Latest lithium market views and price forecasts, plus ASX lithium top picks

The broker that correctly predicted the continued demise of lithium minerals prices in 2024 provides one final lithium update for the year.

We’ve brought you all the major developments in Citi’s views on lithium minerals pricing and the ASX lithium sector in 2024 (see the full list of articles at the bottom of this one). They turned decidedly bearish in April, “doubly bearish” in May, and have remained that way since.

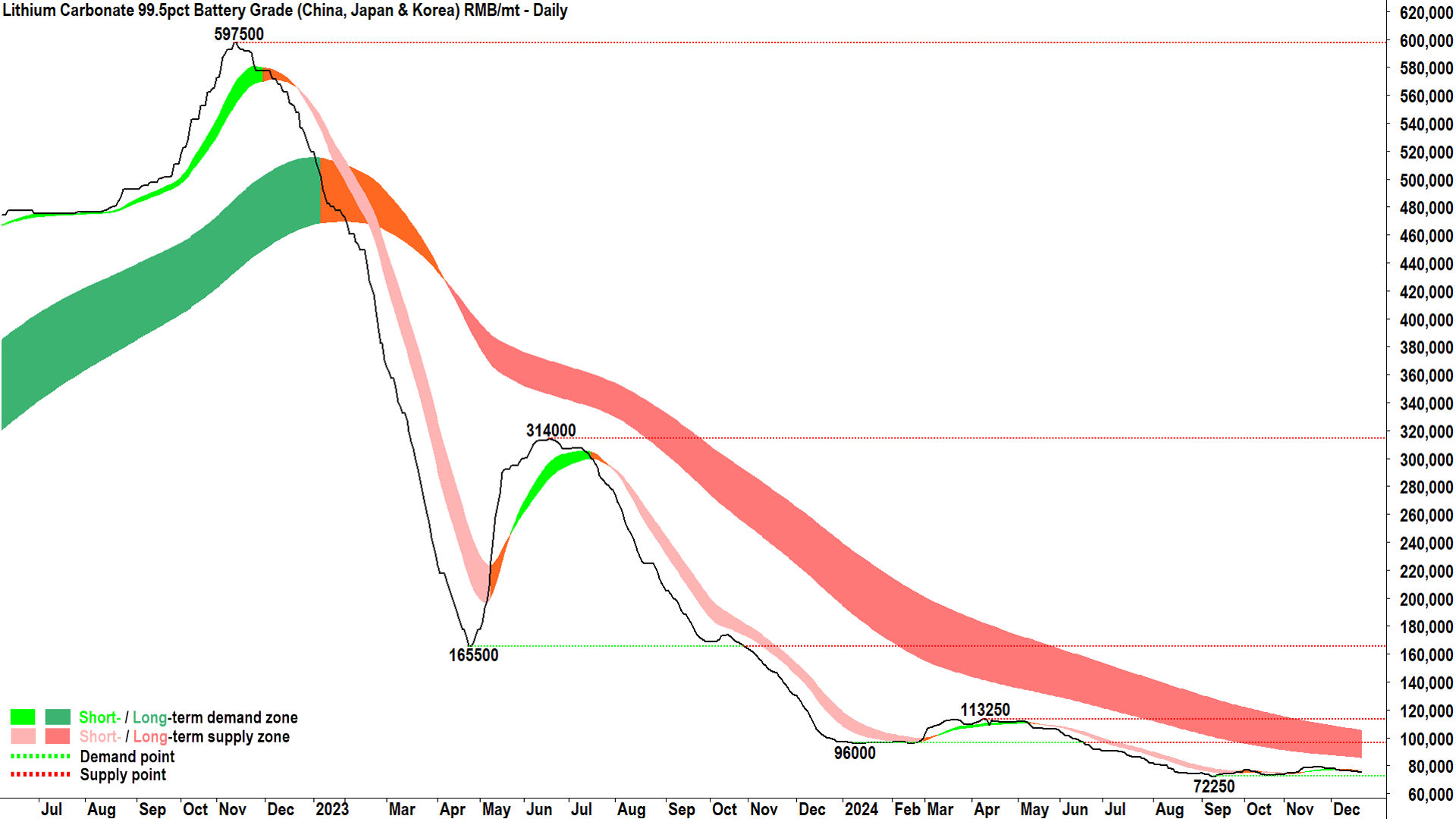

The broker’s calls have proven to be the best course of action with respect to lithium minerals prices, which coincidently put in their 2024 peak in mid-April around the time of Citi’s first bearish call. Since then, the price of the benchmark lithium mineral, lithium carbonate*, has fallen around 33% to RMB 75,000/t. (*Industry metrics are often discussed in terms of lithium carbonate equivalent or “LCE”).

