increase this risk. Reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Inflation-linked bonds (ILBs) issued by a government are fixed income securities whose principal value is periodically adjusted according to the rate of inflation; ILBs decline in value when real interest rates rise. Treasury Inflation-Protected Securities (TIPS) are ILBs issued by the U.S. government. Equities may decline in value due to both real and perceived general market, economic and industry conditions. Commodities contain heightened risk, including market, political, regulatory and natural conditions, and may not be appropriate for all investors. The value of real estate and portfolios that invest in real estate may fluctuate due to: losses from casualty or condemnation, changes in local and general economic conditions, supply and demand, interest rates, property tax rates, regulatory limitations on rents, zoning laws, and operating expenses. Mortgage- and asset-backed securities may be sensitive to changes in interest rates, subject to early repayment risk, and their value may fluctuate in response to the market’s perception of issuer creditworthiness; while generally supported by some form of government or private guarantee, there is no assurance that private guarantors will meet their obligations. Investing in foreign-denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Currency rates may fluctuate significantly over short periods of time and may reduce the returns of a portfolio. Private credit and equity strategies involve a high degree of risk and prospective investors are advised that these strategies are appropriate only for persons of adequate financial means who have no need for liquidity with respect to their investment and who can bear the economic risk, including the possible complete loss, of their investment. Management risk is the risk that the investment techniques and risk analyses applied by PIMCO will not produce the desired results, and that certain policies or developments may affect the investment techniques available to PIMCO in connection with managing the strategy.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice.

Stress testing involves asset or portfolio modeling techniques that attempt to simulate possible performance outcomes using historical data and/or hypothetical performance modeling events. These methodologies can include among other things, use of historical data modeling, various factor or market change assumptions, different valuation models and subjective judgments.

Charts and data have been provided for illustrative purposes and are not indicative of the past or future performance of any PIMCO product. Charts may not be to scale and users should take this into consideration when conducting analysis.

This presentation contains the current opinions of the manager and such opinions are subject to change without notice. This presentation has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this presentation may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark or registered trademark of Allianz Asset Management of America L.P. in the United States and throughout the world. ©2020, PIMCO.

1 topic

Robert co-oversees the portfolio management teams in Asia. Previously, he was a portfolio manager in Munich and head of the European investment grade corporate bond team. He has 35 years of investment experience.

Expertise

Robert co-oversees the portfolio management teams in Asia. Previously, he was a portfolio manager in Munich and head of the European investment grade corporate bond team. He has 35 years of investment experience.

Expertise

Comments

Comments

Sign In or Join Free to comment