It’s volatile!

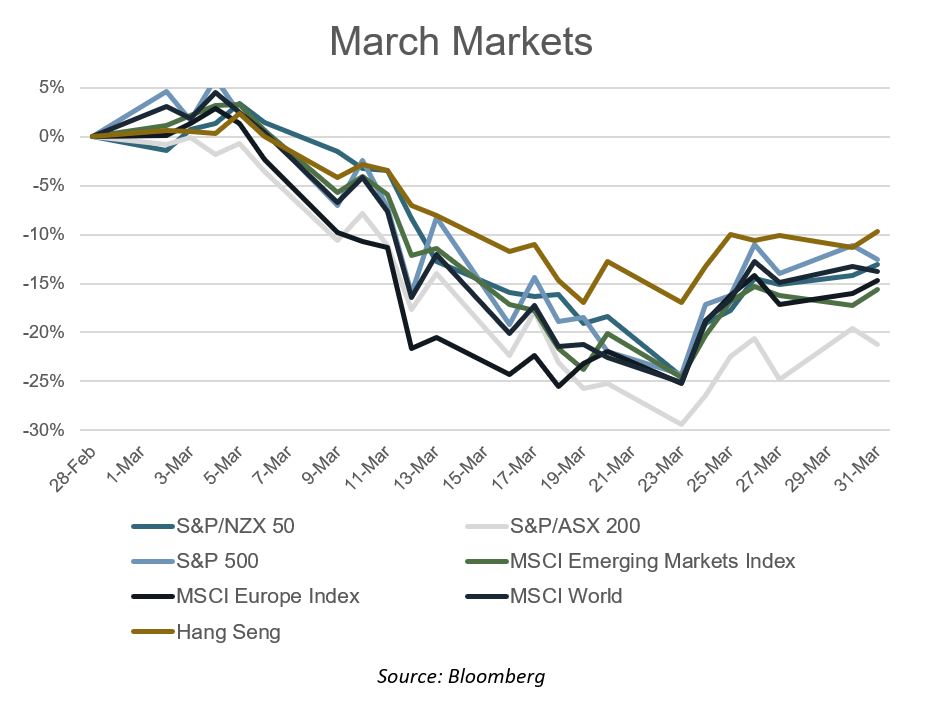

The record bull market in equities turned into a bear market in March, roughly 11 years after the last one ended. Volatility was extreme. The Cboe Volatility Index averaged 57.1 in March, triple the mean in the prior decade.

Volatility was not limited to equities. Gold topped $1,700 in early March before plunging $200 an ounce. West Texas oil lost 65% in the March quarter, the worst quarter on record. The US 10-year Treasury yield hit 1.94% on Jan. 20 then fell to 0.31% by March 9. The Reserve Bank of New Zealand cut the OCR to a historic low of 0.25% and started its own version of quantitative easing. March was historic.

