Is this the Next Credit Corp?

Credit Corp listed in September 2000 at 50c per share. Based on the closing price of $17.62, this represents capital growth of 3,424%. Additionally, the company has paid $3.33 (660%) in fully franked dividends. Here’s our case for the company we consider most likely to be the ‘next Credit Corp’.

What’s So Good About Credit Corp?

Firstly let me be clear: whenever someone says ‘this stock is the next such and such’, it usually isn’t! In fact, I could count on both hands the number of times that analogy has turned out to be true. So I would encourage you to start from a position of scepticism, and critically prove why this could indeed be the next Credit Corp.

Secondly, in order to understand why ‘being the next Credit Corp’ is even worth aspiring to, we need to take a step back and understand just how good an investment it has been.

Credit Corp is a receivables management business, which purchases packages of ‘distressed’ debt at a fraction of the original cost, and then work to recover as much of that debt as they are able to.

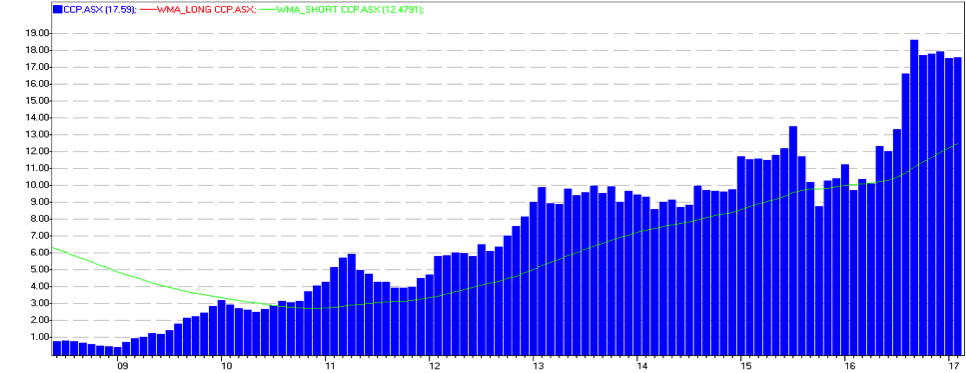

Shareprice from $0.50 at IPO to over $17.00 today

Credit Corp listed on the Australian Stock Exchange on the 4th September 2000. The issue price was 50 cents per share. A total of 11m shares were issued, raising a modest $5.5m. Over the following months, the stock dropped to a low of 40c as the sprinters departed, leaving the marathon runners to go the distance.

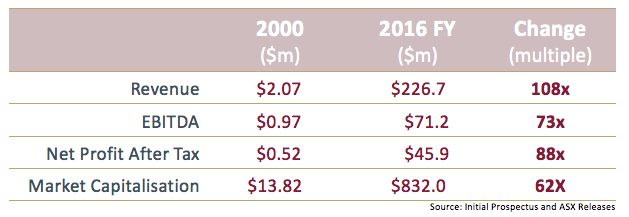

The prospectus forecast revenue for 2000 of $2.067m and a maiden profit as a listed entity of $519k. As it turns out both of these numbers were surpassed, and this has been a recurring theme throughout their history.

If we fast forward 16 and a bit years, we can see how extraordinarily successful the company has been:

And not surprisingly, this strong growth over such an extended period has been reflected in the share price.

Capital gains and a strong yield

As we can see below, the share price reached an all-time high recently of $20.16 and in the past few months, the price has consolidated around the $17 to $18.50 level. At the most recent close of $17.62, this represents a 3,424% return on investment.

