If You’re Shocked That Trump Won You Shouldn’t Be Managing Money

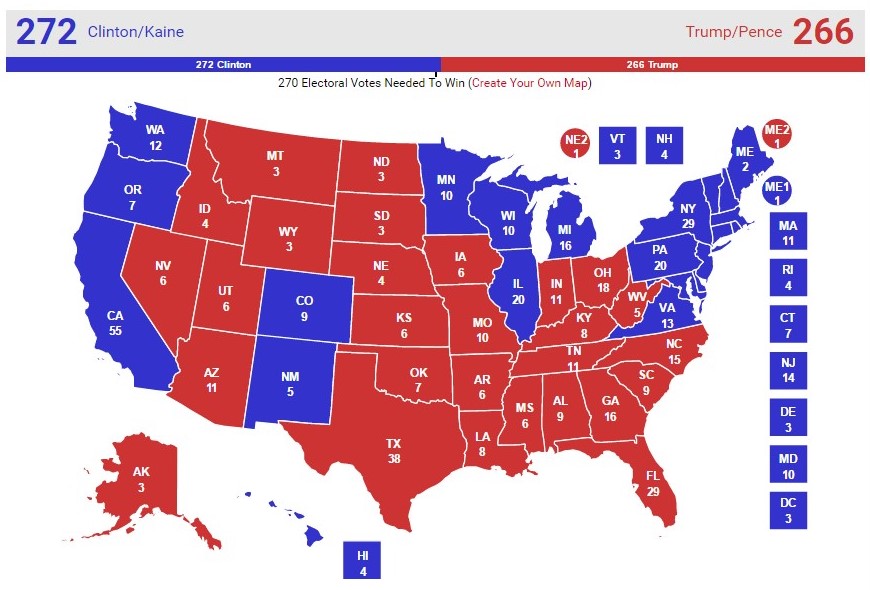

In the aftermath of the US presidential election Donald Trump’s victory is continuously being called “shocking”. The reality is that the result was not a shock at all. The graphic from Real Clear Politics below is their final prediction of where the states would land, published on the day before the election. All Trump needed to do to overcome Clinton’s slender lead was win a few thousand more votes in New Hampshire. Anyone who looked at this graphic alone would have said that the only certainty was a close race.

A reasonable person delving further into the widely available data would also have looked at the early voting patterns. Here Trump was doing better than Romney did in key states. Clinton was leading, but it is widely known that Democrats do better in early voting and Republicans do better on election day. What the early voting also revealed was that polls were oversampling Democrat voters, a point Republican supporters had frequently raised.

The response rate to polls had slumped from 20% to 5%, making the potential for error much higher than previous elections. Yet still the polls had narrowed substantially in the weeks leading up to the election. After the release of the infamous Trump video in early October many assumed Trump had no chance. However, after FBI Director James Comey said the Clinton email investigation was being re-opened Clinton’s lead slumped. On the final day, two of the three polls released had Trump ahead after Clinton had won most, but not all polls in the previous week. Many simply focussed on the headline number of Clinton being ahead by an average of 2%, ignoring the early voting trends, the shift in the polls, the electoral college distribution and discarding concerns about polls not being representative.

So how did the consensus get it so wrong? As is so often the case in financial markets very few people looked at the data and instead deferred to “expert” opinion. People who had a personal bias and vested interests repeated the mantra that Clinton was the better candidate and therefore Clinton must win. The mainstream media, celebrities, economists, big donors and politicians all agreed. Their personal view on what “should” happen became their professional view on what “would” happen. The forgot to ask ordinary people, who make up the vast majority of voters, what they thought and assumed their view reflected what everyone else thought. This was Brexit all over again.

To summarise, you would have been shocked by Trump winning if you were:

- Just looking at the headlines and not looking at the underlying data

- Not reading widely and listening only to people who think like you do (and also don’t read widely)

- Deferring to and trusting people who had clear personal biases and vested interests

If that’s the way you analyse then you are clearly not suitable to manage money. You’ll be confined to trend following, jumping on the bandwagon after most of the gains have been had and getting stuck with most of the losses when the trend reverts. What the wise do in the beginning, fools do in the end.

So if the consensus of expert opinion and financial markets got the US Presidential election wrong what other consensus views might be wrong?

- Consensus says valuations are just a little above average but this time is different as low interest rates justify these valuations. The data says asset prices are substantially overvalued when actual company earnings are used rather than the inflated version that excludes all the bad stuff. This alternate view helps management please naïve investors ensuring they get bonuses and keep their jobs.

- Consensus says the US economy has had a decent recovery since the financial crisis. The data says this is the worst recovery from a recession in decades and it is running on the fumes of credit growth.

- Consensus says that the world has deleveraged and de-risked since the financial crisis. The data says that debt levels have continued to grow with US high yield markets, emerging market debt and developed market government debt levels growing the most. Some European banks remain woefully undercapitalised with very high levels of non-performing loans.

- Consensus says that money printing isn’t creating unacceptable levels of inflation. The data says that there has been substantial inflation in asset prices creating the risk of meaningful falls in asset prices if money printing is curtailed. Just because Japan hasn’t seen hyperinflation yet doesn’t mean that the hyperinflation in Zimbabwe and Venezuela can’t happen in developed economies.

- Consensus says that government debt is a safe haven asset. The data says that governments have made unsustainable promises to their citizens in pensions and welfare spending, both of which will be given priority over debt repayments in the event of a default. The low interest rates that make debt able to be serviced today can quickly change making refinancing of debt much more expensive if possible at all. The failure to generate budget surpluses and deleverage increases the risk that debt buyers will lose confidence.

The victory of Donald Trump in the US Presidential election was a shock to those who held the consensus view that Hillary Clinton would surely win. Mainstream media, celebrities, economists, big donors and politicians are struggling to digest that their opinions were vastly different to the electorate. For those who looked at the data Trump’s victory was no surprise, the data pointed to a very tight result that could go either way.

Investors should take a big lesson from this; the market will punish uninformed opinion and feelings. If you can’t put these aside and do independent analysis you shouldn’t be managing money for yourself or anyone else. If you can, you have a huge edge over the consensus and have a decent shot at outperforming other investors.

Written by Jonathan Rochford for Narrow Road Capital on November 10, 2016. Comments and criticisms are welcomed and can be sent to info@narrowroadcapital.com

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Narrow Road Capital is a credit manager with a track record of higher returns and lower fees on Australian credit investments. Clients include institutions, not for profits and family offices.

3 topics

Narrow Road Capital is a credit manager with a track record of higher returns and lower fees on Australian credit investments. Clients include institutions, not for profits and family offices.

Expertise

Narrow Road Capital is a credit manager with a track record of higher returns and lower fees on Australian credit investments. Clients include institutions, not for profits and family offices.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Investing for the biggest market shift since the GFC

Livewire Markets

Equities

Why ex-20 is the prime hunting ground for ASX returns

Livewire Markets