In what is likely to be their final lithium-focussed update for the year, Citi has flagged further cuts in its lithium price targets for 2025 and beyond, but notes it’s beginning to see less downside in ASX lithium stocks. Let’s investigate Citi’s latest lithium views for one last time in 2024!

Where are lithium prices headed in 2025?

That’s the million-dollar question lithium bulls want answered, and given Citi’s accurate lithium market price predictions in 2024, it’s worth taking note of their newly updated views for 2025 and beyond.

Bad news lithium bulls, Citi has cut further their short-, medium-, and long-term price targets for two key lithium minerals.

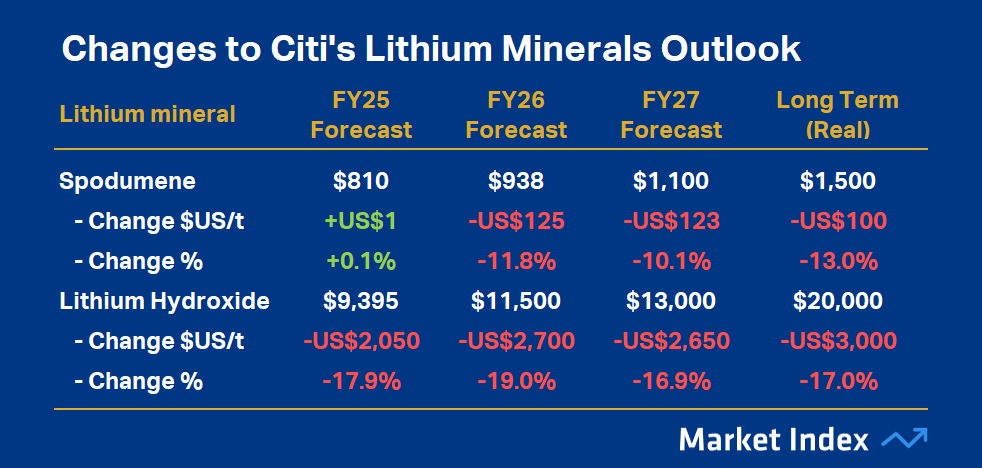

Firstly, spodumene – the lithium mineral produced domestically by Australian miners like Pilbara Minerals (ASX: PLS), Mineral Resources (ASX: MIN), IGO (ASX: IGO), Liontown Resources (ASX: LTR), and until recently by Core Lithium (ASX: CXO)*, has seen its price forecasts cut by 12% in 2026, 10% in 2027, and 13% in the “long-term” on an inflation adjusted basis. (*CXO put its flagship Finniss spodumene mine into care and maintenance in January).

If there is some good news on this item, it’s that Citi’s 2025 spodumene forecast grows by US$1/t to US$810/t. Note however, the current price of spodumene according to S&P Global Platts is US$810/t – i.e., in-line with Citi’s 2025 forecast. Spodumene prices are expected to increase in subsequent years, though, by as much as 15% in 2026, and 35% in 2027.

Next, lithium hydroxide, which is a critical precursor material in electric battery manufacturing, has seen its price forecasts cut by 18% in 2026, 19% in 2027, and 13% in the “long-term” on an inflation adjusted basis.

Note that lithium carbonate and spodumene are typically processed into lithium hydroxide for use in the electric battery supply chain. The current price of lithium hydroxide according to Chinese commodities data provider SMM is US$9,475/t – i.e., modestly above Citi’s 2025 forecast. Lithium hydroxide prices are expected to increase in subsequent years, though, by as much as 21% in 2026, and 37% in 2027.