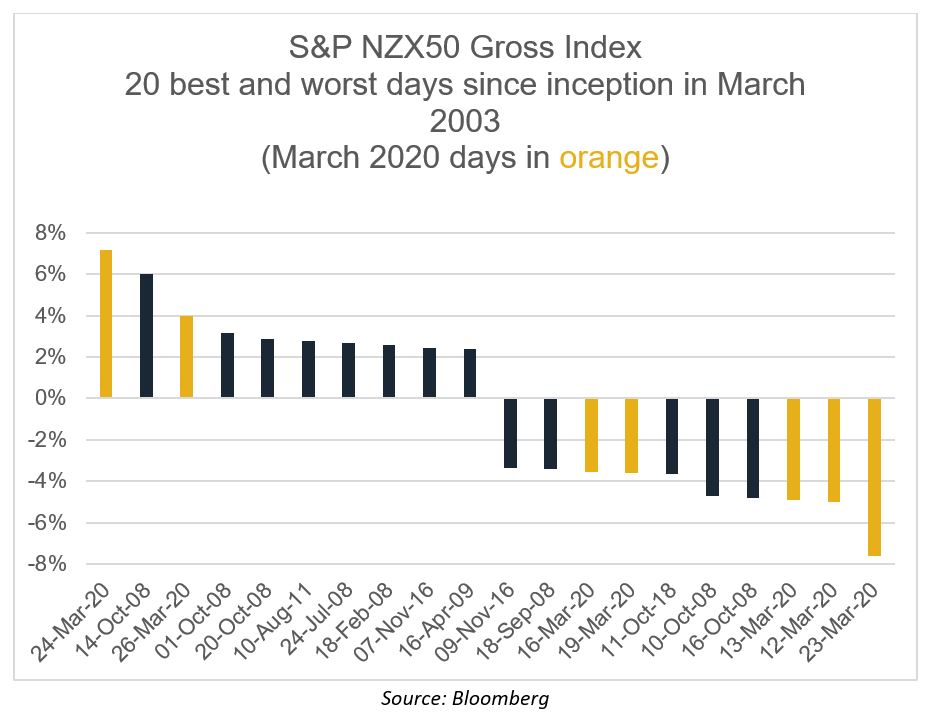

The New Zealand equity market fared better than most, albeit with substantial volatility. March saw the best and worst daily returns since the index was launched in March 2003. The index was down 25% at its lowest point for the month and down a whopping 7.6% on the 23rd of March alone, only to rally 7.2% the next day and continue to rally to the end of the month. The S&P NZX50 index was down 12.5% for the month, with only five companies posting positive returns, the two largest companies, Fisher and Paykel Healthcare and A2 Milk, among them. Fisher and Paykel Healthcare and A2 Milk currently make up 30% of the market capitalisation of the NZX50. Without them the New Zealand equity market would have been down closer to 20%.

There were some big individual company price drops. Tourism Holdings, Air New Zealand, Kathmandu and Vista all more than halving. At their worst point of the month Tourism Holdings was down 78%, Kathmandu was down 77% and Vista Group was down 70%. Daily volatility was extreme. Tourism Holdings posted the biggest day decline, down 46% on the 23rd of March. Gentrack carded the largest daily rise, up 40% on the last day of the month, but still managed to be down 33% for the month.

The New Zealand equity market now stands as a global outlier in terms of price being paid for its earnings. This is mainly due to the eye-watering Price-to-Earnings multiples on Fisher and Paykel Healthcare and A2 Milk, which have prices that are 74x and 39x their previous financial year’s earnings respectively.

Financial markets from here will likely be driven by the opposing forces of COVID-19 demand/supply shocks and government policy response. These forces are large. In New Zealand for example, the ANZ business confidence indicator has slumped to a near to all-time low and the decline in confidence is showing no sign of slowing. This is being countered by never-seen-before levels of monetary easing and fiscal stimulus.

A possible source of major surprise might be inflation. As noted by acclaimed economist and author, Kenneth Rogoff, “In contrast to recessions driven mainly by a demand shortfall, the challenge posed by a supply-side-driven downturn is that it can result in sharp declines in production and widespread bottlenecks. In that case, generalized shortages – something that some countries have not seen since the gas lines of 1970s – could ultimately push inflation up, not down.” The New Zealand Government has already noted instances of price hikes in New Zealand. Persistent inflation ends the ability of governments to keep money supply easy. That would be a negative surprise. A quicker-than-expected end to shutdowns via vaccines, effective treatments and better management strategies would obviously be a big positive surprise.

It is worth remembering that real companies exist under these volatile share price movements. Most of which, while doing it tough right now, will survive and ultimately prosper. Economic predictions have a bad accuracy record at best of times but are likely to be particularly unreliable in the medium term as high levels of volatility remain. Expect markets to reflect that.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Stephen has over 25 yrs investment experience & co-founded Castle Point, a NZ boutique fund manager, in 2013. Prior to that he worked at funds management companies in Auckland, London & Edinburgh. Castle Point WINNER FundSource Boutique Manager 2019

........

Castle Point has taken all reasonable care in the preparation of these articles, however accepts no responsibility for any errors or omissions contained within. Past performance is not necessarily an indication of future performance. Opinions expressed in these articles are our view as at the date of issue and may change

4 topics

Stephen has over 25 yrs investment experience & co-founded Castle Point, a NZ boutique fund manager, in 2013. Prior to that he worked at funds management companies in Auckland, London & Edinburgh. Castle Point WINNER FundSource Boutique Manager 2019

Expertise

Stephen has over 25 yrs investment experience & co-founded Castle Point, a NZ boutique fund manager, in 2013. Prior to that he worked at funds management companies in Auckland, London & Edinburgh. Castle Point WINNER FundSource Boutique Manager 2019

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Investing for the biggest market shift since the GFC

Livewire Markets

Equities

Why ex-20 is the prime hunting ground for ASX returns

Livewire Markets