TOL - 16th Nov, 2020

Is the sharemarket correctly pricing-in fundamentals?

When Afterpay's share price recently rose above A$100, its market-cap surpassed some of Australia’s most successful global companies, such as Amcor, Brambles and Orica. Afterpay has become a poster child for the momentum-type growth-obsessed phenomena currently driving sharemarkets. In this article, we analyse these companies’ fundamentals and we seek to provide an objective insight into the ‘blue sky’ being factored into Afterpay’s share price.

Sharemarkets around the world, including Australia’s, have experienced very strong rallies since their March lows thanks in the main to interest rates being cut to record lows and large quantitative easing from central banks. It can be argued that this flood of cheap money has led many speculative-type growth stocks to trade well above their fundamental value, led by the NASDAQ in the US.

Consumer patterns changed markedly through the COVID-19 virus lockdowns, as consumers stayed at home and as volumes in many areas facilitated by the internet have all boomed such as online shopping, social media, online conferencing, online gambling, and streaming services such as Netflix and Stan here in Australia. This has led to a significant rise in almost any stock that is technology-related.

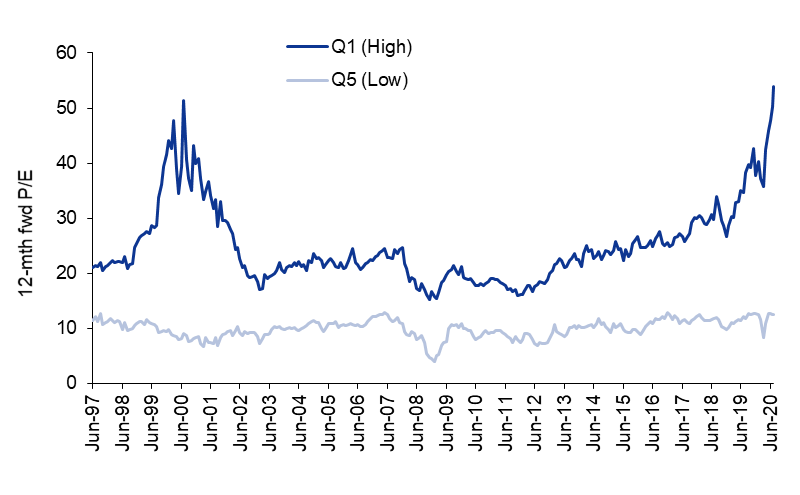

This phenomenon has driven the divergence between value and growth stocks to expand to levels which have now surpassed the ‘tech boom’ of 1999-2000, as Chart 1 below shows. With this momentum currently in full swing, many investors appear less concerned about the underlying fundamentals or valuations of many companies, and are instead focusing on anything with blue sky potential, particularly in the technology sector.

Chart 1: Average Price/Earnings of ASX200 Firms by Forward P/E Quintile

Source: Goldman Sachs Report 11 August 2020; chart range 30 June 1997 – 30 June 2020

Afterpay

Afterpay is a ‘buy now pay later’ (BNPL) service provider founded in Australia in 2017. Since 2017 it has expanded its operations into New Zealand, North America and the United Kingdom. Afterpay offers an app-based service which allows consumers to pay for goods and services over four equal instalments. The base service is offered to customers free of charge, with retailers paying a percentage of the purchase price to Afterpay. Customers face financial penalties if instalment payments are late or not made (capped at $10 for order values below $40; for order values above $40, late fees are up to the lesser of 25% or $68).

The value proposition of a BNPL provider like Afterpay is giving many consumers readily available credit to facilitate the purchase of goods. BNPL facilitators like Afterpay offer a service similar to credit cards, except that consumers do not pay application fees and can be given credit instantaneously once they download the service, as they do not have to undergo extensive credit checks.

Afterpay earns its income from commissions payable by the retailer to Afterpay (as do credit card providers), and from late payment penalties from its subscriber base. From the retailer’s point of view, Afterpay works like a credit card, giving consumers ready credit to make purchases while Afterpay takes on the credit risk of any customer defaults.

