TOL - 19th Jan, 2021

How to play the great EV boom

With apologies to George W. Bush^ for the title of our note, sometimes it is easy to underestimate how quickly, ‘slow’ and ‘consistent’ foundational change is occurring. A bit like the old adage of boiling the frog, steady small changes can often go unnoticed (frog doesn’t notice small gradual increases in water temperature) until the cumulative impact of this imperceptible change suddenly results in seismic shifts (the frog dies).

We believe this may be a good descriptor for what has been happening in the battery and EV (electric vehicle) sectors over the past 5-7 years. Small incremental improvements in EV and battery technology combined with incremental setbacks for ICE (internal combustion engine) vehicles, such as Dieselgate and tighter emission targets, may have gone somewhat unnoticed by markets until recently. These improvements have resulted in a fast approaching tipping point where we believe a more rapid take up of EVs takes place. This may occur much faster than perhaps markets have been expecting, if this year’s rise in Tesla’s share price is any indication.

Very much like we saw with mobile phones, EV’s have advanced greatly. Whilst the initial mobile phone adoption seemed to be incredibly slow, still below 1% even a few years after launching during the early 80’s (think Michael Douglas in the original Wall Street movie with his Motorola DynaTAC 8000x analogue mobile phone). In the mid 90’s penetration continued to be low at about 10%.

At the start of the new millennium, penetration was still only around 30%. Today there are almost 300 million US mobile phone subscribers (90% penetration). These phones not only make phone calls but can also text and most incredibly for smart phones they can in an instant deliver you the cumulative knowledge of all mankind right into the palm of your hand. Plus, today it is not just people that have mobiles but also machines. The number of mobile devices used in machines (the ‘Internet of Things’) is now at multiples of the population.

We believe the same dynamic is now underway with EVs. The comparison with EV's is stark:

Here’s a link to a review of the Tesla Model X by an avowed petrol head (Jeremy Clarkson – Grand Tour). Warning – some may take offence to a few things Clarkson says or draws in this video!

Tesla just reported that it sold almost 500,000 cars in calendar year 2020 (+36% year-on-year). It exited the year at an annual run rate of >700,000 cars p.a. (based on Q4 sales). For context, it exited 2012 at only 20,000 cars p.a., thus massive growth over the past three quarters of a decade.

Does this growth justify today’s US$770 billion market valuation for the company? Hard to say, but perhaps it reflects the market’s increasing view that EV’s will relegate ICE vehicles to the same historical dustbin as that of the horse and buggy and landline phone.

Besides the current stratospheric Tesla share price, there is clearly broad and significant momentum in this structural megatrend, specifically the move to electric transport (and also renewable energy). It is not just climate change that is driving the globe towards zero emissions. It’s a factor even more powerful than moral rectitude. It’s economics.

Renewables today are already the lowest cost grid power option, materially lower in cost than all fossil fuel alternatives. But cost is not the only issue here. Variability and dependability of supply from renewable is the main challenge. There are various solutions to this challenge, including pump hydro storage and natural gas. However, the most efficacious solution from an emissions and latency standpoint, and the one currently seeing the fastest deployment globally is grid battery storage. This will further supercharge the demand for lithium batteries, with long term demand from grid storage alone, potentially multiples of that from EVs.

Nevertheless, the move to zero emission transport is rapidly building momentum. More and more countries are announcing bans on ICE vehicles including UK, Denmark, Ireland, Netherlands, Slovenia, Israel, India and Sweden all banning sale of ICE vehicles after 2030 and France and Singapore after 2040. Sales of EVs in Norway have recently passed above 50% of all vehicle sales (54%). Other Scandinavian countries are not far behind (Iceland, Sweden, Finland), but also countries like the Netherlands, Portugal and China.

Whilst global ICE vehicle sales have plummeted during 2020 due to COVID-19, EV sales have boomed not only in China but more importantly in Europe. Recently in Germany, EV sales have surpassed the sale of diesel powered vehicles (previously >50% of all vehicle sales in Germany were diesel powered).

We have clearly seen EV sales accelerated somewhat by COVID-19. Nonetheless this momentum had been building (unperceptively) for some time. Somewhat evidenced by the complete pivot that many leading global auto OEMs (Original Equipment Manufacturers) have performed on their future model plans.