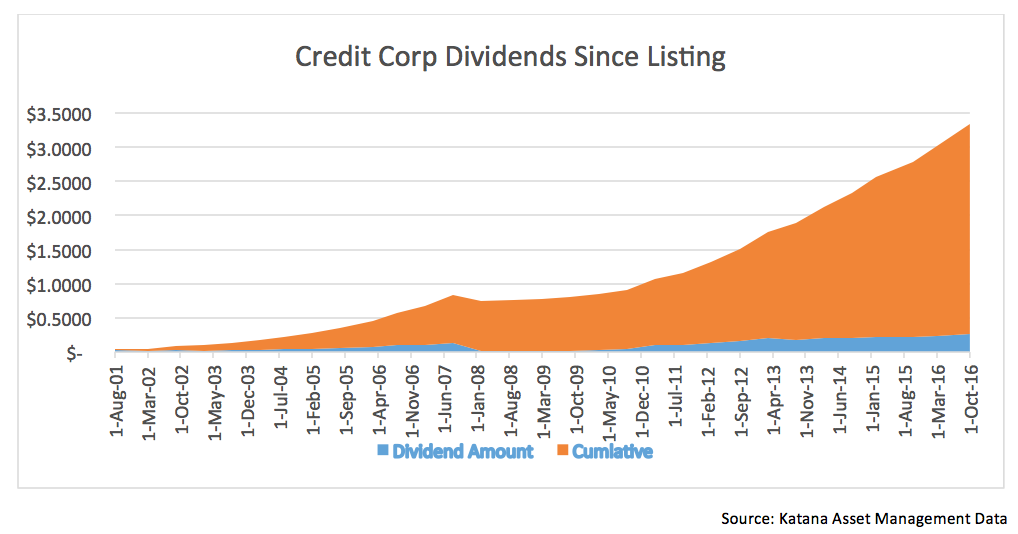

Even more impressively – if that’s possible – the capital growth component is only part of the story. Since listing, Credit Corp has paid a whopping $3.33 in dividends. That’s a 660% return on the initial entry price in dividends alone. If we include franking credits, that number grows to $4.76 per share.

Who Could Be the ‘Next Credit Corp’?

To begin with, in the listed collectables space, the alternatives to Credit Corp are Collection House Limited (CLH) and Pioneer Credit Limited (PNC), so we’re not fishing in a deep pool. But as we have seen from Credit Corp, this is a lucrative niche if executed well. Not surprisingly then, we see potential upside in both competitors, however it is Pioneer Credit that has attracted our particular interest at this time.

Pioneer Credit listed on the ASX in May 2014 at an issue price of $1.60 per share. The company is headquartered in Perth, Western Australia and has a customer service centre in Manila, in the Philippines.

The founder and MD of Pioneer – Mr Keith John - has extensive experience in the receivables management industry, a journey he commenced in 1988. And this is where the analogy to Credit Corp gains some credence. Prior to the listing of Pioneer Credit, Mr John actually sold his business – then known as Pioneer Credit Management Services Pty Ltd – to none other than Credit Corp in July 2006. At that stage Pioneer had 65 full time staff.

In the ASX Release which accompanied the acquisition, the then MD of Credit Corp Mr Geoff Lucas stated:

“Managing Director Keith John is a highly regarded Executive in the industry and he has built an organisation with an exceptional reputation and a culture closely matching our own. …Keith has successfully built Pioneer Credit into one of Australia’s leading private recovery firms.’

Mr John’s services were in high demand by Credit Corp and he became part of the Senior Management Team, taking on the role of Head of Strategic Business.

In January 2007, Mr John then sold a second business – Pioneer Credit Malaysia – once again to none other than Credit Corp.

Mr John worked at Credit Corp until late 2007 at which time he resigned and spent some time with his young family. Mr John re-purchased parts of the business in 2009 and in doing so, Pioneer Credit as we know it today was re-born.

Assembling a strong team

In re-establishing Pioneer, Mr John has once again focussed on building a strong corporate culture. This is evident at all levels of the organisation from the CFO Mr Leslie Crockett to COO Ms Lisa Stedman right down to the teams on the floor that assist clients to rehabilitate their credit status.

And importantly, the Board of Directors is one of the higher calibre Boards we have encountered for a company of this size. This is epitomised by Mr Michael Smith, well known for his leadership as Chairman of iiNet.