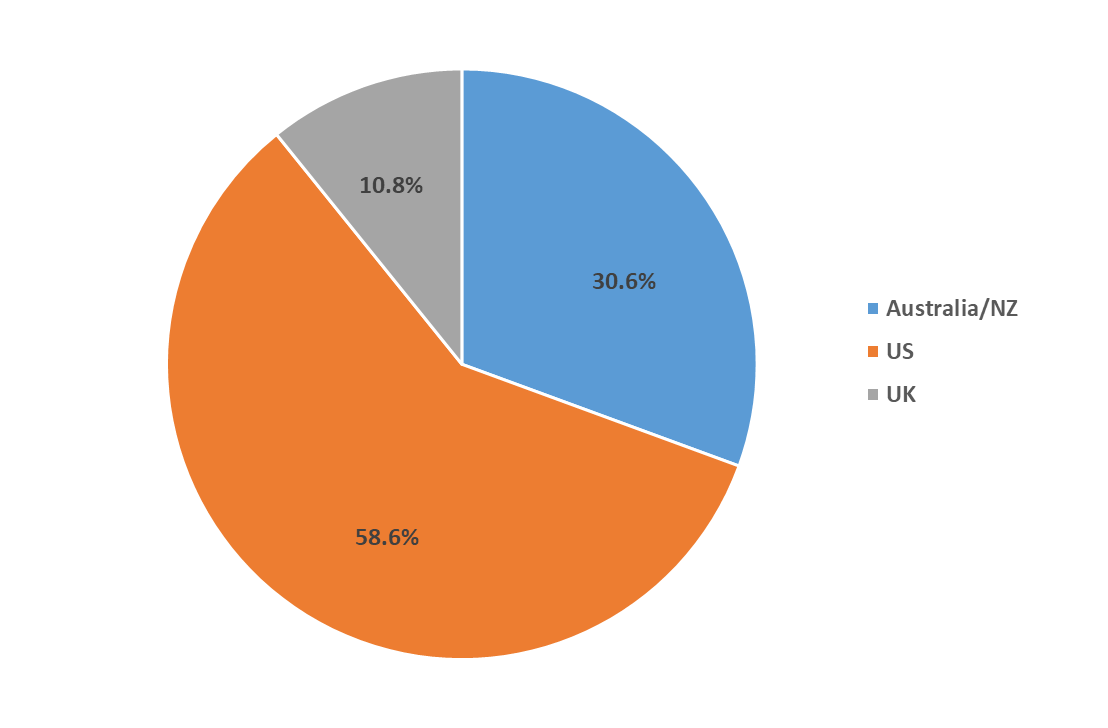

Afterpay has approximately 11.1 million customers at the time of writing. Chart 2 below summarises the geographical distribution of the customer base.

Chart 2: Geographical Distribution by % of Afterpay Customer Base

Source: Afterpay Q1 FY21 Business Update, 28 October 2020

In financial year 2020, Afterpay’s customers used the service to buy some $11 billion worth of goods, made up of $6.5 billion in Australia and New Zealand, $4 billion in the US, and $500 million in the UK. These sales generated $433.8 million in revenue earnt by Afterpay.

The company’s strategy is focused on its rollout. After moving swiftly to gain first mover advantage in the Australian BNPL market, Afterpay’s attention has turned to the significantly greater opportunities presented in the northern hemisphere, where in many markets the company also appears to have first mover advantage. The outcome is an attempt to create differentiation from competitors through the generation of a ‘network effect’. As with any landgrab, however, there is a constant need to reinvest in growth. This elongates the time to generate any free cashflow. In the meantime, the BNPL space is becoming increasingly competitive with most players offering a relatively similar product.

The risks to Afterpay include other BNPL providers such as Zip Co, Splitit, and Sezzle becoming more aggressive by offering better commissions to retailers.

An additional risk is the entry of established financial players entering the BNPL segment. Globally, various banks as well as Visa and Mastercard have entered into agreements with BNPL providers. While these large global participants are likely to prove rational in their approach to the BNPL market, their ability to compete with Afterpay is significantly greater than most pure-play BNPL peers given their huge balance sheets.

PayPal is another recent example of an established financial player entering this segment. PayPal is a very well-capitalised, substantial and profitable business which is already well-known and trusted by merchants. Payments through PayPal are already offered by 80% of the top US retailers, and approximately 70% of US online buyers have a PayPal account. PayPal has a net cash balance of approximately US$6.9 billion (which is larger than the collective market-caps of all the Australian listed BNPL providers bar Afterpay) and PayPal’s financial year 2020 forecast net profit is US$4.4 billion.