Volkswagen is shifting exclusively to EVs and by 2030 will have more EV than ICE models, Volvo is doing so sooner with >50% of models planned to be electric by 2025, Toyota expects to sell 4.5 million EV/hybrids by 2030, even GM has announced the EV Hummer (first year’s production in 2021 was fully reserved within 10 minutes of launch online).

Hundreds of billions of dollars of OEM research and development (R&D) have been shifted from ICE to EV development whilst battery technology continues to improve at 12-15% p.a. in energy density and cost. Tesla is now at or below the magic US$100/KWh battery cost tipping point where the cost of EVs become on par with ICE vehicles.

For us at Eiger, all this change provides us with interesting investment opportunities. There are a number of Aussie small caps exposed to the lower end of the EV supply chain. We believe it is at this early point in the supply chain, particularly in lithium mining (for batteries) and rare earths mining/production (for magnets used in synchronous electric motors), where the likely price pinch points will emerge.

Our two positions in lithium mining, IGO Ltd (IGO) and Pilbara Minerals (PLS) along with our position in Lynas Rare Earths (LYC) are all tier one global producers with long mine lives and are at the bottom end of their respective global cost curves.

These three are not planned projects or exploration opportunities. All are existing operating and producing businesses that can quickly respond to increased demand (and higher prices). Each can also quickly expand production either via lower risk brownfield expansions or in PLS’s case via the recent purchase of their neighbour out of bankruptcy and at below replacement cost. PLS was the largest contributor to the Eiger Australian Small Companies Fund’s performance over the December 2020 quarter and LYC was number two.

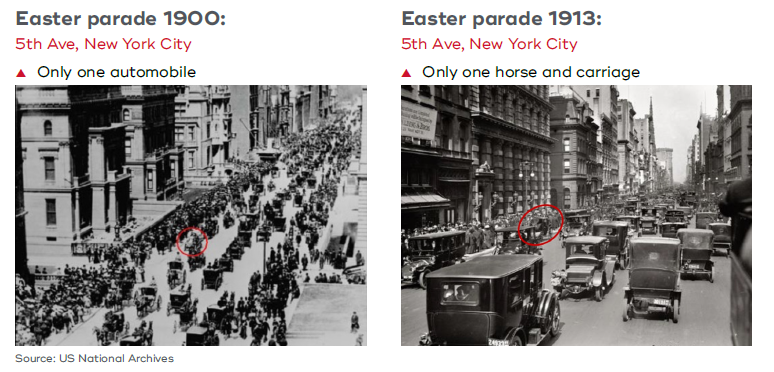

To finish, we like these two photos we’ve previously used to illustrate how quickly structural change can happen. Just as with the last great change in transport technology at the turn of last century, we may be surprised that by 2030 ICE vehicles are as rare as horses were at the Easter grand parade on Fifth Avenue New York City in 1913. As they say a picture (or two) tells a thousand words.

In the words of that great philosopher, George W Bush, the future investment opportunities in Aussie small caps in the EV and battery storage space are not to be misunderestimated.

Stay informed in 2021

Stay up to date with my latest views. Hit the FOLLOW button below to be notified by email as soon as I publish my next wire.

^ 1 Quote from GWB – Bentonville Arkansas, 6.11.2000 – “They misunderestimate me”.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Victor is a co-founder of Eiger Capital and Senior Portfolio Manager for the Eiger Australian Small Companies Fund.Prior to establishing Eiger, Victor worked with Stephen on the UBS Australian Small Companies Fund since 2011. Prior to this, Victor worked at fund managers including BT Investment Management, Platinum, Hayberry & Selector.

4 topics

3 stocks mentioned

Victor is a co-founder of Eiger Capital and Senior Portfolio Manager for the Eiger Australian Small Companies Fund.Prior to establishing Eiger, Victor worked with Stephen on the UBS Australian Small Companies Fund since 2011. Prior to this, Victor...

Expertise

Victor is a co-founder of Eiger Capital and Senior Portfolio Manager for the Eiger Australian Small Companies Fund.Prior to establishing Eiger, Victor worked with Stephen on the UBS Australian Small Companies Fund since 2011. Prior to this, Victor...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Investing for the biggest market shift since the GFC

Livewire Markets

Equities

Why ex-20 is the prime hunting ground for ASX returns

Livewire Markets