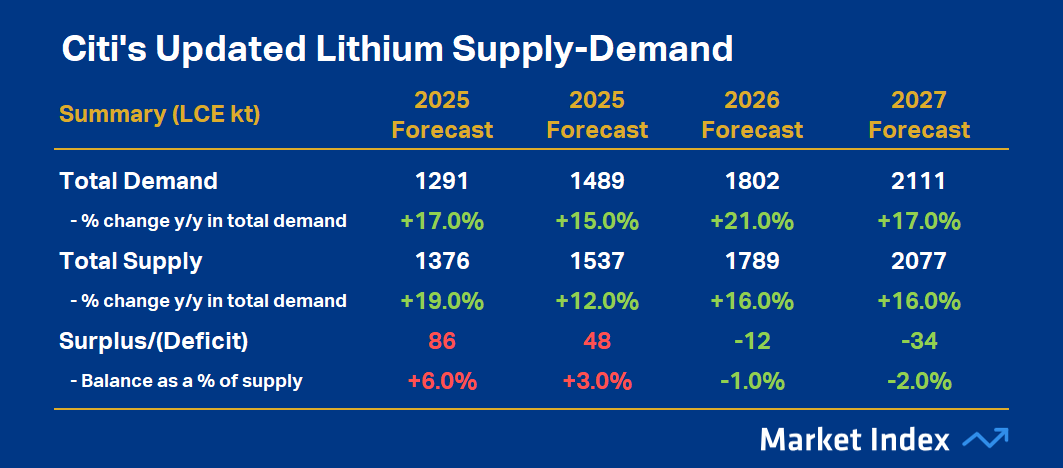

Interestingly, Citi did not provide updated forecasts for lithium carbonate pricing, but did provide its latest views on when the market would finally work through the current supply surplus in LCE terms. The broker notes that we’ve likely passed the peak in the lithium minerals supply glut, and 2026 will be the first year of a return to deficit (12kt LCE). That deficit is forecast to expand in 2027.

That’s potentially good news for lithium bulls who are prepared to stay the course, but there are two potential sticking points, proposes Citi. Firstly, in the short term, the broker believes “price upside appears capped by high inventories and idle capacity”.

Whilst Citi concedes recent market conditions show a near-term rebalance in lithium supply driven by supply cuts and strong China battery production, much of the latter is likely due to manufacturers trying to front-run looming US tariff hikes.

Outside of the short-term rebalancing theme, the broker highlights a “soft ex-China EV demand outlook” in the USA and Europe, and anticipates a “further surplus in 2025,” partly due to payback from earlier export front-loading.

Potentially tempering the longer-term bullish implications for those forecast 2026-27 lithium deficits, Citi notes that they’re “small relative to inventory availability”. This implies deficits in those years don’t automatically translate into higher lithium prices in those years and beyond due to the substantial inventory that’s likely to be still weighing on the market around that time.

On an encouraging note, prices may have found their floor, notes Citi. Downside pressure will likely be curbed by supply cost curve support, as “higher incentive prices are needed to overcome the higher CAPEX and often OPEX*”. “As yet, we have not yet seen significant incentives to overcome this,” the broker concludes. (*CAPEX = capital expenditure, OPEX = operating expenditure).

In the long term, Citi believes the lithium supply chain will need to decouple from China. In line with decoupling trends, the broker points to Volkswagen’s stake in Patriot Battery Metals (ASX: PMT), where the major global car manufacturer purchased a 9.9% stake in the ASX and TSX-listed developer as well as signing a binding offtake agreement for the supply of lithium minerals.

are ASX lithium stocks a Buy, hold, or sell in 2025?

Turning our attention now to Citi’s views on the ASX lithium sector. “2024 has been a tough year” for ASX listed lithium companies, notes Citi in perhaps the understatement of this investing year!

“It’s hard to see a catalyst in the near-term for the equities to re-rate aside from a post CNY restock”, the broker warns. Encouragingly for ASX lithium bulls, Citi does concede however, that “valuations now look reasonable”.