PayPal’s ‘Pay in 4’ BNPL offering is also cheaper to the merchant on average than Afterpay’s offering (at 2.9% compared to an average of 4% from Afterpay), while the additional BNPL service is essentially ‘free’ to the merchant, as PayPal already charges merchants 2.9%, which is a significant differentiator. Additionally – and importantly for Afterpay’s growth ambitions – PayPal is in a very strong position to achieve and maintain market share in the US and will have no issues in funding its book and in funding aggressive promotion and customer acquisition for its new service.

Despite Afterpay’s first mover advantage and early success, competition in the sector is quickly picking up which suggests that margins will come under pressure moving forward as new entrants and established players move into this space.

Another key risk to Afterpay is regulatory risk – as the sector continues to grow, and in particular in the event of any publicity resulting from distressed customers, the BNPL sector is likely to face increased scrutiny and regulation and we would expect this to accelerate moving forward.

Current Revenue and Earnings

Afterpay’s focus on reinvestment means that it is not yet profitable. On current run rates the business is estimated to deliver a $25 million profit in FY 2021, although any decision to accelerate its rollout may push profitability further out.

Given Afterpay’s current market capitalisation of around $29 billion, a fairly generous PE of 30 times multiple and the current market-cap implies that Afterpay earns net profits after tax of $1 billion (as compared to zero profit currently). Working backwards from this, for Afterpay to earn $1 billion, the company would need to have 40-50 million customers (compared with the current 9.9 million). This again assumes that current merchant fees of ~3.5-4.0% are maintained and not reduced as a result of other BNPL competitors offering better deals to retailers.

In broad terms, we see the future addressable market for BNPL services in Australia, the US and the UK as ~140 million people, which assumes 50% of people aged 15-65 having a BNPL account. For Afterpay to gain 40-50 million customers, the company would need to achieve 30-35% market share.

This is a fairly big leap of faith in our view, especially given the credit, competition, and regulatory risks involved in getting to that scale. This scenario also does not consider the capital that will need to be raised as Afterpay’s loan book grows, or the risk that margins may fall over time as more providers enter the BNPL space, or any pick-up in bad debts, which are currently very benign.

We will now briefly discuss the fundamentals of three well-established global companies – Amcor, Brambles, and Orica, to describe the fundamentals underpinning their business models.

Amcor

Amcor is a global leader in the provision of consumer packaging products, with more than 95% of the company’s sales into consumer end markets such as the food, beverage, healthcare and personal care segments. The company was founded in 1860 and today operates across 230 locations in more than 40 countries. Amcor’s customers include some of the largest consumer product companies in the world, among them Pepsico, Nestlé, Unilever, Johnson & Johnson, and Kraft Heinz.

Amcor’s strategy is to develop scale in its key focus areas of flexibles packaging, rigid packaging, specialty cartons and closures. This has been achieved through a combination of organic growth and bolt-on acquisitions, which has enabled Amcor to develop leading regional market positions across each business segment. For example, in flexibles packaging, Amcor is the clear number one in North America, Europe, Latin America and Asia. Competition is typically on the basis of quality, price and reliability, although sustainability is becoming an increasingly important point of differentiation.

Amcor’s scale enables it to invest more than its peers in developing new sustainable packaging solutions and underwrite investments in recycling infrastructure to access recycled plastic resins, which its customers are increasingly demanding.

Current Revenue and Earnings

Amcor generated US$12.5 billion in sales and US$1.03 billion underlying profit after tax in FY 2020. The business’ margins have grown over time, driven by increased scale and an improved mix, as the business targets higher value-add segments such as healthcare.

Given the defensive and essential nature of the end markets served, Amcor’s revenues are highly recurring and predictable and underpinned by long-term contracts. Over the medium term, we expect the business to grow earnings in the mid-single-digit range, driven by modest volume growth, further mix improvement and further bolt-on acquisitions.

At the time of writing Amcor is trading on around 16.3 times 2021 and 15.8 times FY2022f PE, which looks fairly reasonable for a global packaging leader which generates strong cashflows by servicing defensive end markets.

