Iron Ore: Is the price about to roll?

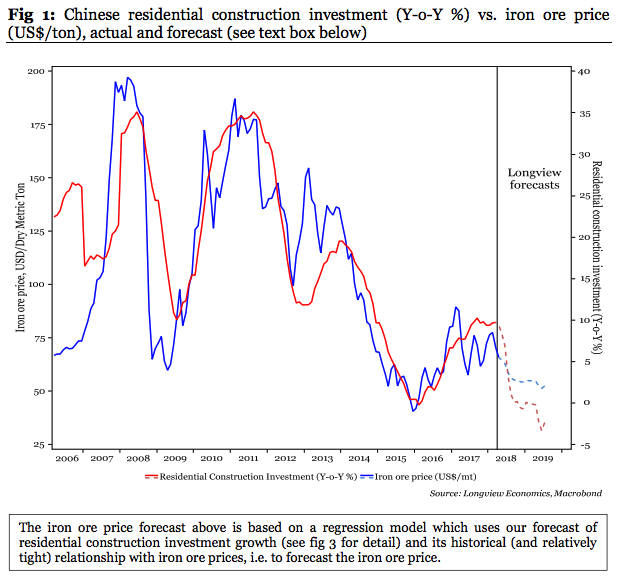

Chinese steel consumption is the most significant variable in determining the iron ore price. China consumes over half of the world’s iron ore each year. As such, and while supply themes play a role, cycles of Chinese credit growth and housing activity are the key factors in determining iron ore price direction. That’s evidenced, for example, by the strong correlation between key Chinese macro indicators and the iron ore price.

Fig 1: Chinese residential construction investment (Y-o-Y %) vs. iron ore price (US$/ton), actual and forecast (see text box below)

The iron ore price is up over 65% since 2015. The key question is whether that price strength will be underpinned by a re-acceleration in China’s economy (and, with that, strong metal demand growth), OR whether that relief rally will be a short-lived affair.

We expect it is the latter, and therefore an opportunity to UW/sell iron ore and iron ore proxies (e.g. the AUD and mining equities).

In particular, both cyclically and structurally, China’s economy is slowing. The cyclical slowdown evidenced across several indicators is a result of PBoC tightening last year and is likely to persist in coming quarters. Structurally, China’s economic growth model is becoming less steel intensive.

As such, and with evidence that the build-out of infrastructure (and property) has become excessive, trend growth in Chinese steel (and iron ore) consumption is likely to continue slowing.

Naturally, the widely discussed cuts to steel production capacity, expected to continue to 2020, add to the case for a reduction in iron ore demand (albeit most of that cut capacity is being replaced).

Adding to that demand backdrop, and with iron ore prices still well above production costs, global supply growth is likely to remain reasonably strong, with iron ore supply surpluses likely to persist this year and next.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Longview Economics, founded in 2003 by Chris Watling, is an independent research house based in London, providing three distinct yet interrelated groups of research products: Short and medium term market timing; Long term global asset allocation advice; and Global thematic, macro and commodities research.

2 topics

Longview Economics, founded in 2003 by Chris Watling, is an independent research house based in London, providing three distinct yet interrelated groups of research products: Short and medium term market timing; Long term global asset allocation...

Expertise

Longview Economics, founded in 2003 by Chris Watling, is an independent research house based in London, providing three distinct yet interrelated groups of research products: Short and medium term market timing; Long term global asset allocation...

Expertise

Comments

Comments

Sign In or Join Free to comment