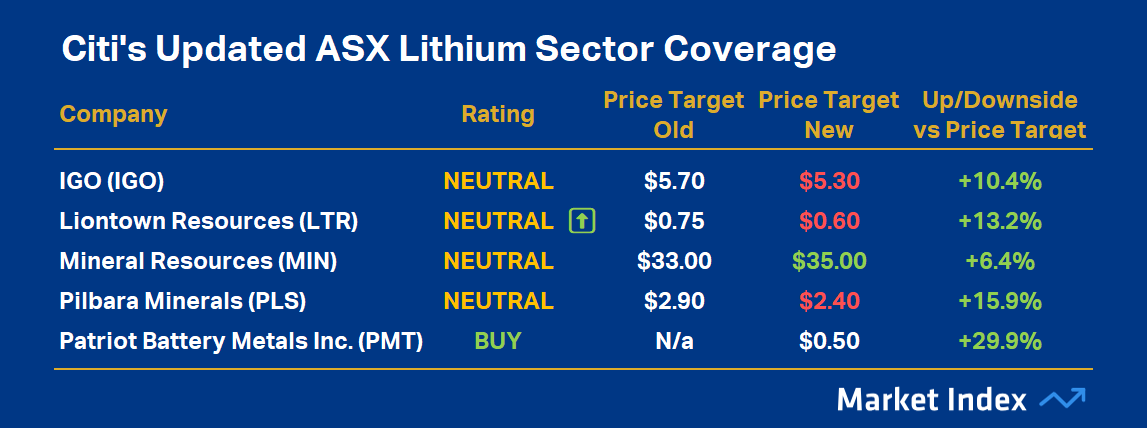

In larger capitalisation stocks, Citi continues to prefer PLS as an “established net-cash producer”. Despite this, Citi is only NEUTRAL rated on the stock with a price target of $2.40, cut substantially from the previous price target of $2.90. Still, based on Friday’s close of $2.07, this does allow for just over 13% upside.

I note Citi also put in bold writing: “We think investors should closely track IGO given there are several catalysts which may improve the investment thesis come Q2”. Those catalysts include getting through suspended dividends from Windfield this quarter, a decision on the company’s Kwinana operations that’s “likely to unwind the complexity of the TLEA cash sweep”, plus further disclosures on Greenbushes.

In smaller capitalisation stocks, Citi’s preference is the only BUY-rated ASX lithium stock in its coverage, PMT. The broker notes PMT’s “strategic appeal” is “underpinned by our view that it’s the best greenfields discovery this cycle supported by the high-grade Nova and Vega zones”.

Citi’s other ASX lithium rating and price targets changes are summarised in the table below. I note in particular, the upgrade in LTR’s rating to NEUTRAL from SELL, and price target cuts for IGO, LTR and PLS. MIN is the only lithium stock in Citi’s coverage to enjoy a price target increase.

Citi’s updated ASX lithium coverage. Source: Citigroup Inc. (From: “Australia Diversified Metals & Mining Lithium: range bound through 2025; Cutting TPs”, Citi Research, 19 December 2024). Source: SMM (click here for full size image)

Market Index’s coverage of Citi’s views on lithium in 2024:

Citi downgrades ASX lithium sector earnings. This is its only remaining buy (Published: Tue 22 Oct 24)

Real production costs at ASX lithium miners will shock you: Just one mine is profitable (Published: Tue 03 Sep 24)

Citi now “doubly bearish” on lithium (Published: Wed 22 May 24)

Lithium rally is “detached from fundamentals” Go short says Citi (Published: Thu 18 Apr 24)

Citi and UBS weigh in on lithium rally: Don’t assume low is in yet (Published: Wed 06 Mar 24)

This article first appeared on Market Index on Monday 23 December 2024.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl has a passion for technical analysis and has taught his unique brand of price-action trend following to thousands of Aussie investors.

........

Investing is risky. Inevitably you will endure losses. If you can't cope with losing, don't invest.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

5 topics

6 stocks mentioned

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl...

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl...

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Buy Hold Sell: 5 ASX stayers built to go the distance

Livewire Markets

Funds

The 5 best-performing super funds of the year

Livewire Markets