Brambles

Brambles, through its subsidiary CHEP, is the global leader in pallet pooling solutions. CHEP’s wooden pallets are an essential and integrated part of consumer staples supply chains all around the world. Brambles’ CHEP pallets are used by companies such as Proctor & Gamble, Unilever, PepsiCo, and many others to deliver their products to retailers such as Walmart, Costco, Amazon.com, Tesco, Carrefour and Woolworths. After delivery, the pallets are returned to a CHEP service centre for repair and reuse, and Brambles earns a rental fee for the use of the pallet.

CHEP started in Australia in 1946, using pallets left by the US Army after World War II. Over the last 74 years CHEP has used its accumulated profits to fund the purchase of new pallets and has expanded into new markets. CHEP now holds the clear number one market share position in about 60 countries worldwide, including about 70 - 80% market share across the largest pallet markets in the US, UK, Europe, Latin America and the Asia-Pacific. Brambles’ global pool of reusable pallets has now grown to around 300 million units.Pallet pooling is a business that requires economies of scale. Having more service centres than any other competitor means that CHEP can deliver and retrieve pallets while minimising transport distances. This network advantage creates a significant barrier to entry, and once established in a country CHEP has never lost its number one market position.

Current Revenue and Earnings

Brambles earnt global revenues of US$4.7 billion and made an underlying profit after tax of US$504 million from continuing operations in FY 2020. Brambles earns healthy profit margins from its global CHEP pallet network because of the competitive advantage of the network efficiencies outlined above. Over time, revenue and earnings should continue to grow at mid-single digit rates, driven by growth in emerging markets where pallet use is still developing; by converting customers in mature markets from single use, disposable pallets to pooled pallets; and through modest price inflation. Importantly, because CHEP pallets are used for everyday consumer items, Brambles should deliver this growth in a relatively consistent and low-risk manner.

Brambles is currently trading on a PE of around 21.6 times 2021 earnings and 19.4 times FY 2022 earnings. While wooden pallets may not be an exciting new industry, owning a global leader with a hard to replicate business model and strong fundamentals certainly looks a reasonable proposition at this valuation.

Orica

Orica is the global leader in explosives and innovative blasting systems to the mining, quarrying and construction industries around the world. The company services customers across more than 100 countries and has highly strategic ammonia nitrate manufacturing plants in several countries located close to its customers. Orica services a diverse group of customers, the majority being large blue-chip miners including BHP Billiton, Rio Tinto and Newcrest Mining. The company also has an extremely experienced management team and Board.

Demand for Orica’s products and services is recurring in nature and driven by mining volumes. Mining volumes have a long history of growth over many decades, as typically ore grades fall slowly over time as mines get older and deeper. This means demand for explosives typically grows as more earth or overburden needs to be removed each year for the miner to get the same amount of ore out of the ground.

The explosives industry is reasonably consolidated, with each major continent possessing only a few competitors. Orica is the scale player in many of the major mining countries in the world, and its key competitive advantages are the location of its ammonia nitrate plants and the firm’s significant scale of investment in research and development and technology, which enables Orica to lead the market with innovative products and services and grow its market share globally.

We expect fairly significant earnings growth and cost savings over the next three to five years. This should be driven by the introduction of SAP enterprise resource planning software across Orica’s global network, from synergies from the recent acquisition of Peruvian explosives manufacturer Exsa, and through ongoing operating efficiencies from better inventory management and plant optimisation, as well as through the introduction of new products – such as wireless detonation.

Current Revenue and Earnings

Orica is expected to earn global revenues of $5.6 billion in FY 2020, and make an underlying profit after tax of $320 million. The company’s revenue and earnings should grow around mid-single-digit rates, driven by growth in mining volumes, incremental market share gains and growth in new products and services, in particular from Orica’s new wireless blasting initiating systems.

Orica is currently trading on a PE of around 18.2 times 2021 and 14.5 times FY 2022 earnings on our estimates. This multiple looks highly attractive to us, given that the firm is a global leader with strong competitive advantages and possesses a positive long-term growth outlook.