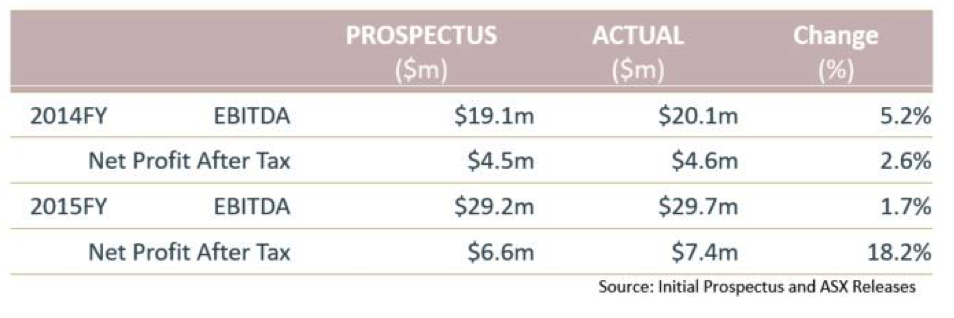

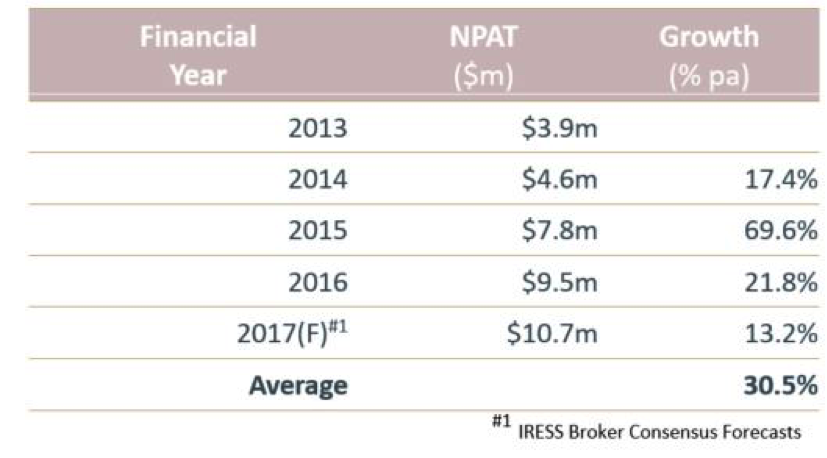

Since listing, Pioneer Credit has emulated the approach of the best companies, by under-promising and over-delivering. In the 2014 Prospectus, Pioneer forecast substantial revenue and earnings growth, which many believed were unachievable. In the fullness of time, they not only met but exceeded each of these outcomes.

Whilst these beats are only modest, the key here is that Pioneer’s growth to achieve these numbers was extraordinary. In fact, from 2013 to 2017 (forecast), Net Profit After Tax (NPAT) has grown at 30% per annum.

And this is at the core of the comparison with Credit Corp, whose ultimate success has come from strong earnings growth compounding on itself year after year.

As Albert Einstein said ‘The most powerful force in the universe is compound interest.’

In the case of investing, the most powerful force is compound earnings. A spectacular one-off increase in earnings is great, but to see a share price grow to the extent that Credit Corp has, we need high earnings growth compounding on itself year after year.

All this ... and at a single digit PE...

Yet despite this strong history of growth, Pioneer Credit is trading on multiples that would gladden the heart of the most diehard value investor. On our analysis, Pioneer is on track to earn 27 cents per share in the 2018FY.

At the last traded price of $2.13 per share, this equates to a PER of 7.9x earnings and a dividend yield of 6.3% fully franked (based on a 50% payout ratio).

In Pioneer, we see that rare trifecta of growth. value, and excellent management.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Katana Asset Management was founded in September 2003 as a boutique investment management firm. Katana employs an all opportunity investment mandate being style, sector and market cap agnostic.

.jpg)

2 topics

2 stocks mentioned

.jpg)

Katana Asset Management was founded in September 2003 as a boutique investment management firm. Katana employs an all opportunity investment mandate being style, sector and market cap agnostic.

Expertise

Katana Asset Management was founded in September 2003 as a boutique investment management firm. Katana employs an all opportunity investment mandate being style, sector and market cap agnostic.

Expertise

Comments

Comments

Sign In or Join Free to comment