Conclusion

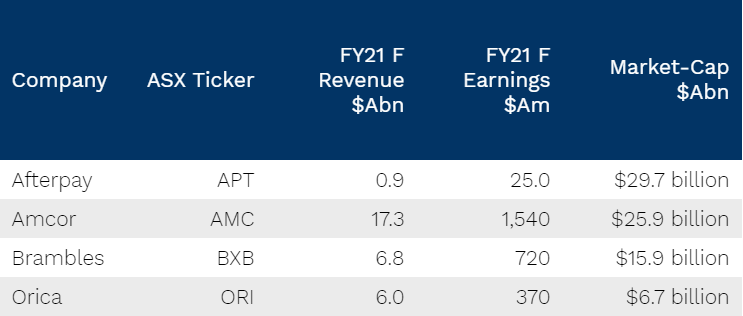

We began this article by noting the extraordinary valuation that the sharemarket is assigning to Afterpay compared to well-established, profitable companies like Amcor, Brambles, and Orica. Given the global scale and profitability of these businesses, this valuation indicates that investors are taking an enormous leap of faith in Afterpay’s ability to reach sufficient scale and profitability to justify its near $29 billion market valuation.

Table 1: Afterpay, Amcor, Brambles, Orica – Key Financial Metrics

Sources: Investors Mutual, Iress, FactSet. Data as at 10 November 2020

To put the market caps of the other well-established companies we reviewed into context, Afterpay was recently valued at more than Amcor, one of the largest packaging companies in the world, and much larger than Brambles and Orica combined.

No matter how good the future prospects of Afterpay are, to have it valued at more than one of the largest packaging companies in the world as well as higher than the largest pallet and explosive companies in the world COMBINED seems to be a fairly optimistic way of valuing the company.

It took Amcor, Brambles and Orica many decades to reach the global scale that they are at today – and they reached this scale through several ups and downs in the last three decades.

In a nutshell as a long-term investor focused on not taking excessive risk, we prefer to back the proven fundamentals, management and track records and steadily growing profitability of well established companies like Amcor, Brambles and Orica than to use what looks like excessively optimistic forecasts to try and justify Afterpay’s current valuation and share price.

When markets are in an exuberant phase, it requires discipline and patience to avoid what look very like excessively priced sectors and stocks and to stay true to our fundamental approach. Our discipline back in 1999/2000 rewarded our investors with substantial subsequent outperformance, and the conditions we see in sharemarkets today seem to echo the hype of that period.

Our approach remains that of anchoring our portfolios with high-quality companies with strongly defensive characteristics using a low portfolio turnover approach and seeking to produce tax-effective income streams for our investors.

We continue to believe that investing in well-established, profitable companies with sound fundamentals will ultimately prove to be a much more successful investment strategy than chasing the latest exciting sector or fad.

Never miss an insight

Be the first to read all my latest Livewire thought pieces by clicking the follow button.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Anton Tagliaferro is one of Australia’s most highly respected value-style fund managers. Anton founded IML in 1998 with the purpose of creating a research-driven fund manager focused on building portfolios of companies that represent both 'quality and value'.

Anton arrived in Australia in the 1980’s and was soon drawn to the sharemarket at a time when high-flying entrepreneurs dominated the headlines. His passion for investing in the sharemarket has not waned and he continues to put his considerable experience and the important lessons learnt over the last three decades to mentor the IML investment team and to deliver to clients' expectations.

........

While the information contained in this article has been prepared with all reasonable care, Investors Mutual Limited (AFSL 229988) accepts no responsibility or liability for any errors, omissions or misstatements however caused. This information is not personal advice. This advice is general in nature and has been prepared without taking account of your objectives, financial situation or needs. The fact that shares in a particular company may have been mentioned should not be interpreted as a recommendation to buy, sell or hold that stock. Past performance is not a reliable indicator of future performance.

4 stocks mentioned

Anton Tagliaferro is one of Australia’s most highly respected value-style fund managers. Anton founded IML in 1998 with the purpose of creating a research-driven fund manager focused on building portfolios of companies that represent both 'quality...

Expertise

Anton Tagliaferro is one of Australia’s most highly respected value-style fund managers. Anton founded IML in 1998 with the purpose of creating a research-driven fund manager focused on building portfolios of companies that represent both 'quality...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Investing for the biggest market shift since the GFC

Livewire Markets

Equities

Why ex-20 is the prime hunting ground for ASX returns

Livewire Markets